The US central bank, the Fed, is very likely – almost 90%, according to Fed funds futures – to raise the Fed funds rate this year. The expected rate hike has been one of the dominating topics on the financial markets for a year. The bursting of a mega bubble, rising pressure on fragile emerging markets, and the end of years of a share market rally in the USA are the most commonly mentioned worries in this context. None of which is overly far fetched, as we have indeed seen all of these scenarios before. Still – history prompts the conclusion that there is no need to panic, at least not when it comes to equities.

Effects differ every time

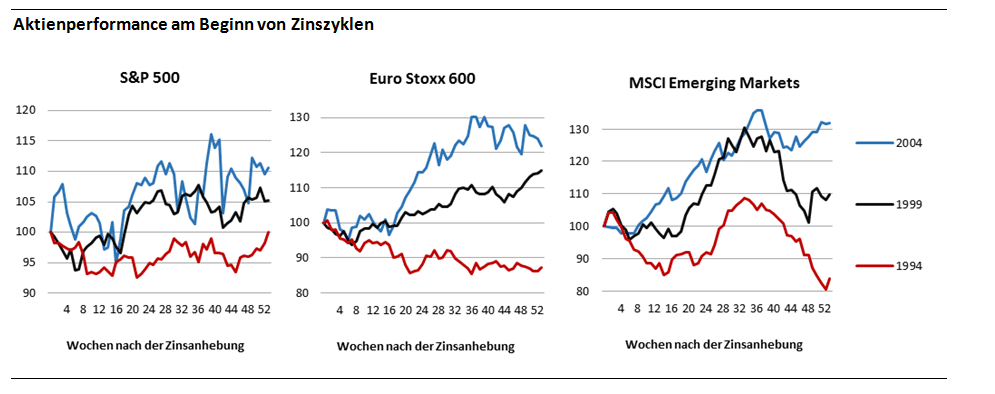

In the past 25 years we have seen three comparable phases, where the Fed increased the Fed funds rate after a longer period of low interest rates and set off a new interest rate cycle: 1994, 1999, and 2004. Although the results were different every time, they were never disastrous. While the equity markets did almost always come under pressure immediately after the rate hike, they also experienced a recovery about four months after the Fed funds hike. After the hikes in 1999 and 2004, the S&P 500, the Euro Stoxx 600, and the MSCI Emerging Markets index had already clearly exceeded their respective levels prior to the interest rate hike by the Fed (by up to 30%) within six to nine months. Only in 1994/95, when the Fed funds rate was increased by three percentage points to 6% within twelve months, European and emerging markets equities lost significantly, and the subsequent recovery took longer.

Sources: Bloomberg; own calculations

Surprise effect should play a subdued role

A number of arguments suggest that the equity markets should be reacting less noticeably to the interest rate reversal. Firstly, there has probably never been a monetary measure that was discussed in more depth and in public than this interest rate increase. The surprise effect should be very limited. Secondly, in spite of the recovery since last year the US economy is still weaker than at the beginning of previous interest rate cycles. Inflation remains non-existent. We therefore expect moderate increases and a flatter upward path than at previous occasions. Thirdly, the US interest rates will be increased around a time when the ECB and the Japanese central bank are sticking to their monetary loosening for domestic reasons, and the Chinese central bank may soon follow that stance. And lastly, with regard to the emerging markets – while there are a few weak economies such as South Africa and Turkey, overall the block of emerging markets is in better shape than it was at the middle of the 1990s.

Elevated volatility expected

For equity investors, the expected rate hike by the Fed means that elevated volatility and short-term pressure are to be expected. There might be trading opportunities (which at hindsight will of course have been crystal-clear), but the empirical evidence does not suggest that the interest rate policy of the Fed would trigger a change in strategy among equity investors with a long-term horizon.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.