US interest rates are on the rise. It took the Federal Reserve Bank (“Fed”) twelve months, after the initial lift-off in December 2015, to make the second move, but for two reasons the odds of more frequent rate hikes over the next twelve months have increased. First, the Fed has turned more hawkish and second, inflation expectations have started ticking higher. Only recently, Chairwoman Yellen warned that “waiting too long to begin moving toward the neutral rate could risk a nasty surprise down the road–either too much inflation, financial instability, or both.”

Investors’ concerns

Rising rates are often seen as something equity investors should be concerned about. Concerns are related to

- shrinking valuations due to higher discount rates;

- pressure on earnings reflecting rising interest expenses of leveraged companies; and

- the shrinking gap between dividends and returns from interest bearing assets.

More generally – rising interest rates are also perceived as a bellwether of turbulences in financial markets.

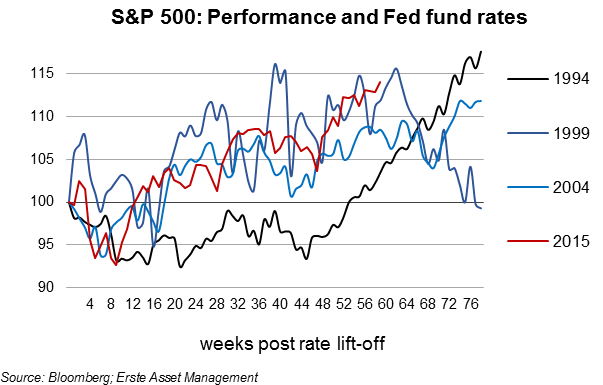

The empirical evidence for those fears, however, is mixed. The last four times, when the Fed started a new rate cycle, there was some pressure on US equities for 2-4 months, but subsequently markets started to recover (except in 1994, when it took a year before the S&P 500 reached its level before the rate lift-off).

Sector winners and losers

As important as the direction of the overall market for equity investors is the impact of the new interest rate environment on investment styles and on the performance of sectors. Based on evidence from the US stock market, using monthly data since 2010, a couple of points are worth mentioning:

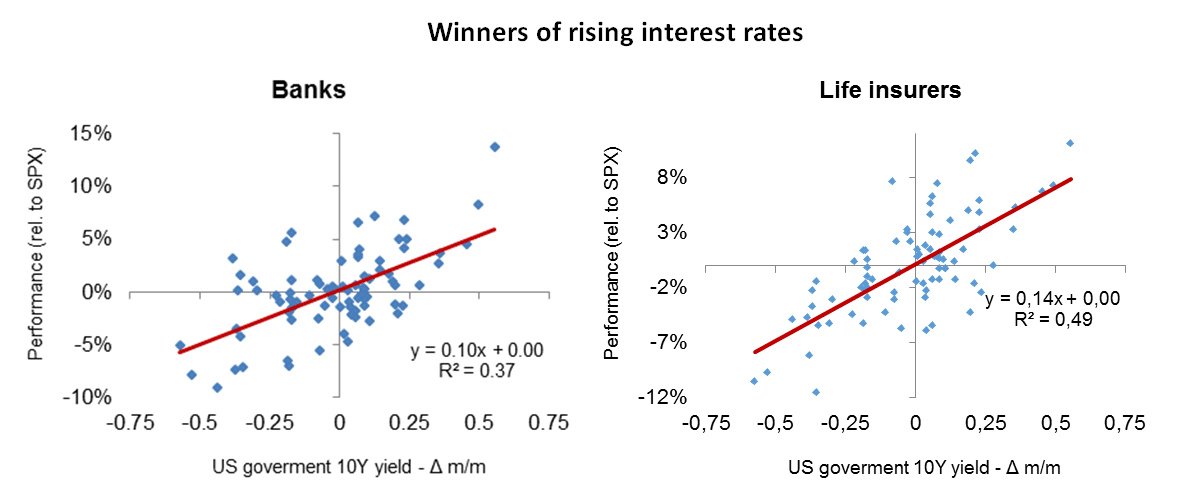

- The key winners in an environment of rising interest rates have been financials, particularly life insurers, banks and diversified financials. There is a strong positive, statistically significant relationship between changes in 10-year treasury yields and the relative performance of these sectors to the broader market.

