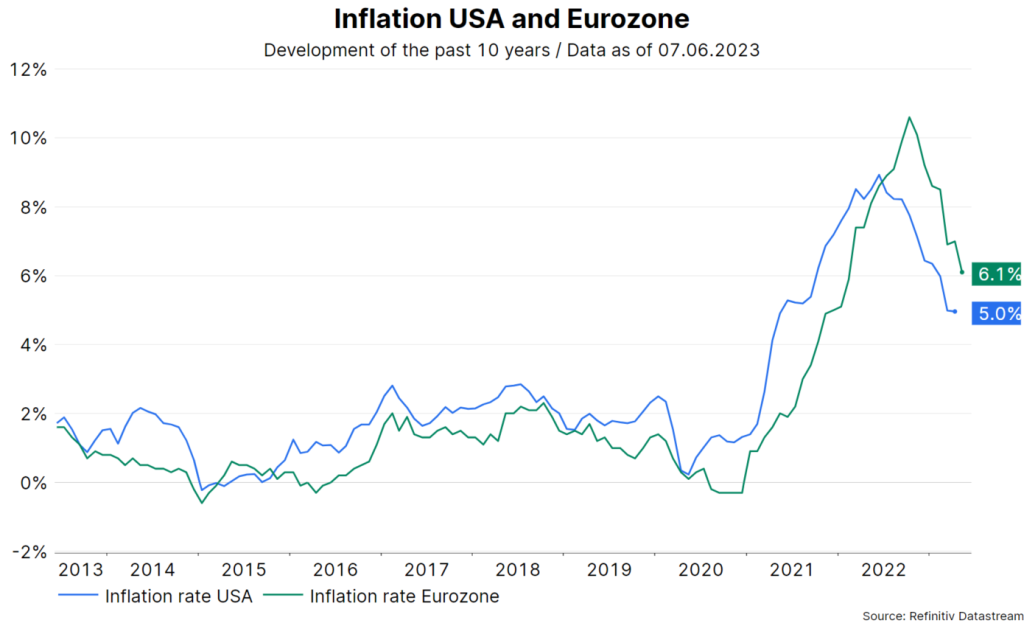

On the surface, we have seen several positive events recently on the economic data front. According to the flash estimate, consumer price inflation in the Eurozone fell in May, from 7.0% to 6.1% year-on-year.

Source: Refinitiv Datastream; Note: Past performance is not a reliable indicator for future performance.

Year-on-year unit labour cost growth in the USA was also revised downwards from 5.8% to 3.8%. Both these factors fuel optimism for an imminent pause in the rate hike cycle in the US and in the Eurozone. The Fed’s central bank decision is due next Wednesday, followed by the ECB’s interest rate meeting on Thursday.

In addition, a technical bankruptcy of the USA has been averted by the postponement of the national debt ceiling of two years. The outstanding piece of economic news of the week, however, was the extraordinarily strong employment growth in the USA. That being said, the risk of recession, the main enemy of risky asset classes like equities, remains at an uncomfortably high level.

Labour market data indicate strong employment growth

Last Friday, the labour market data were published in the USA. Traditionally, the focus here is on newly created jobs in the non-farm sector, i.e. the so-called nonfarm payrolls. At an increase of 339,000 in May, the figure came out far above expectations, which had been 195,000.

Under normal circumstances, strong employment growth would suggest an economic boom. But GDP adjusted for inflation grew by only 1.3% quarter-on-quarter (and annualised) in the first quarter. A similar figure is expected for the current quarter.

Employment growth also exceeds economic growth in other countries and regions, which means a decline in labour productivity. In fact, US productivity shrank by 0.8% year-on-year in Q1.

Reasons for the significant increase

Pandemic-related distortions are probably an important reason for the surprisingly high employment growth. In February 2020, the total number of employed people amounted to roughly 152 million, in May 2023 to around 156 million. The increase of four million employees sounds a lot, but it translates to an average monthly increase of only 104,000.

From 2010 to February 2020, the average monthly increase was 184,000. Like many other sectors, the labour market is undergoing a process of normalisation, i.e. an adjustment to the long-term path.

Less potential on the labour market

At 60.3%, the portion of the population in employment in the US is still below the February 2020 figure of 1.2%. This is due to the participation rate, which represents the share of the labour force (employed and unemployed) in terms of total population. At 62.6%, this also still remains below the value of early 2020, which means that fewer people are participating in the labour market than before the pandemic.

