Equities from the environmental sector have recently been somewhat snubbed by the market. Rising interest rates and the associated higher financing costs are weighing on the sector. However, figures suggest that the expansion of renewable energies, for example, is continuing at a rapid pace. Also, the AI boom in the technology sector could cause demand for electricity to skyrocket – demand that is to be met primarily by renewable energy sources.

While it is true that some shares in the environmental sector have already turned around in recent months, the sector has retained its historically low valuations. Fund manager Alexander Weiss explains his view on the current market environment for cleantech equities and why the sector could be exciting right now.

Note: Please note that an investment in securities entails risks in addition to the opportunities described.

Shares from the clean tech sector have been among the underperformers on the market for some time now. What are the reasons for this?

Alexander Weiss: The main reason is definitely the current interest rate environment. In the cleantech sector, the companies are generally younger, and many of them have secured variable financing. Younger companies also have higher capital requirements. Both of these factors have recently put pressure on these companies and their market valuation, as we have seen very strong and above all rapidly rising interest rates in the past two years.

In addition, the interest rate is a crucial part of the valuation of renewable energy projects. There are very few running costs for a wind turbine or a large-scale solar plant. The majority of the costs are incurred at the time of construction. As these projects are financed by debt, the impact of higher interest rates is very noticeable.

Some people are already talking about valuations for environmental shares that have not been seen for a very long time. Would you agree?

That’s right, in the past, the valuations in the environmental technologies sector would have usually been above that of the market as a whole. This is due to the fact that we invest in more dynamic companies that are still in the growth phase. In addition, sectors that command more favourable valuations are generally excluded, such as oil & gas companies, banks, or traditional car manufacturers. To put it bluntly: Tesla basically trades at a higher valuation than Volkswagen. However, I would like to point out that we are not invested in either company in our environmental equity fund.

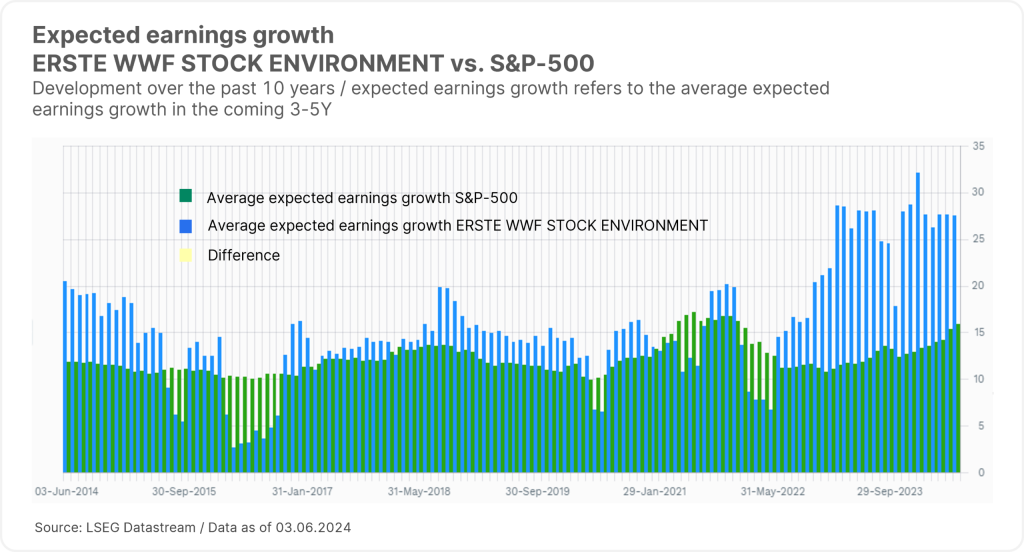

That being said, we have recently observed something that has never really happened in our segment before – we are now trading at lower valuations than the broader market. In addition, the growth prospects in the segment are more favourable than in the broad market. The expected earnings growth over 3-5 years is almost twice as high as that of the MSCI World index.