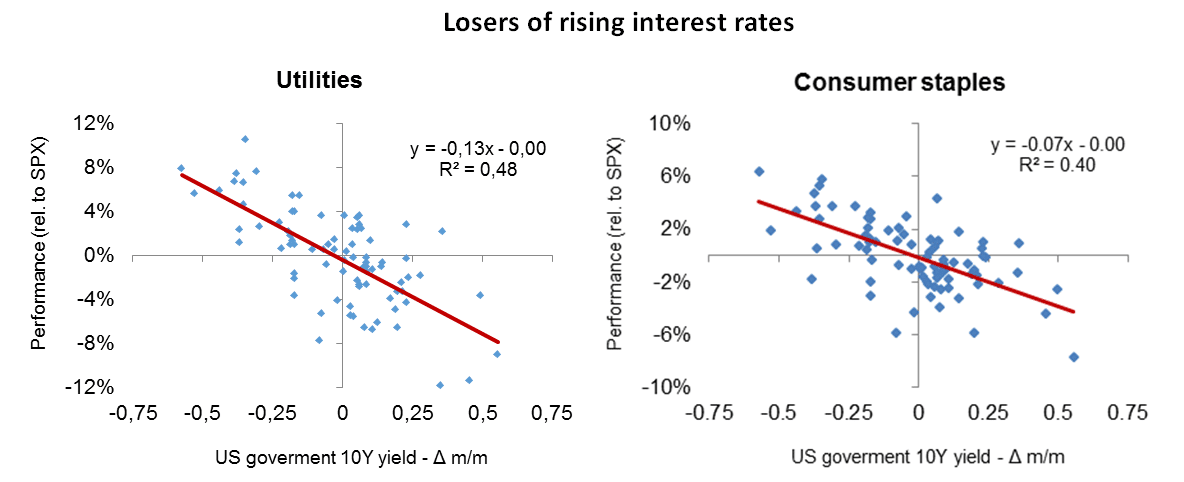

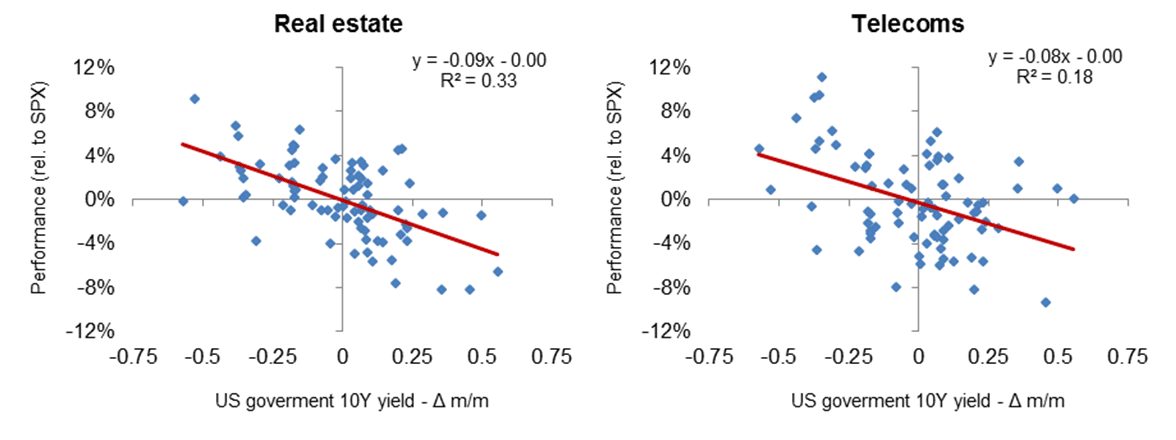

Source: Bloomberg; Erste Asset Management. Relative performance against S&P 500 versus changes in 10y treasury yields, Jan 2010 – Jan 2017. - On the losing end are utilities, consumer staples, real estate and telecoms. The negative linkage is strong and statistically significant. It reflects the fact that these sectors mostly consist of high-dividend stocks, which are losing some of their appeal as interest-bearing assets are becoming more attractive. In addition, most companies in these sectors are also asset-heavy, financed by long-duration liabilities, and therefore interest-rate sensitive.

Source: Bloomberg; Erste Asset Management. Relative performance against S&P 500 versus changes in 10y treasury yields, Jan 2010 – Jan 2017. - There are a number of sectors, which seem to outperform in an environment of rising rates (e.g. capital goods, materials, energy) or underperform (health sector). However, the links are statistically not significant and too weak to be of any use for portfolio decisions, even if investors were confident enough to predict the direction of interest rates.

