On 14 March our Investment Committee met, and as always, we started out on a discussion of our risk stance, i.e. our risk assessment. From my point of view, four findings of the discussion are worth bringing up here:

- We have become bolder in our asset allocation. Our risk stance has increased from 70% to the maximal risk exposure of 75%. This is also in line with our risk assessment of the market, which increased from 48% in February to now 55%. The first message is therefore: we are still willing to assume risk and, from our point of view, more so than the market.

- The second finding was the fact that we act pro-cyclically. After the correction in February our willingness to take risk had declined, but now, as some time has passed and prices have increased, we are ready to up the risk again. If this pro-cyclical risk assessment turned out to be the norm, things might become expensive. The degree of cyclicality is only slightly higher (from 70 to 75%), but it is crucial to remain vigilant all the same.

- A large part of the discussion was about the question of what more or less risk in a mixed portfolio meant. We were on the same page that in the current environment the less risk would mean more cash, i.e. a scenario of limited attraction. The negative correlation between equities and government bonds, which used to be something you could rely on in the past, does not seem that cogent anymore going forward.

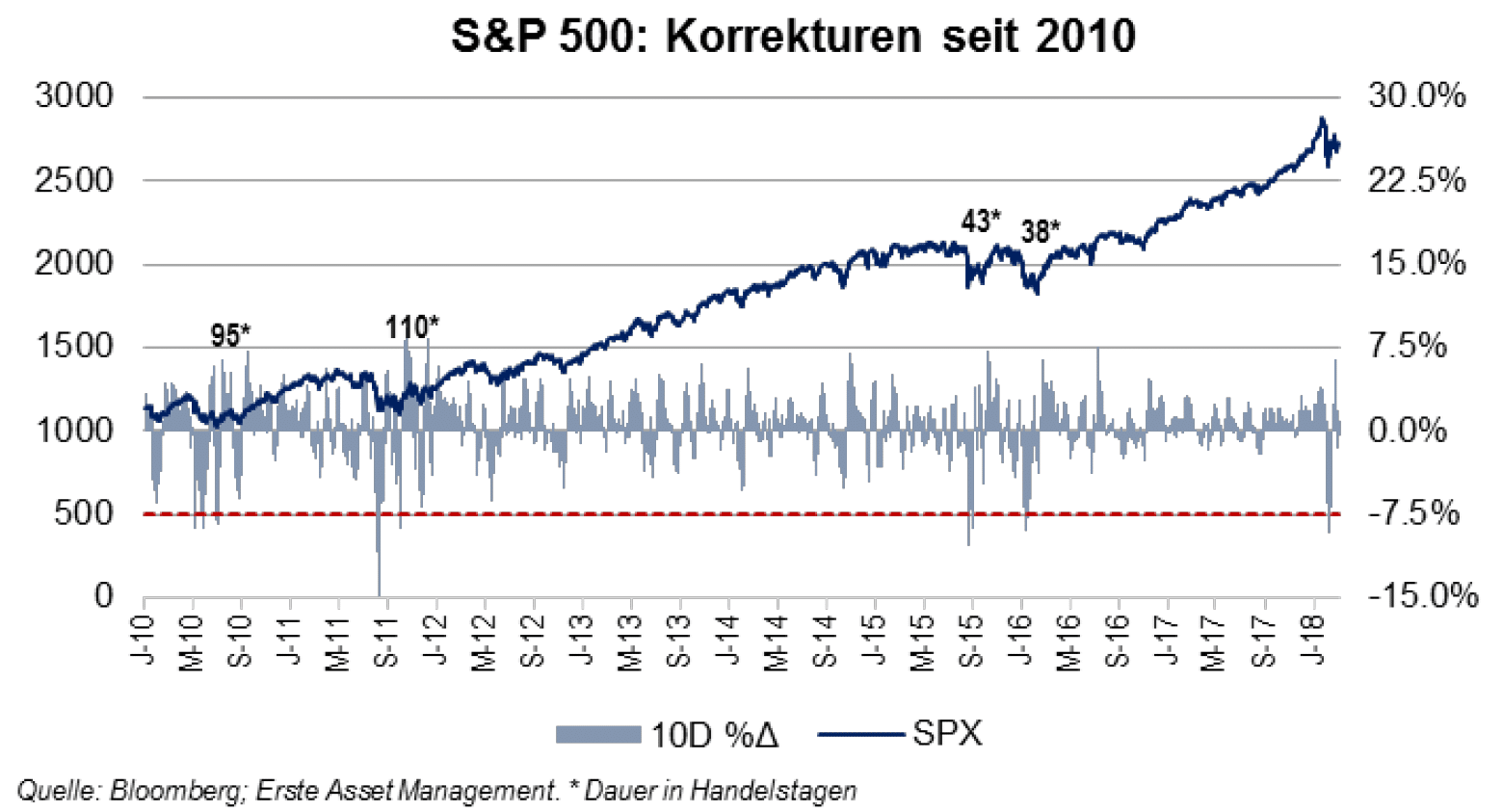

- The fourth finding was our unanimous opinion that equities would pick up some more within this cycle, as a result of which we expect prices to close the year at higher levels than today. However, opinions were divided on whether we have seen the other side of the February correction or not. Here, even the most recent past fails to provide us with any