In recent weeks, the scenario of a recovering global economy has become more likely. In line with the textbook, share prices have been up, and the prices of safe government bonds have been down.

In addition, the US dollar, inherently often anti-cyclical, has depreciated against a currency basket. In this blog entry, we want to discuss the reasons for this development and the necessary conditions for its continuation.

[post_poll id=”8690″]

Positive developments:

- he outlook on an agreement in the conflict between the USA and China has improved. While said agreement will probably not affect all areas of conflict (trade, technology, finance, currency, patents), both countries might agree on a truce. This means that the downside risks (tail risks) for the global economy have decreased.

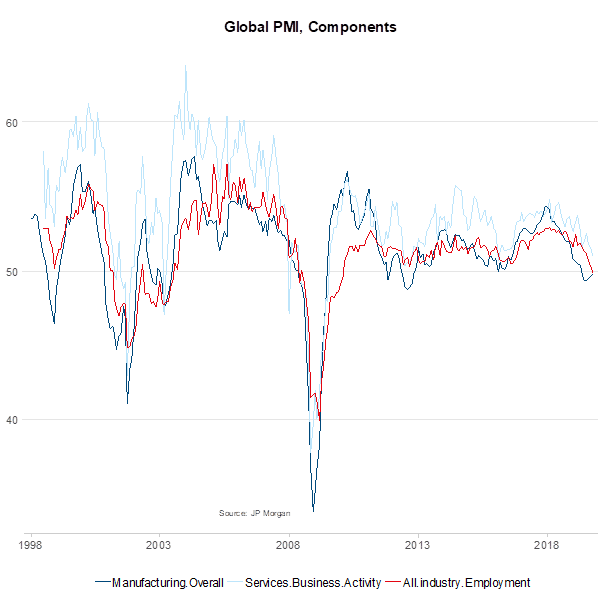

- The signs of stabilisation in the weak, i.e. hardly growing sectors of the global economy have increased. This applies to industrial production as well as corporate capital expenditure. The global purchasing managers’ index in the manufacturing sector is an important indicator in this context. In October, it recorded its third consecutive increase. The indicator that has recorded the most significant decline since the beginning of 2018, i.e. the sentiment in the business sector, has shown signs of bottoming out.

- Indeed, sentiment indicators have generally fallen more significantly than the indicators rooted in the real economy (production, consumption). Constructive events with regard to global and geopolitical uncertainties would have the power to set off a trend reversal.

Monetary policies have become looser this year. This includes rate cuts in many countries and a trend reversal in money supply, both in the USA and in Europe.” Gerhard Winzer, Chief Economist Erste Asset Management (c) iStock

- The central banks have re-embarked on (net) purchase programmes again and are buying government bonds. While the Federal Reserve only buys short-term T-bills, the effect of rising liquidity still feeds through to the market. The result is a looser financial environment (i.e. financial conditions), which means that many asset prices have increased over the year. This supports economic growth, albeit at a considerable time lag.

- Fiscal policies have turned slightly looser as well. The relevant indicator in this case is the federal budget exclusive of interest payments, adjusted for the effects of the economic cycle in relation to the potential output of the economy. From 2018 to 2019, the aggregate figure for the OECD area declined by 0.4 percentage points to -1.4%. This has a marginally positive effect on economic growth.

- As far as the credit environment is concerned, the development in China stands out. From the beginning of 2016 to the end of 2018, the credit impulse – i.e. the change in credit growth in relation to economic growth – was negative. On top of the increased geopolitical uncertainty and the reduction of global money supply, this was probably one of the main reasons for the weakening of global economic growth. Since the beginning of 2019, the credit impulse in China has been positive, albeit only slightly.

Please Note: Past performance is not indicative of future developments. Source: Erste Asset Management

These positive developments, however, are only strong enough to ward off a further weakening of global economic growth. They will probably not suffice for a trend reversal. What developments are necessary for a trend reversal, then? Of course, the aforementioned positive factors that have already occurred have to remain in place. There are three main pillars in particular:

- The negative spillover effects from the weak to the currently strong sectors of consumption and services have to remain limited. On this front, the news flow is not particularly positive. Employment growth has already weakened, and the employment component of the purchasing managers’ index suggests a further decline. This means an erosion of the most important pillar of economic growth, i.e. private consumption. This means it is too soon for a trend reversal. Economic growth will probably remain low (i.e. below potential) for a few quarters.

- The assessment that the loosening of the monetary policy was sufficiently effective to stabilise the weakening of economic growth may be right. However, the central bank in the USA is signalling an end to its rate cuts (in total, 0.75 percentage points to a band of 1.5-1.75%). This is tantamount to a higher hurdle for the other central banks to cut their key-lending rates. In other words: the global interest cut cycle is coming to its end. At the same time, Chairman Powell from the Federal Reserve has made it clear that the hurdle for rate hikes is equally high. The Fed might think about going down that road in the event of a sustainable increase in inflation, and less so in case of higher economic growth. Conclusion: the monetary policies have to remain loose.

- Company earnings have to grow again. In recent months, company earnings have fallen significantly worldwide. At the moment, they are stagnating. This has to do with revenue growth, which has declined just like nominal economic growth, and with the accelerating growth rate of unit wage costs.

- Due to the still tight labour market, many countries have seen their wage growth speed up. This is generally positive. However, since productivity growth is lower, unit wage costs have increased. Theoretically, this can translate into pressure towards higher consumer price inflation or on profit margins. The latter scenario has manifested itself in recent quarters. In a recovery scenario, the pressure on profit margins in the corporate sector falls, probably on the back of higher revenue growth.

Conclusion: the increase in risky asset prices is increasingly less due to rate cuts by central banks (as this cycle is coming to an end). Rather, it is based on the falling tail (downside) risks, driven by the outlook on a mini deal between the USA and China. For a trend reversal of economic growth, the negative spillover effects have to remain limited, and the central bank policies have to stay loose. At the same time, company earnings will have to pick up. This may take a few more quarters.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.