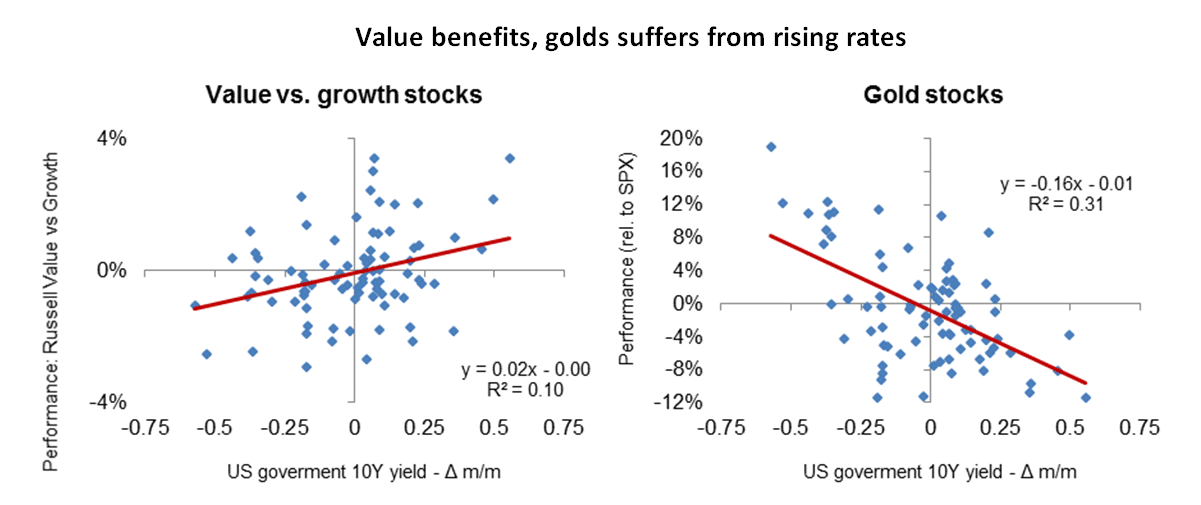

The consequences of changing interest rates for equity investors extend beyond pure sector effects. For example, data suggest that during periods of rising interest rates

-

- value stocks (typically stocks that trade at low valuations) tend to outperform growth stocks (expensive stocks expected to grow above average);

- cyclical stocks tend to outperform defensive stocks (which partly just reflects the sector effects described above);

- emerging markets tend to underperform stocks in developed markets, and

- gold prices are affected negatively because rising interest rates increase the opportunity costs of holding gold. Consequently, physical gold and gold stocks tend to underperform the broader equity markets during periods of rising interest rates.

Source: Bloomberg; Erste Asset Management. Relative performance against S&P 500 versus changes in 10y treasury yields, Jan 2010 – Jan 2017.

Health warnings

The charts above need to be seen with a grain of salt. They show some empirical regularities but before using them as an input in investment decisions more, deeper statistical analysis would be required.

One of the main caveats is that the statistical properties of the empirical relationship between interest rates and stock performance are weak, i.e. typically changes in interest rates explain only a small part of the variability of stock returns.

In addition, the relationship between interest rates and stock returns – like most empirical patterns in financial markets – is not stable. During periods of financial stress and/or aggressive monetary tightening, supposedly well-established linkages often break down and winners of rising rates, particularly financial stocks, could turn into losers.

Moreover, the links between interest rates and stock returns shown above may just reflect the simultaneous response of both variables to other economic developments such as growth and inflation expectations. As Ed Leamer, a renowned econometrician, once stated: “Correlation is in the data but causation is in the mind of the observer”.

Finally, the slope of the yield curve matters. If, for example, rising rates are accompanied by a flattening of the curve, both positive and negative effects of interest rate movements are usually mitigated.

Bottom line: Odds have increased that US interest rates will increase. While the new normal will likely be lower than historical levels, and the spill-over to Europe will be delayed, investors need to adapt to a new environment. Rising interest rates go hand in hand with a rotation of sectors and investment styles. It seems likely that financials and other cyclical sectors will continue to enjoy some tailwind, while non-cyclical consumers, utilities and real estate will be facing headwinds. This said, none of these developments will follow a mechanical, predictable pattern offering easy profits.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.