Ahead of the upcoming reporting season, several negative factors dominate the markets. Tamás Menyhárt, Senior Fund Manager at Erste Asset Management, sums up the stock market year so far and shares his views on the further development.

The first half of the year was a very bad period for the stock markets. The mixture of negative factors such as war, inflation and growth concerns sent major indices such as the S&P-500 into a bear market. What are the chances of a recovery in the second half of the year?

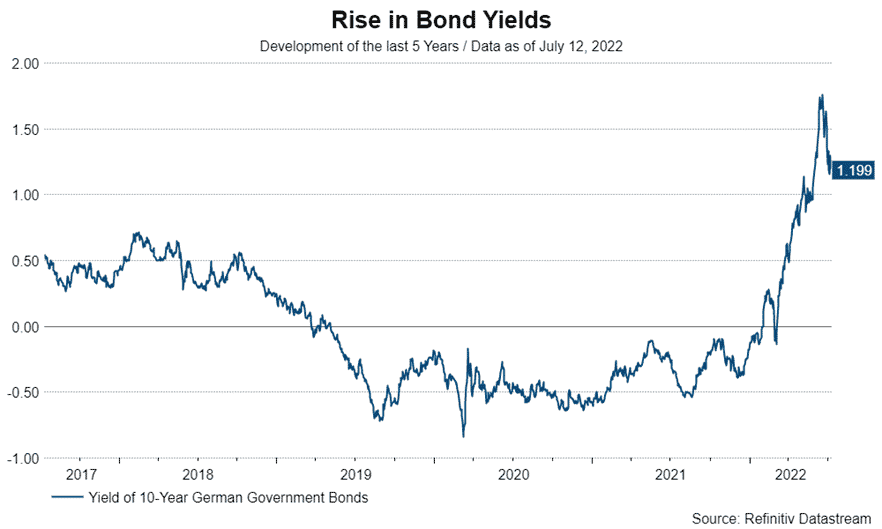

Currently, the prospects for equities in the second half of the year are mixed. Major indices experienced significant declines since the start of the year. The negative price development was mostly driven by the sharp increase in bond yields globally, which is a byproduct of central banks turning more hawkish, as they try to fight off inflation. During the first six months of 2022, the US 10-year yield roughly doubled to above 3% and in Germany, 10-year yields turned positive for the first time since May 2019.

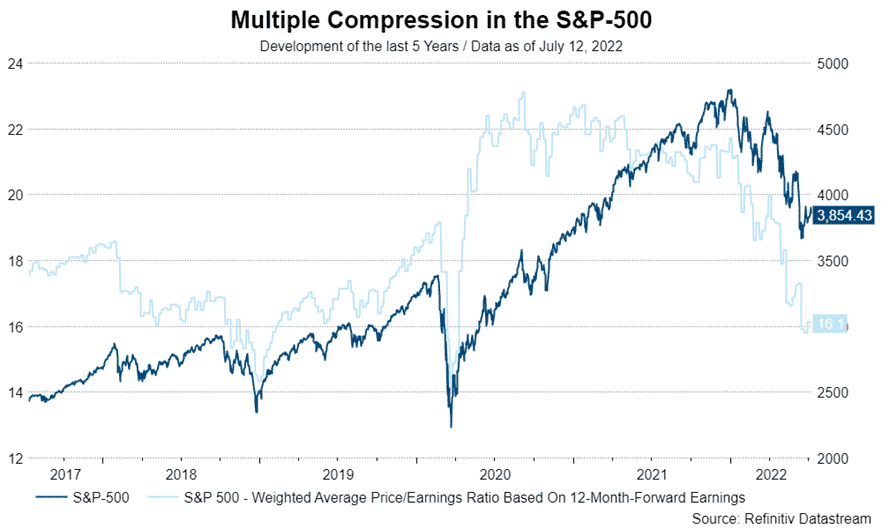

Higher government yields increase the discount rate used for stock valuation, meaning that equity multiples like the price-earnings-ratio (P/E) get compressed in such a scenario. Year-to-date, the losses on equity markets were almost entirely attributable to this effect. The S&P-500 for example kicked off the year at a P/E above 21 times forward earnings, which then fell to below 16 at the end of June – a multiple compression of almost 25%(!). However, the index was down “only” 20.6% in the first half of the year, as earnings estimates actually increased during that period.

What we can say is that valuation multiples look a lot healthier now, than they did a couple of months ago. If one takes a look at recent crises like the Covid-shock or the Fed mistake in 2018, we can observe that there is still some downside left if sentiment were to deteriorate further, but overall, multiples have adopted to the higher yield environment.

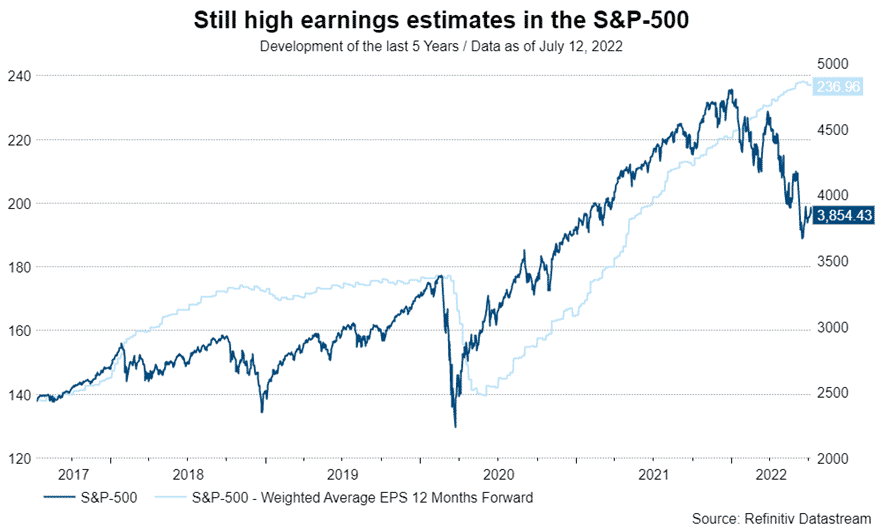

The bigger risk going forward lies with analysts potentially trimming their estimates. Currently, consensus expects earnings and revenues for the 500 largest US-companies to increase by more than 10% in 2022. Recently, economic data pointed towards a slowdown in the world economy, which increases the chances of lower earnings.

