Why is the inlfation outlook for 2018 important? In our three part series we explain how inflation works.

At the moment the environment on the markets is very supportive. The economy is booming, the big central banks are still buying government bonds on aggregate and are thus keeping yields low, and the tax reform in the USA has improved the sentiment further over the past weeks. In addition, most asset managers agree on the status quo. The cycle has come a long way, and assets are not cheap anymore. That being said, there is hardly any reason not to take some risk if one wants to (and has to) earn money. Given this background, people ask “when will the party end?”. An increase in inflation is (one of) the usual suspect(s).

Why is that the case?

The current cycle has come a long way. After the big recession in 2008/09 in the USA, a recovery set in that has lasted to this day. Soon it will be the second-longest recovery phase in recorded history, which in the USA dates back to about 1850. While periods of recovery do not die from old age, it is clear that in such a situation the question emerges as to how long this can continue. And this is where we get to talk about the causes that usually trigger a recession.

First, we have external events such as wars or sudden price shocks of important commodities like oil. In addition, large-scale imbalances that have become unbearable can result in recession. This was the case in 2008/09.

The situation that we have seen most often since WWII, however, was a scenario where the economy was about to overheat, and the central bank would increase interest rates so as to prevent this from happening. The long-term US Fed President William McChesney Martin Jr. once described the job of the central bank as “to take away the punch bowl just as the party gets going”. According to traditional indicators, we are currently in the phase of the party taking off. If inflation were to rise as well in this situation, the US central bank would probably come under pressure to raise interest rates more significantly than currently expected by the market. Which the financial markets would react to negatively.

Does this only apply to the USA or also to Europe?

In Europe, the situation on the whole differs from that in the USA. First of all, due to the euro crisis in Europe, the region has not seen an uninterrupted recovery phase. The ongoing recovery is still very fresh. Also, the situation in Europe is not homogenous. In some countries such as Germany, the economy is at its peak. In other countries, the recovery is strong, but the economy is far from overheating. This is for example the case in Spain. Some countries such as Italy have seen a very limited degree of recovery. Given this context, the situation in Europe differs significantly from that in the USA.

When we talk about inflation, what exactly does that mean?

Nowadays most large central banks have an explicit inflation target. For example, the ECB wants to keep inflation below, but close to, 2% in the medium term. By the term inflation, central banks refer to a change in the level of prices rather than in individual prices. This change is measured on the basis of a representative basket of goods. It contains goods and services that are weighted so as to be representative of the overall demographic. It is important to understand that this is not about individual prices or parts of the population, but about the change in the general price level.

We often hear that inflation is not properly measured anyway, and that it is actually much higher. What do you think about this criticism?

This is one of my favourite topics. I have been in this business for more than 20 years, and almost always when there is talk of inflation, two issues come up. The rate of inflation is not correct, and/or the core inflation rate is rubbish, because there is nobody who does not need food or petrol.

As far as the first issue is concerned: it makes perfect sense that a representative basket of goods would not fit an individual person, and indeed as a rule it does not do so. I have taught for many years at the university and in adult education. Back then, the accusation of “inflation forgery” was a popular one, too. So, I started to ask the various participants how much they spent on the main categories of the Consumer Price Index (CPI). Interestingly, as soon as the sample had reached a size of about 20 people, the average results were roughly in line with the weightings in the basket of goods that is used for the CPI. But individually, the overlap was rather less impressive. People just differ from each other massively when it comes to consumer behaviour. And the central bank’s job is not to manage the changes in Gerold Permoser’s basket of goods, but those in all our baskets. To sum it up, I do believe that the basket of goods underlying the CPI is correct, as are the inflation data.

I also believe that the criticism levied against core inflation holds little water. It is the central bank’s task to keep inflation in check. Core inflation is inflation without energy and food. Those two components tend to be volatile and also largely defy steering by the central bank. While the oil price does react to economic growth, it is driven much more significantly by other factors. Food prices depend mainly on the weather. Imagine a bad harvest causes food prices to rise. The turmoil created by this causes war in the Middle East, which in turn results in a higher oil price. We had a similar situation during the Arab Spring, which had been preceded by a massive rise in food prices. Should the central bank in such a scenario, where disposable income has fallen due to an increase in oil and food prices, really hike its interest rates? It would have no bearing on the underlying cause and would only make things worse. This makes no sense. Therefore, core inflation is the better inflation indicator for central banks, from my point of view.