Please note: Past performance is no reliable indicator of future performance. The average expected earnings growth is based on analysts’ expectations for the individual companies in the ERSTE WWF STOCK ENVIRONMENT and the S&P 500 share index over the next 3 to 5 years. Forecasts are not a reliable indicator of future performance.

However, we can now also see that the fund has been trading at attractive levels compared to the broad market for some time.

Correct – valuations are generally not perfect as a tool to work out the timing of investments. We don’t mean to say that the fund cannot become even more attractively valued. However, if you have a long-term horizon, valuations are very relevant for long-term performance – this also makes intuitive sense.

We have also recently seen an increase in transactions from the private equity sector for listed renewable energy companies. Private equity also recognises that the current valuation levels are excessively low and snap up these publicly listed companies. In our view, this provides a certain floor in terms of valuations.

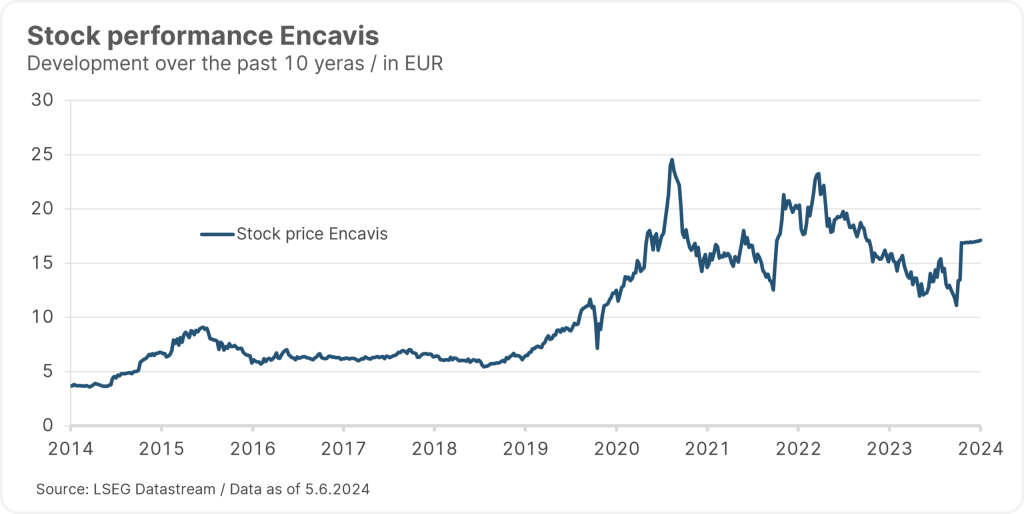

One example of this is the takeover of the German company Encavis by KKR, one of the top five private equity firms in the world. Encavis develops solar and wind parks in Europe, with a focus on Germany. We have been invested since 2015 and last visited the Hamburg-based company in 2023. With the takeover bid, the share price jumped by almost 60%. We therefore seized the opportunity and sold our position. Examples like these show that the sector currently commands a favourable valuation in both relative and absolute terms.

(Please note: past performance is no reliable indicator of future value development. The company listed here was selected as an example and does not constitute an investment recommendation).

Takeovers in the renewables sector have increased recently. At the end of May, Energy Capital Partners announced its intention to acquire Atalantica Sustainable Infrastructure, a renewable energy developer, for USD 2.55bn. The share price has risen by 20%+ since speculation of a takeover took hold. Brookfield Renewable also announced plans to acquire Neoen, a French solar, wind, and battery storage developer. The share price has risen by over 40% on the back of these takeover rumours. OX2, a Swedish developer of wind turbines, was also taken over at a premium of 42%.

These announcements illustrate that the segment is currently trading at steep discounts and that long-term investors are still interested.

Most recently, we have heard more and more about artificial intelligence (AI) and data centres as well as their impact on the energy landscape. What is going on in that segment – how much of it is hype and how much is real?

Everyone is currently talking about AI and wants to be part of the potential next revolution. We shouldn’t, however, underestimate the enormous power consumption required by data centres and, above all, artificial intelligence models. We have analysed this topic intensively and have come to the conclusion that it will have a strong impact on our environmental equity funds. The demand for electricity in the USA will grow more strongly from now to 2030, i.e. within six years’ time, than it has in the past 25 years. After years of more-or-less flat electricity demand, data centres are ushering in a new era of growth. When even conservative utility companies almost double their assumptions, it also gives us confidence that it can’t just be a hype.

