Bitcoin has achieved an average performance of 142% p.a. in the past five years. In the past four months alone, it has gained 190%. The coin set a new all-time high on 10 January 2021 before entering a healthy correction. Some criticise the high level of volatility but forget about the potential. Many wonder whether, after the dramatic increase, one could still enter the market or whether that ship has sailed. In the following I therefore want to discuss the reasons that have led to the rally of Bitcoin in recent months.

1. Halving

The blockchain system of Bitcoin is based on a race between the so-called miners, where blocks are created by transactions and a so-called hash is produced by an encryption method that has to fulfil certain criteria. The calculation takes on average ten minutes. The first miner to generate a valid block receives all transaction costs and a reward of 6.25 new bitcoins. Once a block has been attached to the chain (blockchain), the race begins anew. However, before that, every participant has to update the entire database to the status quo. The reward is halved every four years. This way, few and fewer bitcoins are entering the market. Constant demand and half the supply will automatically result in an upward pressure on the price. Last May, another halving took place (the third in the history of Bitcoin), and three to four months later (i.e. September 2020) a new upward trend set in that is still ongoing.

2. Regulatory progress

Institutional investors in particular need legal certainty and clarity about their investments. The proposal by the EU Commission in September 2020 to regulate crypto assets has contributed significantly to said certainty and clarity, although at this point, we are still only talking about a proposal and not about a law. Still, the EU will regulate the market on the basis of MiCA (Markets in Crypto Assets), a regulatory framework that somewhat emulates MiFID. These measures should help Bitcoin shake off the image of being a money laundering currency. Even today, Interpol monitors all Bitcoin transactions on the blockchain and can take steps to prevent criminal activity.

3. QE, ZIRP, and high government debt

The central banks have reacted to the corona crisis by massively expanding the money supply (QE – Quantitative Easing) and at the same time cutting interest rates further (if possible) towards zero with the intention of leaving them on that level in the foreseeable future (ZIRP – zero interest rate policy). Many states have also prevented the economy from collapsing by passing enormous emergency packages. As a result, the debt of many countries has increased above 100% in terms of GDP.

These measures were definitely necessary, but more and more investors worry about possible inflation resulting from them and have started moving into tangible assets. Bitcoin benefits from this trend, given that its money supply is capped at 12 million units and it cannot be changed by any institution. This means that to many investors, Bitcoin is a way to protect themselves from inflation in the long run.

4. Institutional investors opening up to Bitcoin

Given the zero-interest rate policy, many institutional investors are also desperately looking for yield. An increasing number of them has come across Bitcoin in their search. While Bitcoin was created as currency, it has developed towards a financial asset. Although its volatility is high, adding a small percentage (1 to 3%) to a traditional portfolio can make sense. Due to the low correlation with other asset classes, it does not increase the total risk of the portfolio by much, while the yield can be noticeably higher. This is also the conclusion of Fidelity and a prominent piece of research it has produced. This means that Bitcoin has developed from a currency to an asset and has been increasingly often compared with gold. Some have even called it “Gold 2.0”, although Bitcoin actually has many advantages such as easier storage and transportability.

An indicator of the fact that institutional investors are dominating the market activity is the jump in assets under management of bitcoin trackers that are largely bought by this segment of investors. An example is the Grayscale Unit Trust, which boosted its volume from US-Dollar 2bn to US-Dollar 25bn within one year.

5. Investment banks launching research and forecasts

An increasing number of investment banks have started to cover cryptocurrencies, above all Bitcoin, and are trying to support the rising demand among institutional investors with research. So far, no generally acknowledged valuation model has emerged as consensus. However, please let me present three approaches underneath that are currently among the analysts’ favourites.

- Mining cost (production costs)

Here, the price of Bitcoin is put in relation to the production costs (electricity, hardware). At the moment, the ratio is 2.8x, which – given the average of slightly less than 2x – makes Bitcoin overvalued.

- Comparison with gold

In a research report[1], JP Morgan subjected Bitcoin to a comparison with gold. The analysts think that Bitcoin could in the long run match the volume of gold held by private investors in bullions, coins, ETFs. (N.B. that excludes the holdings by central banks.) This results in a theoretical price of USD 146,000. However, the investment house points out that this is a long-term estimate and that the value can only be reached once the volatility of both assets have converged.

