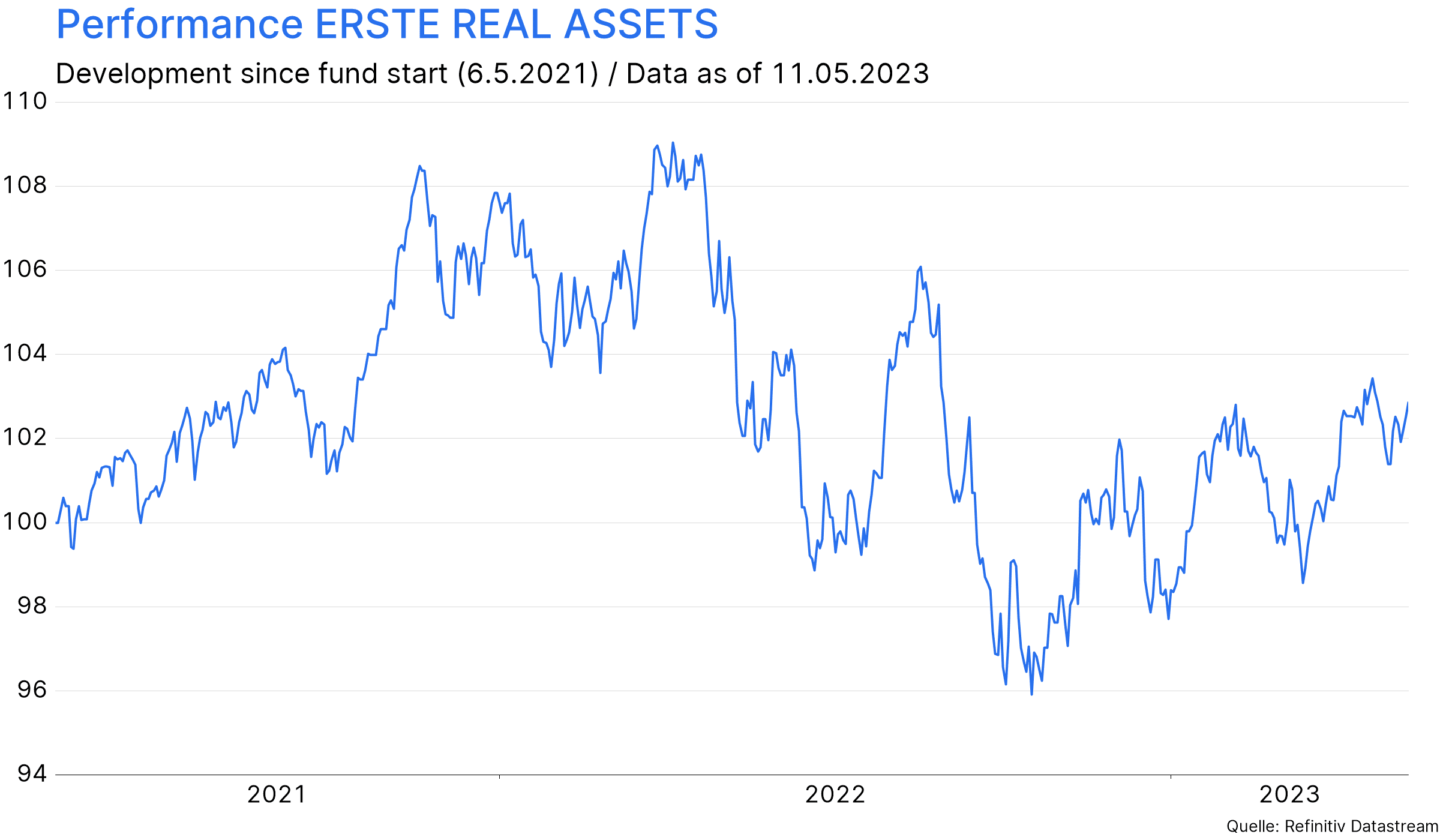

With the ERSTE REAL ASSETS mixed fund, investors can invest in real assets – and have indeed been doing so for two years now. As early as May 2021, when the fund was launched, many people were concerned about rising inflation. Since then, inflation has gained further momentum, and the interest rate environment has also changed completely.

On the occasion of the fund’s two-year anniversary, Philip Schifferegger, fund manager of ERSTE REAL ASSETS, is taking a look at the current market situation in an interview. He also explains why the fund is well equipped for both positive and negative market phases.

Please note that investments in investment funds involve risks as well as opportunities.

The pandemic-related supply chain disruptions and the outbreak of war in Ukraine have caused inflation to rise sharply over the past two years. Do you think that inflation has peaked yet?

High inflation usually occurs in waves, the peaks of which may be several years apart. The supply bottleneck for goods caused by the pandemic initially fuelled inflation, supported by expansionary monetary and fiscal policies that in combination kept demand high. Economists and central banks initially classified this development as temporary, but energy prices then gave it a whole new dynamic.