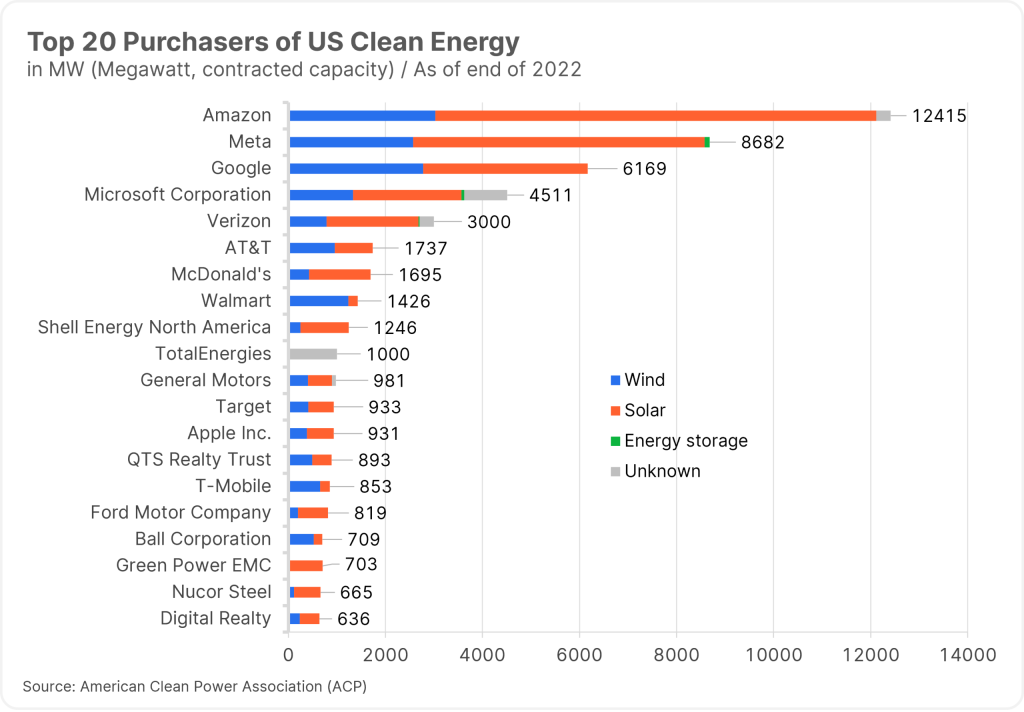

Depending on the forecast, data centres will account for between 6 and 7.5% of total US electricity demand by 2030, up from just 2.5% in 2022. However, we can also see enormous growth in the data centre sector on a global level. This growth is driven primarily by big tech, i.e. Amazon, Microsoft, Google, and Meta are already among the largest energy consumers in the world. The chart below shows the contracted capacity, i.e. the ordered capacity of green electricity in the USA.

As you can see, Big Tech is the most important consumer. These companies now have their own departments that deal with the energy needs of data centres. Of the top suppliers in America, McDonalds is only in sixth place, a company that is not active in data centres. (Please note: the companies mentioned here have been selected as examples and do not constitute an investment recommendation.)

Why do tech companies rely largely on green electricity to meet their growing demand?

The big tech companies have set themselves ambitious environmental targets. In the future, they want to source 100% of their electricity from renewable energies, so the electricity must be green. A second important factor for these companies is speed. Given the extreme demand, it is particularly important that the power supply can keep up with the massive expansion of the data centres. Solar power is particularly exciting here because it can be connected to the grid very quickly.

The price is less relevant for these companies. It’s more about securing the power supply in a timely manner so as not to fall behind in the field of artificial intelligence.

What also confirms that the demand for artificial intelligence is more than just a hype are the investments that Big Tech in particular has recently announced in its quarterly reports. Amazon, Microsoft, Google, and Meta have massively stepped up their capital expenditure. These investments are flowing almost exclusively into data centres, particularly in the field of artificial intelligence.