To sum up, the good news is that a large part of the yield-driven valuation adjustment is already complete. On the negative side, the risk of lower earnings prevails. If the Fed in the end manages to achieve a soft landing – that means bringing down inflation without causing a recession – the stock market has a decent base to start rising from again. Also, if the market judges that a weaker economy will lead to lower yields going forward, then some of the negatives from lower corporate earnings can be offset by expanding multiples. The latter might also be helped by a sudden end to the war in Ukraine, as then market sentiment could be expected to improve rapidly.

We expect more visibility on these issues in the second half of the year. Putting everything together, I think it is too early to call the bottom for equities yet. Nevertheless, for investors with a longer time horizon, it makes sense to start adding equities to their portfolio at current levels, as valuation became a lot more attractive after the recent pullback.

Against the backdrop of a turbulent stock market year so far, we are in for a particularly interesting reporting season. This week, the major banks in the US will start with their figures. Do you expect the growing fear of a recession to be reflected in the corporate figures for the second quarter?

Expectations for Q2 results have come down recently and the market currently expects S&P-500 earnings to grow by roughly 4%. Therefore, an earnings recession for the quarter is not so much the issue. As is usually the case in such uncertain times, investors will pay more attention to management`s outlook and guidance than to reported numbers.

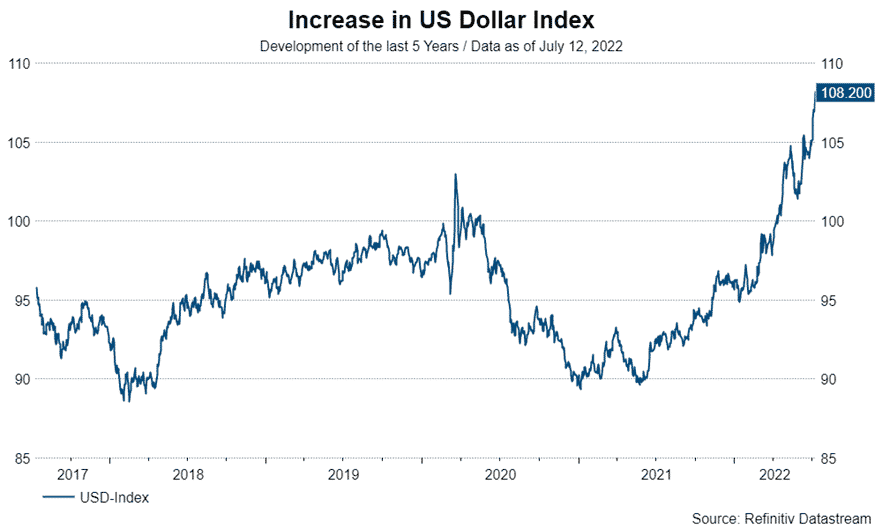

As of late, we could observe that CEOs of various companies switched to a less optimistic tone regarding the business environment. A headwind for companies, which report their numbers in US-Dollar, comes from the strong greenback, which leads to a lower dollar-value of international revenues. The Dollar has appreciated to levels not seen in decades, as investors fled to the safe-haven currency in light of an uncertain economic environment and a hawkish Fed.

Market behavior tells us that the focus has now shifted from inflation to recession, which became most apparent in the recent pullback of various commodity prices. Our expectation is that management commentary during the earnings season should also reflect this trend. Overall, we do not think that fear of recession will play a big role in reported numbers, but it will certainly have its effect on the near-term outlook of corporates.

Bond yields have risen significantly since the start of the year, making fixed-income securities a more attractive investment again. Is the time of TINA, i.e. “there is no alternative” (for equities) over?

Clearly, the era of record-low yields and low inflation seems to be over for now. My judgement is that TINA is over, and that this year`s market declines were mostly a reaction to exactly this. TINA got priced out, bonds can compete again with different asset classes as yields rose, and therefore investors demand a higher earnings yield – which is the inverse of P/E – in order to take on the risks associated with owning equities. In the end, this led to the compression in valuation which we have touched upon.

It would be wrong, however, to jump to the conclusion that equities are no attractive investment anymore. Historically, equities have been one of the best asset classes to offer a hedge against moderate inflation. One of the reasons why dividend-paying stocks have done relatively well this year is that investors expect the payouts of these companies to match or exceed inflation, and over time, stock prices should also go up. These features are not present in the case of fixed-income instruments, as is implied by its name. Also, one should not forget that even though bonds now do offer higher yields, these are still mediocre at best when adjusted for current inflation rates.

Compared to the previous decade, the end of TINA will make the environment for stocks a more difficult one, but equities are far from being done.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Sovereign defaults and their debt restructuring

A glance at history shows that it is not unheard of for a state to go bankrupt. How does an entire country actually go bankrupt, what are the consequences and how do you react to this in fund management? Fund manager Felix Dornaus explains this in his blog post.