insight into the imminent future: since 2010, the S&P 500 index has corrected four times by more than ten percent within very short periods of time. In all cases, the pre-crisis highs were recuperated, but within largely different time frames (38 to 110 trading days). Also, as a rule, the upward trend would not pick up immediately nor continuously after the correction.

At that point we started the general discussion about the market.

- Economic growth is still broad and strong, but many indicators suggest that the wave is about to break. Thus, they confirm what in the current phase one would be expecting anyway. After an acceleration phase, a phase where the economy continues to grow above trend ideally follows; however, at that point, the growth rates are in decline: the classic late boom phase.

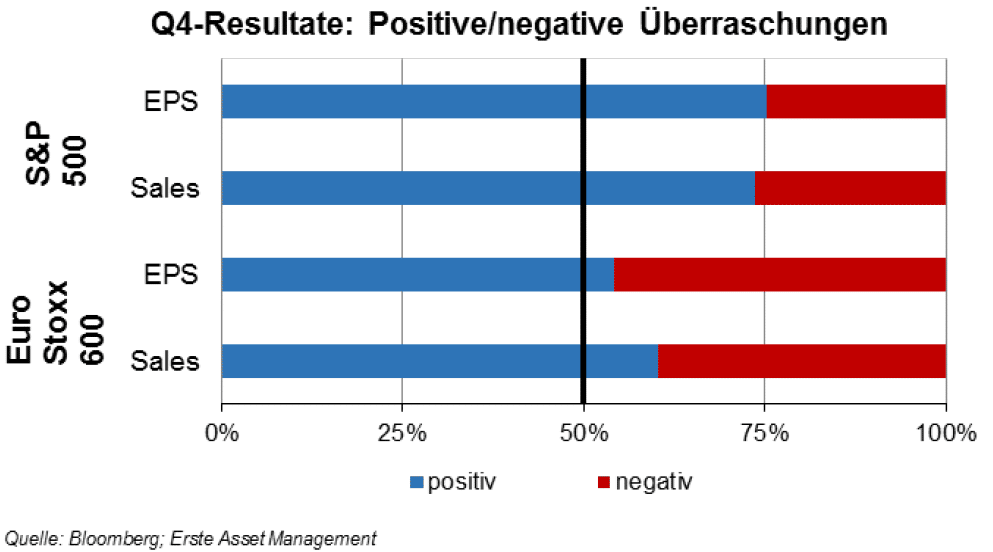

- The inflation surprises of January and February have been absorbed. The market has accepted that inflation can also rise again, and with this piece of news having been priced into the expectations of interest rate hikes and many asset prices, the topic itself has moved out of focus a bit. In fact, the inflation expectations for the USA priced into the market (for example the 5Y5Y inflation swap) have even fallen in the past weeks. The contributions made by our equity managers were also interesting in this context. While many US companies have reported that the tight labour market impedes their future growth and could result in higher wages (and thus lower margins), the numbers do not yet reflect that. For example, within the framework of the previous earnings season, the US companies were producing bigger surprises in earnings than in sales. If the wage pressure were to make itself felt already on a broad scale, it would probably have to be the other way around.

