The aggregate of published indicators points to average global economic growth and falling inflation. Economic growth is being driven by the services sector, while the manufacturing sector is stagnating.

Looking through the lens of country differences, the good growth in the USA stands out in particular, while negative news dominates for China. Overall, the probability of an immediate recession has decreased significantly. But the risks in the medium term remain.

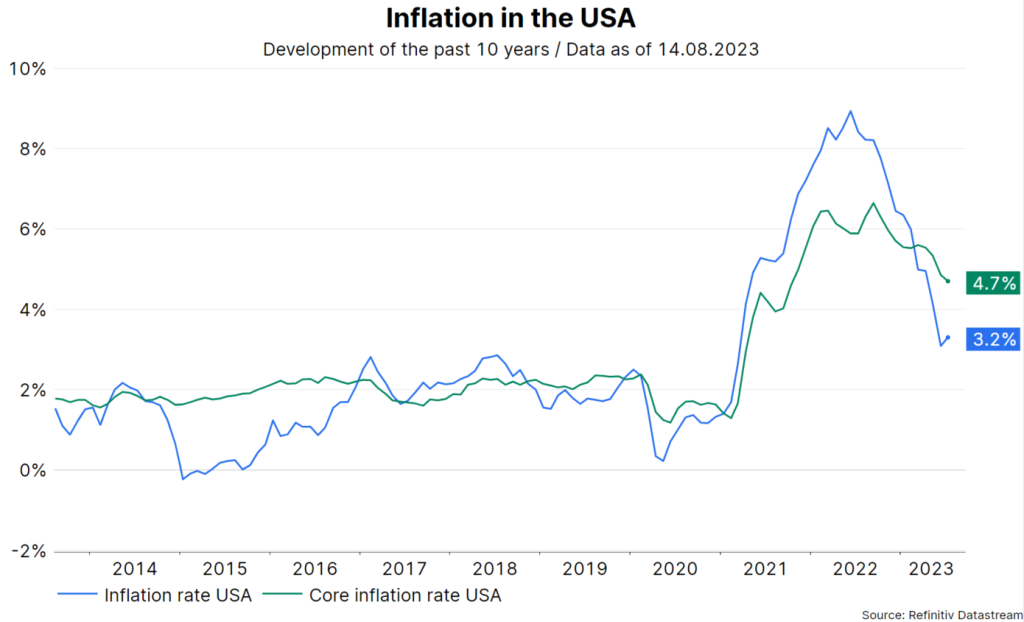

Falling inflation

Last week, the report on consumer price inflation in the USA for the month of July was published. Compared to the same month last year, inflation was slightly higher at 3.2% than in June (3.0%). However, this was due to base effects – the trend is for inflation to continue to fall. Importantly, the numerous indicators for core inflation also pointed to a decline in inflation.

Note: Past performance is not a reliable indicator for future performance of an investment.

Inflation is also falling across the OECD region (June: 5.7% y/y, high: 10.7% in October 2022). Inflation remains above respective central bank targets (2% in advanced economies). But declining inflation rates increase the scope for central banks to pause in the rate hike cycle. Indeed, no further rate hikes are expected at the respective central bank meetings in September for both the USA and the euro zone.

Positive growth surprises in the USA

At the same time, the growth indicators for the U.S.A. are surprising on the positive side. Admittedly, mapping the monthly indicators to quarterly GDP (nowcasting) for the third quarter still yields a wide range, because not many indicators have yet been published for the current quarter (between 4.1% and 1.4%, growth at quarterly intervals, annualized), but we are a long way from a GDP contraction. The probability of an immediate recession in the U.S.A. has thus decreased significantly.

Weak growth indicators in China

Last week showed a further decline in exports and imports for goods, falling prices for consumers and producers, and particularly weak credit growth. In addition, news is mounting about unpaid debts of real estate developers and financial service providers in the shadow banking system. China is currently facing several problems: weak private domestic demand, adjustment in the real estate sector, negative consumer sentiment, high youth unemployment, conflict with the U.S. and weak global demand for goods. The announced government support measures are small and targeted, addressing the downside risks. But they are not broad-based and large. The 5% growth target announced in the spring could still be achieved this year. However, China is not a global growth pillar at present. Rather, deflationary pressures are being exported. This can be seen in the weakening of the Chinese currency and the falling prices for industrial metals.

In the medium term (until the end of 2024), three scenarios are emerging:

- Scenario 1: Soft landing

If inflation continues to fall toward the central bank target, the scope for key rate cuts next year increases. However, economic growth in the advanced economies weakens to below-average levels due to the delayed effect of key rate hikes. Probability: 40%

- Scenario 2: Stagnation

Central banks stop raising policy rates, but monetary policies become more restrictive: A) If inflation falls but nominal interest rates remain unchanged, real interest rates increase. B) Economic research suggests that the real neutral interest rate rose during the pandemic. This would provide an explanation for why the rapid and large rate hikes have not (yet) triggered a recession. If the neutral interest rate falls again, but policy rates remain high due to persistent inflation risks, this would imply a tightening of monetary policy. Probability: 40%

- Scenario 3: Inflation / hard landing

The decline in inflation ends at too high a level or inflation even rises again because global economic growth remains resilient. Central banks raise key interest rates after an extended pause. Probability: 20%

Conclusion

The probability of scenario 1 (soft landing) has increased in recent weeks, driven by the positive growth surprises and the negative (in the technical sense) inflation surprises in the USA. In the meantime, the financial market has (probably) priced in a good part of this good scenario.

This can be seen from the rise in share prices, the low credit spreads and the inflation rates priced into the market (falling to 2.4% in a year in the USA and to 2.9% in France). But the other two, less favorable scenarios, still have an uncomfortably high probability. This can also explain the share price declines since the beginning of the month.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Netflix – the movie script of a success story

Everyone knows Netflix these days. The company has developed from a DVD rental service into a globally renowned streaming service. The company’s history is also an example of the important role the high-yield market can play in corporate bonds for young and innovative companies.