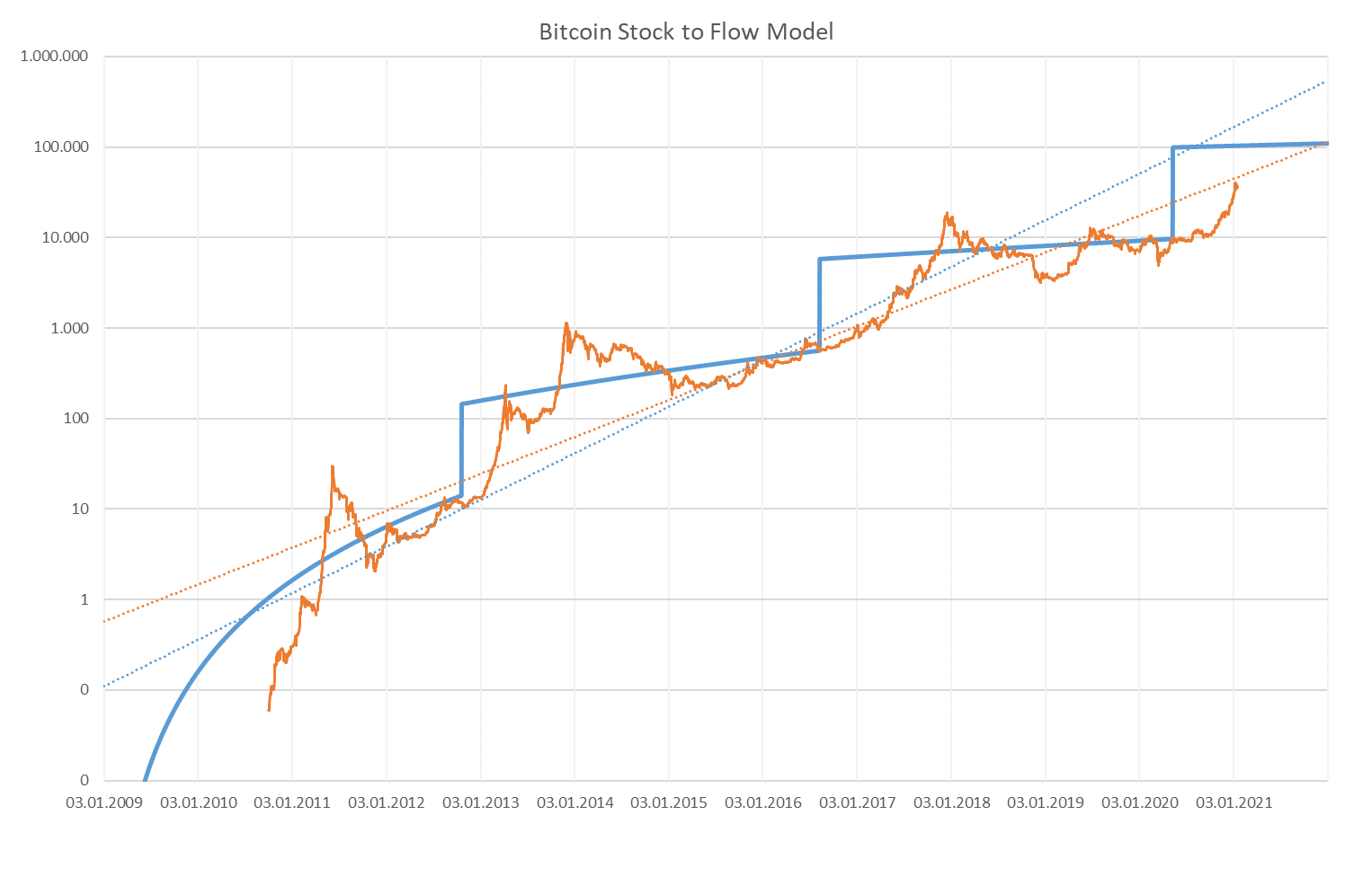

- Stock-to-flow model

The stock-to-flow model is very popular and has been quoted by numerous analysts. It is a valuation method often resorted to for commodities. Here, the amount of Bitcoin that is created newly every year is put into relation to the existing volume. Since the supply is halved every four years, there is an according jump in fair value. According to this model, the price of Bitcoin would have to settle slightly above USD 100,000 by the next halving in 2024. I have reconstructed the model for illustration purposes below.

In addition to investment banks, numerous specialised analysts cover Bitcoin. An example is Swissrex and its forecast model. Here, an adjusted stock-to-flow model is used, as a result of which the forecasts are slightly lower.

Source: Bloomberg, own calculations

6. Traditional platforms facilitate purchase of Bitcoin

The company Paypal, an important payments systems company, has announced it will offer the purchase and trading of Bitcoin on its platform (launch date USA: 2020). In addition, it wants to allow its users to pay invoices by Bitcoin. The vendor still receives US dollar, but Paypal exchanges Bitcoin for a fiat currency in the background. We have also seen online brokers (e.g. Swissquote) mushrooming where users can trade Bitcoin. No private keys have to be held and safeguarded anymore. This allows for a less technologically savvy target group to enter the Bitcoin market.

7. Conclusion

The market for cryptocurrencies is dominated by Bitcoin and Ethereum. The total volume already exceeds USD 1,000bn and has thus made it onto the institutional investors’ radar. However, cryptocurrencies do not only come with opportunities but also with risks for investors. Above all, the extremely high level of volatility springs to mind. Bitcoin is a young, largely unregulated form of investment with a lack of transparency. In many respects, Bitcoin also has to work on correcting its image. Many regard it as money laundering instrument and as currency of choice in the Darknet. At the same time, regulation and the executive branch have contributed a lot to the status quo, where criminals are now moving on to cryptocurrencies with a higher level of anonymity (e.g. Monero).

Although Bitcoin was conceived as currency without intermediaries, it has turned into its own asset class. We expect Bitcoin to become increasingly part of asset allocation and management. Large investment companies such as Fidelity or BlackRock have already taken first steps. Some companies have also started to exchange parts of their cash holdings into Bitcoin.

[1] JP Morgan, Flows & Liquidity, 4 January 2021

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

US elections: are the billions of investments in green technologies at risk?

Two years ago, the USA initiated its energy transition with the Inflation Reduction Act. This was followed by billions in subsidies and investments in renewable energies. What will happen to the Act if Donald Trump makes a comeback to the White House? Is the “Green Rush” in danger of coming to an end?

The markets in a gold rush – overheated rally or brilliant opportunity?

Gold on the rise: Will the rally continue and what opportunities are still available for investors? Read today’s blog post to find out what is behind the development of the gold price and why shares in the gold sector might also be worth a look.