The question of what industries were particularly susceptible to overheating – especially in view of the tax reform – yielded a similar result. While the positive impulses of the tax reform cannot be attributed to certain industries without fail, there is agreement that mainly companies that focus on the domestic market (retail, utilities, telecoms, oil & gas) should benefit. Here, too, we can see only few signs of overheating caused by the labour market so far.

- In this scenario we expect the Fed to raise interest rates four times in 2018, starting at the next FOMC meeting on 21 March, by 25bps each (N.B. 100bps = 1 percentage point). At the beginning of the year, we had expected three rate hikes of 25bps each. This means that at the end of the year, the bandwidth of the Fed funds rate should be 2.25 to 2.50%.

- We were discussing tariffs and other protectionist measures at length in our meeting. Protectionism was generally regarded as negative for the economy and the financial markets. The effects are multifaceted, ranging from less growth, higher inflation, and lower trade activity to higher economic uncertainty. Companies are faced with a situation where their plans for the future could become practically void as the result of a signature. While this is undoubtedly true, one has to point out that the extent of protectionism at this stage is still very limited (N.B. as a colleague summed it up: the entire US steel industry is worth less than the upswing in market value of Netflix this year). Also, the status quo is not overly different than what we have seen in similar cases in the past. As Max Weber said, trade policy is like drilling through hard boards. This gives us hope that we will not see any real trade war. Trade requires focus, persistence, and patience. Those are not exactly the fortes of the current US Administration.

-

- The relative high twin deficits (i.e. elevated budget and current account deficits) expected for the coming years in the USA were another item on our agenda. For the coming three years, a budget deficit of more than 5% and a current account deficit of about 3% are expected. These values would have resulted in a mission by the IMF in the 1990s. Our discussion indicates that there is a large bandwidth of opinions with regard to this topic, which is potentially important and may stay with us for a while. The aforementioned bandwidth suggests that we will have to talk about this issue in more detail in the coming weeks.

This led us to look at the risk scenarios for the coming three months.

