Economy activities improved

As the „first in, first out” country of the COVID-19 crisis, China is gradually returning to normal. The April activity numbers indicate that China’s domestic economy has been resilient and has continued to recover from the COVID-19 disruption.

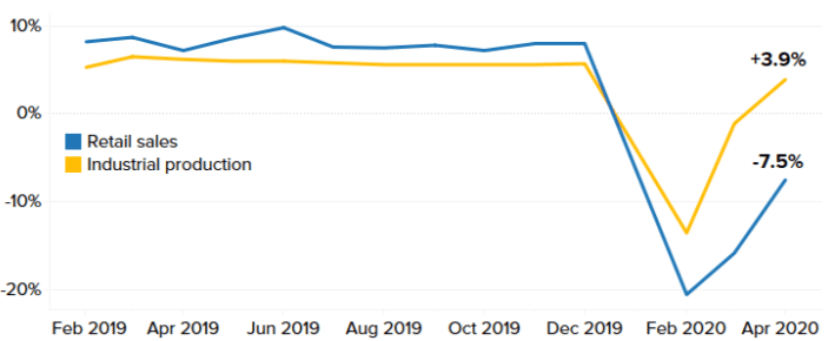

Industrial production rebounded to a 3,9% annual growth rate in April after collapsing 1,1% in March. Exports rose 3,5% from a year earlier, reversing a decline of 6,6% in March. Fixed-asset investment and retail sales continued to fall but at a slower pace.

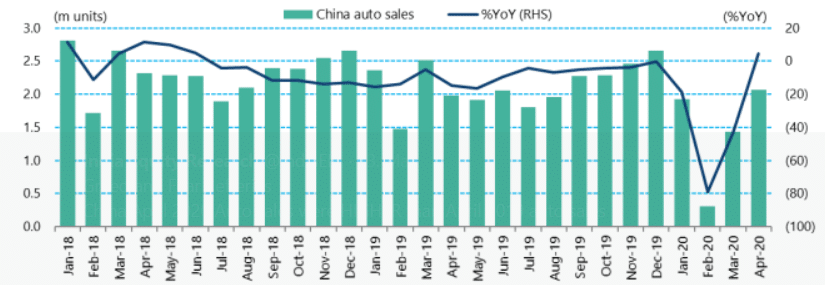

The pattern of gradual return to normal is also reflected in the Chinese auto market and the residential property market. Auto sales nearly doubled and rose another 50% MoM in March and April, respectively, after falling 75% in February. This recovery took auto sales back above last year’s levels in April. China’s home prices and housing activities picked up momentum too. According to the National Bureau of Statistics (NBS), 70-city home prices on average rose 5,2% YoY in April. Housing market transactions have rebounded notably, returning to around historical average level. Real estate investment returned to positive annual growth of 6,9% YoY in April, leading the recovery in overall fixed-asset investment.

Together with steady activity recovery labor market conditions improved notably in April. An update of the labor report from the NBS shows unemployment rate ticked up to 6.0% in April, but the under-employment rate (employed but not working) dropped dramatically from 18.3% at end March to 3.5% at end April (or from 76 million to 15 million).

V-shaped recovery for industrial production and retail sales

Source: National Bureau of Statistics China Note: Past performance is not indicative of future development.

Headwinds remain

Beside a potential second wave of COVID-19 and the decline in global demand, serious escalation of US-China tension is among the biggest downside risks to China’s economy this year.

The coronavirus pandemic has reignited tensions between the United States and China. As the Phase I trade deal reached on January 15th was only a temporary solution, the re-escalation of US-China tension is not surprising. Fundamental changes in the US-China relationship led the bilateral confrontation in trade, technology, finance and geopolitics issues, especially in the US election year.

A place caught in crossfire is Hong Kong. During the National People’s Congress China announced the plan to impose a Hong Kong National Security Law. The new law will ban secession, subversion of state power, foreign interference and terrorism. A similar law was proposed in 2003 but was abandoned after mass protests. The surprise move by Beijing renewed concern on Hong Kong’s uncertain future and risks further exacerbating tension with the United States.

Auto sales have largely recovered

Source: China Association of Automobile Manufacturers Note: Past performance is not indicative of future development.

Policy outlook

China introduced the first batch of policy responses to the COVID-19 crisis in February. On the fiscal side, China has announced about 3,5% of GDP worth of stimulus. The size is relatively modest compares to other major economies and China’s own ~10% of GDP stimulus during the Global Financial Crisis.

On the monetary front, it included liquidity injection, Required Reserve Ratio (RRR) cuts and cuts of the lending rate and key financial market interest rates. This is supplemented by increased regulatory forbearance to help corporates survive the temporary disruption. Nonetheless, the policy support needs to be bolstered, if China wants a stronger recovery in the second-half of this year and next year.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.