The US central bank keeps mentioning the PCE Core Deflator. What is that?

The PCE Core Deflator is the inflation figure that the official inflation target of the US Fed has referred to since 2012. But de facto the Fed has made its preference of the PCE Core Deflator versus the CPI pretty clear since the beginning of the 2000s.

PCE is short for Personal Consumption Expenditure. It is called deflator because this is an index that is used to translate nominal into real consumer spending.

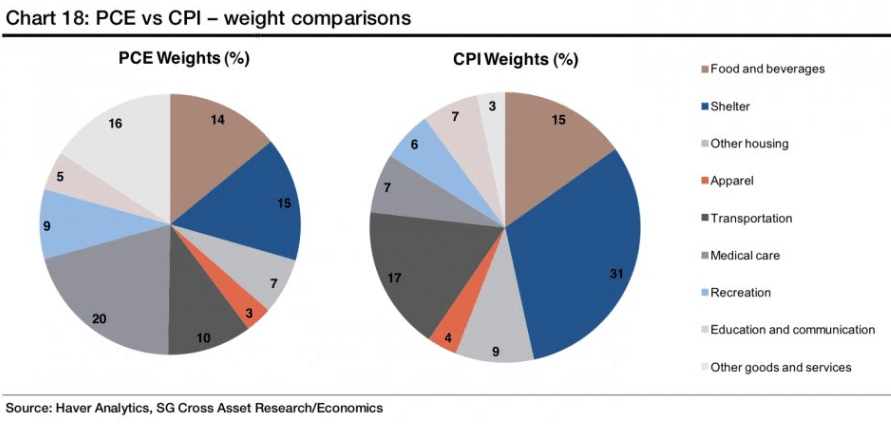

How does it differ from the CPI?

Superficially, the PCE Deflator is based on a broader basket of goods than the CPI. The basket of goods of the PCE Deflator consists. The basket of goods of the CPI makes up 75% of the PCE basket, which then also includes additional items.

Here, three effects play a crucial role.

- We can call the first one scope effect. The CPI covers private household consumer spending. The PCE Deflator, on the other hand, measures what the household sector spends or what third parties spend for the household sector. Healthcare spending makes up the biggest difference here. Only a minor part of said spending comes from households directly. Third parties account for the biggest part of healthcare spending. Either healthcare insurance offered by companies or by Medicare and Medicaid, the two public healthcare programmes. The costs of these indirect expenses are taken into account by the PCE Deflator, which is why here the share of healthcare costs is significantly higher than for the CPI.

- The second big difference is based on the weight effect. Even if one did use the same components, their weights might differ in the basket. Which, for various reasons, they actually do.

- Given the broad composition of the PCE Deflator and the high weight of healthcare spending, the weight of housing expenses, which make up about 40% of the CPI, automatically decreases.

- The data used for establishing the two baskets come from different sources. The basket of goods used for the CPI is based on surveys among consumers, whereas the basket of the PCE Deflator is built from surveys among companies. Diverging terminologies and definitions result in differences.

- The last big effect is the formula effect. Consumers react to price changes by adjusting their consumer behaviour. Imagine the price of leek increases, as it did two years ago. Consumers react by buying more (spring) onions. The CPI does not react to this shift at all, whereas the PCE Deflator takes it into account and adjusts the basket of goods systematically.

Ultimately, the biggest divergence of the two baskets comes from the difference in weights of healthcare and housing.

In addition to this formal explanation, one also has to point out that the PCE Deflator has been about 0.5% lower than the referential value of the CPI over the past 20 years. The fact that the Fed changed the inflation index but not the inflation target of 2% in 2012 means that the inflation target of the Fed with reference to the CPI increased automatically by about 0.5%. This way the US central bank has increased its own target. Considering the fact that inflation has been lower for years than predicted by central banks, perhaps the target is overly ambitious.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.