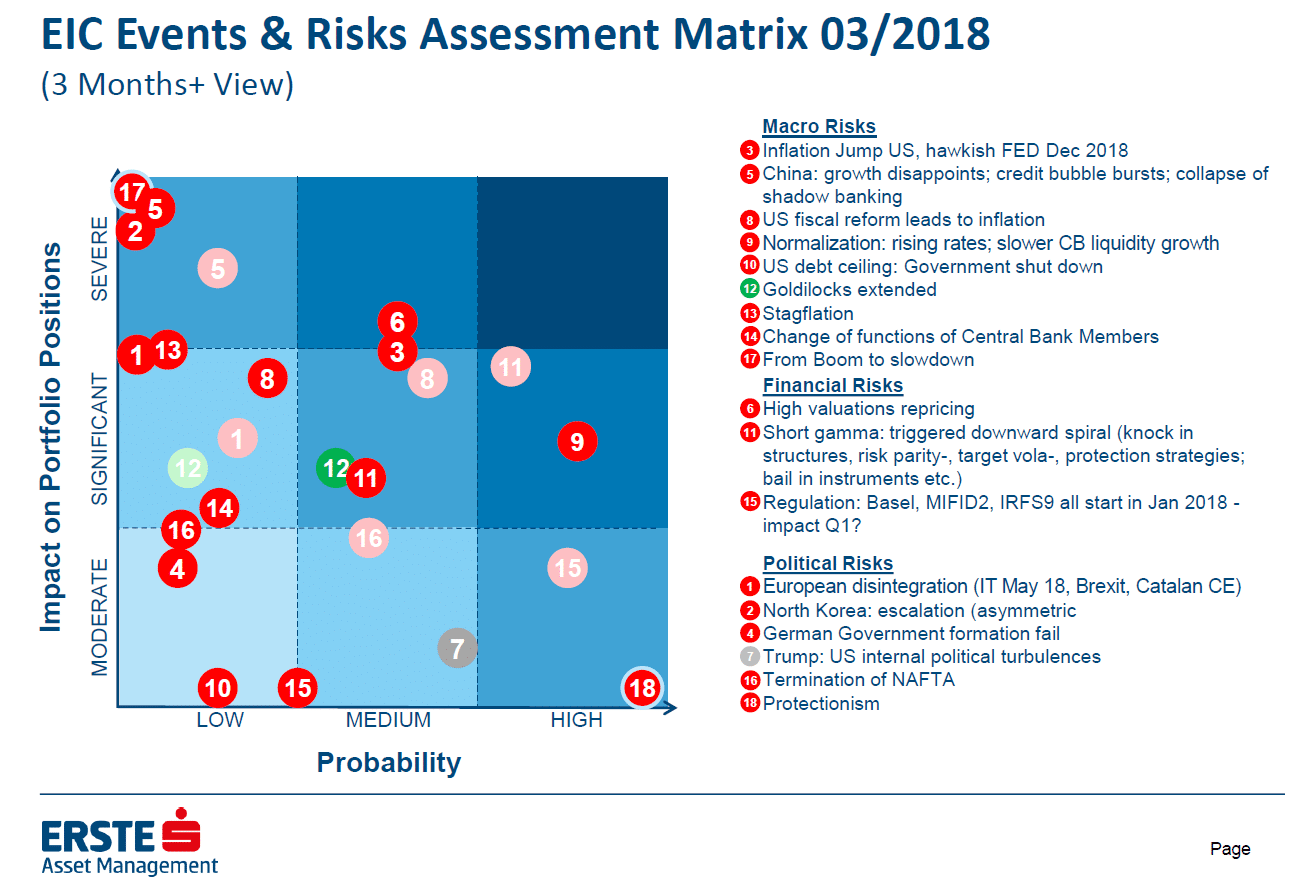

From our perspective, the biggest three risks (in terms of probability of occurrence and potential effect) are an (3) increase in inflation, which leads to a more aggressive Fed policy, (9) the normalisation of the monetary policy (i.e. the end of the bond purchasing programme by the central banks), and the generally (6) high valuations on the financial markets. The risks we downgraded were the (8) effects of the US fiscal reform and (11) negative effects of a position unwind [1]. The former will merge into the topic of twin deficits in the long run, and the latter has partially happened in February, as a result of which the risk itself has declined.

[1] In view of the very low volatilities and the strong positioning in some illiquid market segments (e.g. derivatives on the VIX) we were concerned about the risk that an increase in the volatility among many instruments (e.g. VIX ETFs, some of which lost more than 90% of their values in February) or pro-cyclical hedging strategies (e.g. PPI concepts) might set off a selling spiral (losses trigger automatic sale orders, which in turns takes prices even lower).

Peripheral government bonds overweighted – equities of developed markets continue to harbour significant upward potential

We have reduced interest rate risks in the government bond segment. The peripheral countries (except Italy) have been overweighted. We expect corporate bond spreads to increase until the end of the year, both in the investment grade and the high-yield segment. In the USA, we regard this segment as better supported by the earnings profile and tax reform, which is why we expect spreads to remain stable and prefer these market segments in the asset allocation. We still see upward potential for equities. With regard to developed vs. emerging markets, we believe that the outperformance by the emerging markets has come to an end.

The EUR/USD development from here on out has been a special topic over the past months already. While the discussion yielded numerous different points to consider, a short vote did produce a relatively clear result: a large majority of participants expects the US dollar to appreciate.

The chairman by seniority of our Committee (>60 years) had the final word. Whatever applies to getting older also applies to the late stage of the cycle: you do the same, but more cautiously!

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Five years since Covid hit: a historic crash, and the lessons learned

This week marks the fifth anniversary of the low point of the coronavirus crash. In February and March 2020, global financial markets experienced one of the fastest downturns in history. The coronavirus crisis brought the economy to a virtual standstill and caused a massive decline in stock prices, unsettling many investors.

Our new blog post looks back at the events that led to this crash and analyses what lessons investors can learn from the Covid crash. Because as quickly as prices fell, they were also largely able to recover the losses.

Autumn on the stock markets will be anything but boring

Election campaign, interest rate turnaround, sluggish growth in Europe – there should be no sign of autumn fatigue on the stock markets. What will the coming (and certainly exciting) weeks bring for the markets and how can investors prepare for them?