Italy is about to elect a new president of state. The election that will be held from 24 January 2022 in several ballots is going to determine the successor of the current, 80-year old President Sergio Mattarella, whose mandate expires in February 2022. This was announced by the president of the chamber of deputies of the Italian parliament, Roberto Fico.

Mario Draghi, current prime minister, has indicated he is willing to take the job

Even though in parliamentary democracies the role of the president of state is of limited relevance to everyday politics, this election is of big political significance because the current prime minister of Italy, Mario Draghi, might run for office. Draghi indicated he was willing to take office in his year-end speech.

The 74-year old Mario Draghi is particularly well known as former president of the European Central Bank (2011-2019), when he established a reputation as good crisis manager; he confirmed this reputation as prime minister of Italy.

The big symbolic relevance of the presidential election is that Draghi would not be able to insert himself and his abilities as crisis manager into Italian everyday politics any longer. He would have to step down as prime minister immediately after his election as president of state.

Reform efforts could slow down

In addition to the worries that the current reform efforts in Italy could slow down, there is also the concern that snap elections could be held in Italy, which could result in a move to the right.

According to the most recent polls by the polling firm “Demos”, which were published in the daily newspaper “La Repubblica” at the end of December, these worries are not unfounded. While the “Partito Democratico” (PD) would come out on top again at 21%, the right-wing party “Fratelli d’Italia” (FDI – The Brothers of Italy) would be a close second at 20%. Lega Nord with Matteo Salvini would come in third at 19%. The populist Five Star Movement would have to content itself with 16%.

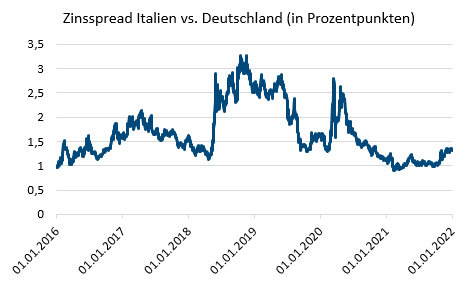

Yields of Italian government bonds on the rise

On the capital markets, this situation is reflected in the drastically widening interest rate differential between 10Y Italian government bonds and German government bonds. Said differential widened from its low of about 0.90% at the beginning of 2021 to its high (especially around the end of 2021) of above 1.35%, despite the massive purchase programme by the ECB.

Italian government bonds account for about 22% of euro government bonds

Italian government bonds account for a significant share of euro government bonds. Therefore, the market participants are closely monitoring the development in Italy, as it has a noticeable bearing on the yields on the government bond market of the Eurozone overall.

Interest rate differential between 10Y Italian government bonds and 10Y German government bonds (in percentage points)

Sources: Refinitiv Eikon, 1 January 2016 – 4 January 2022, Erste Asset Management; in percentage points (1 = 100 percentage points)

The Italian president of state is elected by the joint session of the parliamentary chambers and representatives of the 20 regions. The ballots are secret, and a two-thirds majority is required. It is therefore not uncommon for the presidential election to require several ballots. This time, it will be one ballot per day. After three ballots, a simple absolute majority is sufficient. The election in 1971 holds the current record at 23 ballots and 16 days. The presidential term is seven years.

The centre-right parties Lega, Forza Italia, and Fratelli d’Italia seem to be prepared to support the candidacy of four-time Prime Minister Silvio Berlusconi. Next week we will find out whether Mario Draghi will run for office and whether he will be elected.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Rising inflation expectations and yields: a risk for market sentiment?

Two developments on the stock markets have stood out since the beginning of the year: rising inflation expectations and significant increases in government bond yields. Could market sentiment soon turn frosty in view of this?

Investment View | February 2025

What’s happening on the markets? In our Investment View, the experts of our Investment Division regularly provide insights of current market events and their opinion on the various asset classes.