Risky asset classes such as equities have recorded price increases at the beginning of the year. The core question for the investor is whether this recovery after the sharp decline in Q4 is sustainable or not.

Growth weakening

Chart 1: falling economic indicators

The global economic cycle is currently on the decline. Real global economic growth has been on the fall since Q4 2017. GDP growth has reached trend growth levels. Remarkably, the goods sector is particularly sensitive to the downturn. In many countries, industrial production was falling significantly at the end of 2018. The majority of survey-based leading indicators (purchasing managers’ indices, OECD leading indicators – see chart 1) suggest further decline in growth. Is this development only a form of normalisation after a phase of unsustainably high growth rates, or has the risk of recession actually increased?

Weakly positive signals

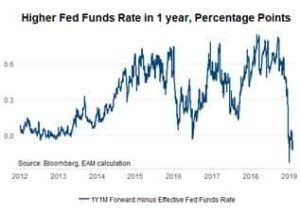

Chart 2: no further Fed funds rate hikes

Not all economic indicators are facing south. There are a number of signals that suggest the stabilisation of economic growth, albeit at low levels. As far as the purchasing managers’ index for January is concerned, two important sub-categories have increased, i.e. new orders in the USA and imports in China. In Germany, the number of spin-offs of capital goods in December increased relative to the previous months. Also, credit growth stopped falling in China in the month of December (m/m). This environment suggests an imminent end of shrinking industrial production.

Monetary policy supports financial market

The monetary policy is lending strong support to the markets yet again:

- The US Fed has given up its tendency towards further interest rate hikes. As a result, the worries of the economy and the markets over excessively high interest rates have therefore disappeared (for now). The future interest rate hikes priced into the market for the coming 12M have reversed from 0.8 percentage points in September to currently a slight cut (see chart 2). Also, the US Fed has signalled its intention of ending the process of shrinking the balance sheet sooner than generally expected (i.e. more liquidity).

- The ECB has mentioned downside risks to the economy (i.e. recession risks). This makes a soon reversal of the currently very expansionary monetary policy even less likely.

- In China, the reserve requirement ratio has been cut repeatedly (i.e. more and cheaper liquidity for banks). The growth rate of the central bank balance sheet increased in December after a downward trend throughout the year.

Summary

The main motive cited for abandoning the gradual tightening of the monetary framework is the deterioration of the financial environment (i.e. falling share prices, higher credit spreads). This does not mean that falling share prices are to be avoided per se. Rather, this is about putting a halt to the negative feedback from the deteriorating financial environment to the economy. And it seems to be successful for the time being. A (possible) end to the weakening growth rate in the first half of the year combined with a still expansive stance by the central banks supports (for now) risky asset classes (equities, emerging markets). This would also require the leading indicators for economic growth to stop falling soon.

Disclaimer:

Forecasts are not a reliable indicator for future developments.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Turkish financial markets temporarily under pressure following political turbulence

The Turkish stock market has been turbulent recently: the arrest of Istanbul mayor Ekrem Imamoglu caused massive uncertainty. What does the political unrest mean for the Turkish economy and the Istanbul stock exchange?

Environmental stocks: How is the sector faring in the current volatile environment?

The first quarter had a few surprises in store for the markets. The US tariff announcements shook the markets to the core and caused a volatile stock market environment. The environmental technology sector was not spared either. What is the outlook for the sector? We asked fund managers Clemens Klein and Alexander Weiß in a double interview.