All these data centres require sufficient electricity. This is where companies in ERSTE WWF STOCK ENVIRONMENT and ERSTE GREEN INVEST enter the picture, as illustrated, for example, by a deal for the purchase of renewable energy that was concluded between Microsoft and Brookfield Renewable Partners at the beginning of May.

Companies in the electrical engineering sector are also benefiting from the rapid expansion. Companies such as Schneider Electric, which supply the infrastructure for data centres, are experiencing enormous growth rates in this segment. In short, the investment opportunities arising from the increased energy demand for artificial intelligence are real and tangible. (Please note: the company mentioned here has been selected as an example and does not constitute an investment recommendation.)

So, although the latest price movements in the segment do not reflect it, is the expansion of renewable energies still taking place?

Yes, expansion is still taking place, and at a rapidly growing too. The invasion of Ukraine by Russia in 2022 has given a huge boost to the issues of energy security and energy autonomy. We saw a real shift in 2022, with a massive increase in global solar capacities. This gave way to an even stronger expansion in 2023, with growth up 76% compared to 2022! The market here is primarily driven by China, but the rest of the world has also seen enormous growth rates.

Solar power has now become one of the cheapest sources of electricity and can be installed very quickly. Even Texas has now realised this – traditionally better known for the oil & gas industry, it has been by far the largest producer of wind energy for some time now. Recently, however, the state has also seen a considerable increase in solar installations, so much so that it has overtaken California as the market leader! So, you can see that profitability can ultimately prevail over ideology.

Is there anything to be learnt from this for the US elections in November?

Many of the subsidies that are currently available in the USA via the Inflation Reduction Act (IRA) in the field of renewable energies go to traditionally Republican states. Investments in battery or solar module factories occur at an above-average extent in “red” states. We therefore believe that the political risk of a repeal of the IRA is limited. The governors of those states that benefit from it will speak out against it. In addition, repealing a law without an absolute majority is very difficult. As a result, this scenario is very unlikely at the moment.

Investing in environmental technologies and cleantech

Our environmental equity funds ERSTE WWF STOCK ENVIRONMENT and ERSTE GREEN INVEST, give you the chance to make broadly diversified investments in pioneers in the field of environmental technologies. As impact funds, both aim to have a measurable, positive effect on the environment and society.

This article is part of the July 2024 issue of our ESGenius Letter. All other articles in this issue, as well as previous versions of our sustainability publication ESGenius Letter, can be found on our website.

👉 Read now

Please note that investing in securities involves risks as well as opportunities.

Further articles that might interest you 👉

No Posts Found

Notices ERSTE WWF STOCK ENVIRONMENT

The fund pursues an active investment policy and does not follow a benchmark. The assets are selected at our discretion, without any constraints to the latitude of judgement on the investment company’s part. Please note that investing in securities also harbours risks in addition to the opportunities described above.

For further details on the sustainable strategy of ERSTE WWF STOCK ENVIRONMENT and on the Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐related disclosures in the financial services sector and the Taxonomy Regulation (Regulation (EU) 2020/852) please refer to the current prospectus, section 12 and the appendix, “Sustainability principles”. When deciding to invest in ERSTE WWF STOCK ENVIRONMENT, please take into account all features and goals of ERSTE WWF STOCK ENVIRONMENT as described in the fund documents.

Notices ERSTE GREEN INVEST

The fund pursues an active investment policy and does not follow a benchmark. The assets are selected at our discretion, without any constraints to the latitude of judgement on the investment company’s part. Please note that investing in securities also harbours risks in addition to the opportunities described above.

For further details on the sustainable strategy of ERSTE GREEN INVEST and on the Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐related disclosures in the financial services sector and the Taxonomy Regulation (Regulation (EU) 2020/852) please refer to the current prospectus, section 12 and the appendix, “Sustainability principles”. When deciding to invest in ERSTE GREEN INVEST, please take into account all features and goals of ERSTE GREEN INVEST as described in the fund documents.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.