This situation is caused by the population aged 55 and over. The participation rate of 25 to 54-year-olds is very high at 83.4%. The potential to raise the participation rate and thus meet the high demand for labour is thus rather limited. This can explain the high number of vacancies.

Rising unemployment

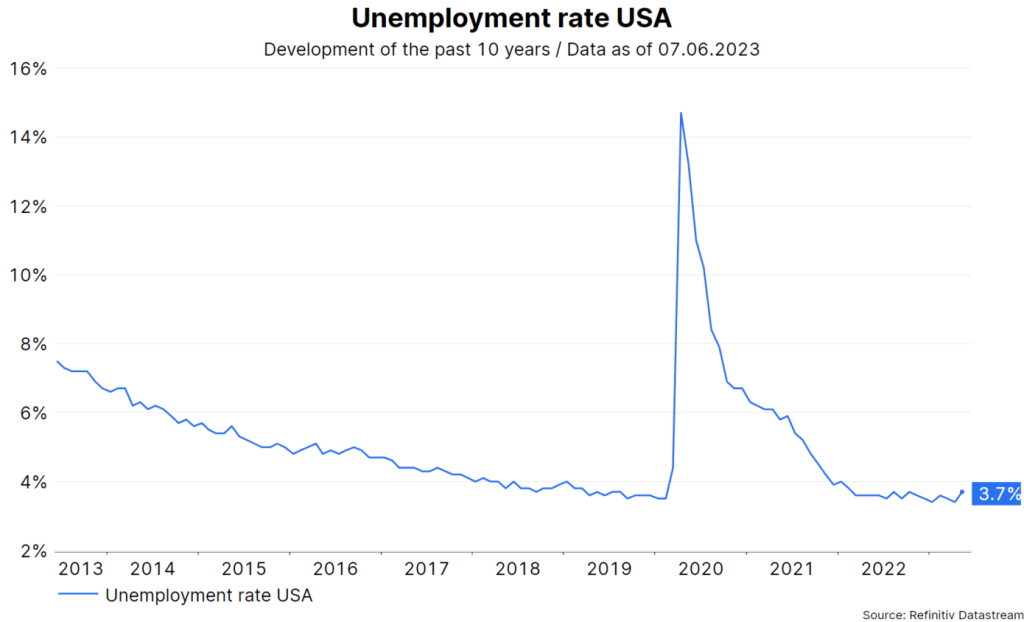

At the same time, the number of jobseekers increased by 440,000. In this context, the most important indicator is probably the unemployment rate. This rate rose to 3.7% in May after 3.4% in the previous month.

Source: Refinitiv Datastream; Note: Past performance is not a reliable indicator for future performance.

Admittedly, this is still a very low value. However, it is worth keeping an eye on the so-called Sahm rule, named after economist Claudia Sahm. The rule signals the beginning of a recession when the three-month average unemployment rate rises by at least 0.5 percentage points compared to the low of the previous twelve months. While we are not yet in this scenario, experience shows that this can change quickly.

In the past, once the unemployment rate started to rise, it would often do so quickly and strongly if this had been preceded by quick and strong key-lending rate hikes.

Soft landing

The optimistic camp, however, points out that a soft landing of the economy is conceivable. In this scenario, inflation pressure falls because the currently very high number of job vacancies also drops markedly. Meanwhile, the unemployment rate rises only moderately towards its natural value.

This natural rate of unemployment is estimated at a value of 4.4%. At this level, all job seekers find employment without any additional inflationary pressure coming from the labour market. Still, in the month of April the number of job vacancies surprisingly increased to just over 10 million, after declines in the previous months.

Core parameter: average working hours

In order to establish a relationship between economic growth and employment growth, another key figure is required: the average number of working hours per week (average weekly hours). Since the second half of 2021, this figure has been on a downward trend. In May, average weekly hours worked continued to fall.

Thus, the various labour market indicators are in line with meagre economic growth, even though the unemployment rate is low and employment growth is strong.

Conclusion

Although the latest US labour market data show strong employment growth, economic growth remains on the subdued front. The labour market remains very tight. However, the rise in the unemployment rate in May could indicate the first signs of a recession. The risk of such an economic event remains at an uncomfortably high level.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Tense situation in the Middle East: Will oil prices rise again?

Oil prices have fallen significantly in the year to date, which also had a noticeable dampening effect on inflation. However, this could change with the further escalation in the Middle East. Following the Iranian missile attack on Israel, Prime Minister Netanyahu announced retaliation.