In a condensed definition, the economy is nothing other than the transformation of energy. Without energy, we could not even record and publish this interview. If energy prices multiply within a very short period of time, this naturally has a massive impact on the price structure of all goods and services offered.

But such a dynamic price development is usually not long-lasting, or to use a metaphor: as soon as you see the left side of the Eiffel Tower, the right side is not far away. The energy price peaked in June 2022; now, energy is trading much lower. That means, to answer your question, yes, we have now passed the energy price-induced peak of inflation.

We do not know whether the next wave of inflation will again be energy-induced or perhaps wage-induced. We will only know in retrospect. In any case, the central banks have reacted and raised key-lending rates significantly over the past twelve months. In the USA from 0.25% (upper limit) to 5.25% most recently. The question is whether this is enough. Normally, sustained positive real interest rates (N.B. key-lending rates minus inflation) have an inflation-inhibiting effect. In the USA, with an inflation rate of currently 5%, we have de facto exceeded the neutral threshold, while in the Eurozone we are still a long way from it.

Why does it pay off for investors to invest in real assets, especially in times of high inflation?

I would not call the ERSTE REAL ASSETS an anti-inflation investment. That would be a bit presumptuous. ERSTE REAL ASSETS is a broadly diversified portfolio that is well equipped for both positive and negative market phases due to its structuring. As a client, I don’t need to constantly worry about whether I am currently invested in the right asset class or not. The fund does not engage in short-term market timing, but sticks to its strategic allocation weights.

We have equities for the good times, and gold for the times of crisis. In addition, we hold real estate and commodities in the portfolio, which have historically proven to be a good investment in an inflationary environment. All four asset classes together allow for balanced risk diversification and this also in times of higher inflation.

“We have equities for the good times, and gold for the times of crisis. In addition, we hold real estate and commodities in the portfolio.”

Philip Schifferegger,

Fund manager ERSTE REAL ASSETS

How are you currently positioned in the fund, and what has changed in terms of positioning in the past two years since the launch?

The core of the investment has remained unchanged. We constantly hold around 50% equities and around 30% gold; but we have made adjustments to the real estate allocation. We have reduced the proportion of open-ended real estate funds and reallocated the freed-up assets to global real estate shares and infrastructure shares. At the same time, we have added around 10% commodities to the portfolio. In this way, an even broader diversification of the fund was achieved.

In the commodities segment, we focus on those industrial metals that are needed for the energy transition, such as copper and nickel. We expect strong demand potential there. An investment or speculation with food is of course excluded.

What do you think could be in store for us with regard to the economy and the markets this year? In your opinion, how should investors position themselves at this point?

It usually takes 12-18 months for interest rate hikes to take full effect. The USA started raising interest rates last year in March. This means that we are now in the thick of it, and the first effects are visible (Keyword US banking crisis). The economic momentum is expected to weaken as the year progresses. Whether it will be a mild or severe recession, we do not know.

In our view, a mild economic downturn is already priced into the market. But in the event of a profit recession, we should definitely expect unpleasant price markdowns.

On the interest rate front, we have reached the forecast level of the key interest rate of 5.25% in the USA. The market already envisages lower key-lending rates for the end of 2023. And lower interest rates are positive in themselves, both for equities and for gold.

Philip Schifferegger is fund manager at Erste Asset Management. He has worked in asset management since 1997, holds a master’s degree from the Vienna University of Economic and Business Administration and is a chartered financial analyst (CFA).

At one glance

ERSTE REAL ASSETS invests mainly in the asset classes of equities (including a focus on infrastructure), commodities and precious metals, real estate, and inflation-linked bonds, all of which form the “real values” focus. All important information about the fund can be found here.

Risk notes according to 2011 Austrian Investment Fund Act

ERSTE REAL ASSETS may make significant investments in investment funds (UCITS, UCI) pursuant to section 71 of the 2011 Austrian Investment Fund Act.

Advantages for the investor

- Investment focus on real assets

- Opportunity to achieve long term capital appreciation

- The broad investment in a vast array of assets allows for a significant degree of risk diversification in the fund, which may reduce the risk of capital losses.

- Investment funds are separate assets

Risks to be considered

- The assets in the fund may be subject to considerable price fluctuations.

- Due to investments denominated in foreign currencies, the net asset value of the fund can be negatively impacted by currency fluctuations.

- Alternative investments involve a higher level of risk

- Capital loss is possible

- Risks that may be significant for the fund are in particular: credit and counterparty risk, liquidity risk, custody risk, derivative risk and operational risk. Comprehensive information on the risks of the fund can be found in the prospectus or the information for investors pursuant to § 21 AIFMG, section II, “Risk information”.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.