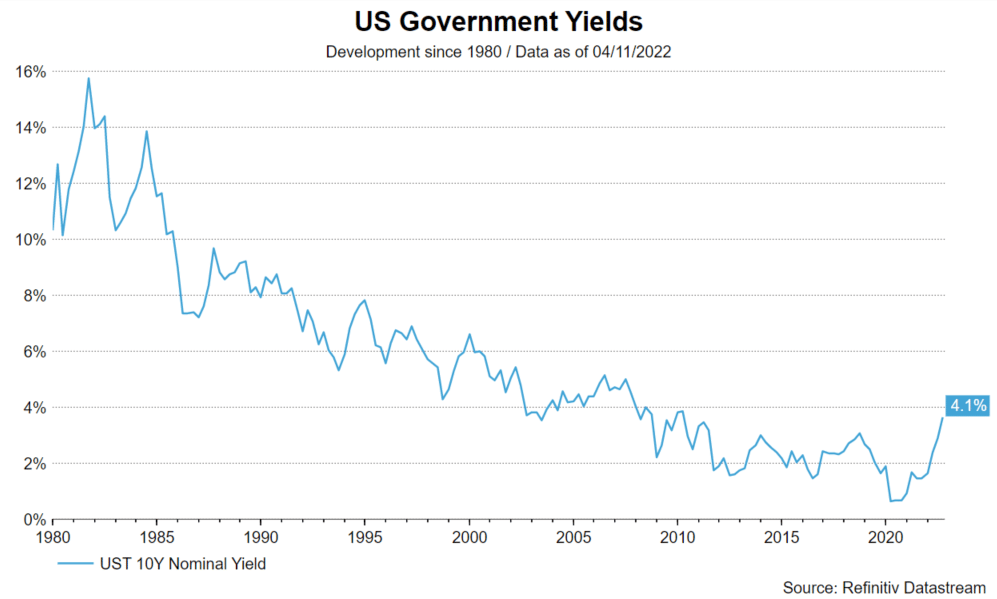

The major central banks have recently come to a turning point in their monetary policy: After years of low key interest rates the hiking cycle has begun. This week, the Federal Reserve in the USA raised its key interest rate for the sixth time this year to a level of 3.75 to 4.00 %. The “Fed funds rate” thus reached its highest level since January 2008.

With the turnaround in interest rates, the bull market the bull-market in bonds, which had started in the early 1980s, seems to have come to an end. This is also reflected in the nominal yields of US government bonds:

Note: Past performance is not a reliable indicator of the future performance of an investment.

In this paper we concentrate on long term effects. The essential question is whether this turning point is cyclical or structural. Only if this effect is driven by structural changes, will it be sustainable. And since structural macro-economic changes are captured by neutral interest rates, which does not include inflation or business cycle effects, we will concentrate our analysis on this rate. Our primary focus is on US bond yields since the US market accounts for more than half of the world’s bond market.

From nominal to neutral – an overview of different rate concepts and theories

Usually, interest rates are quoted in nominal terms in almost any conversation. However, investors are not interested in the amount of money they will receive but how much their investment will be worth in terms of goods and services that they can buy with it. Therefore, we need to consider the real interest rate, which is the compact version of the nominal interest rate, net of expected inflation.

Consequently, central banks use real rates in order to steer their most important tool, i.e. monetary policy. If the central bank considers inflation too high /low it will increase /decrease real interest rates.

The essential question is what level of real interest rates would keep the economy in balance? The “neutral interest rate” works as the proverbial lighthouse here: it basically expands the concept of real interest rates by searching the target real rate such that no additional monetary action (stimulus / reduction of economic activity) is necessary.

In the long term, therefore, the real interest rate has to move towards the neutral interest rate as it is economically impossible to decouple from it indefinitely.

So, what are the factors that determine the neutral (real) interest rate in the long term? Most theories see this rate as the equilibrium between two major factors: savings (supply of capital) and investments (demand of capital). Decreases in the propensity to save tend to increase real interest rates and shift the supply curve inwards, while increases in the propensity to invest tend to increase real interest rates and shift the demand curve outwards.

Significant fundamental factors for the development of the neutral interest rate

The mid- to long-term behaviour of the neutral interest rate depends on a variety of factors. However, we identified three main themes which we regard as structural changes with a direct and significant impact on the future neutral interest rate.

These three factors are:

- Return of the “Big State”

- Change in demographics

- Reversal of the “Global Savings Glut”

1. The Return of the “Big State”

The major factor regarding the investment side is the changing general perception of the role of the government. A “strong state” with bigger interference for mastering business cycles, but also targeting universal issues such as climate change, universal security, and “re-globalisation” has moved into focus. In addition (especially driven by the pandemic), the public acceptance for higher fiscal deficits and governmental debt has increased significantly on a global scale.

Also, the “big state” uses subsidies and stimulus packages to implement its political agenda. It also acts on a regulatory and legal level, which leads to a higher degree of intervention compared to the 2000s, when de-regulation was the political style de jour. Nowadays, taxing excess profits of energy companies and additional financial regulation is rather common among Western countries.

This intervention even affects global supply chains as governments define which countries are better suited to trade with from an ethical and/or political perspective. “Friend-shoring” will in our opinion be a decisive factor for companies in terms of suitable vendors and suppliers.

As a result, we expect governments to continue with high spending programmes in major areas such as climate investments, security of food and energy supply as well as military defence.

These areas are rather undisputed among economists and have a direct impact on the investment side of the interest rate equilibrium. Increasing investments move the demand curve outwards and lead to a rise in the neutral interest rate.

2. Demographics

The second structural factor which is important for the trend of the neutral interest rate is the change in demographics. Demographics have already been a major factor driving the interest rates down in the past. However, we believe that this dynamic is about to fundamentally change.

Increase in general life expectancy

For the past decades, most economies worldwide have been experiencing a sharp rise in life expectancy. Rising life expectancy results in higher savings propensity, as individuals expect a longer retirement period. Higher savings move the demand curve inwards thereby putting downward pressure on real interest rates. However, this increase has slowed down significantly in past years. We expect this trend to continue basically due to the fact that past advances in medical treatment are not likely to be repeated in the future. That should significantly reduce the downward pressure on neutral real interest rates.

Increase in the old-age dependency ratio

The old-age dependency ratio is defined as ratio of the share of population above 64 years to the share between of 16 to 64 years. This ratio has been slowly increasing in the US in the past years. However, the increase has started to accelerate recently and is expected to continue. An increasing dependency ratio leads to a reduction in the overall savings rate as individuals build their savings during their working years and consume it in retirement.

Decrease in economic growth

The flip side of an increasing dependency ratio is that the working-age population is forecasted to decline in many OECD countries. A slowdown in the growth of the working-age population will result in a slowdown in economic growth and would put downward pressure on the neutral interest rate.

This effect could be mitigated by pushing back the retirement age or increasing the participation rate of women as well as by an increase in productivity. Another way to dampen the effect of the decrease on the working population is immigration.

As a result, the slowdown in the extension of life expectancy and the acceleration of the dependency ratio result in lower saving rates, thereby increasing neutral interest rates. However, an expected slowdown in the growth rate of the working force has the opposite effect. Combining all effects, we tend to regard the first effect as the dominant one for the next ten years. Therefore, we expect a slightly positive effect on the neutral interest rate.

3. The reversal of the Global Savings Glut

The last of the three structural changes deals with international excess savings and the impact on US Treasury yields. This effect started about 20 years ago and was a major factor for the long bull-market in US bonds. Again, the effect is divided into two connected yet independent sub-factors.

As described above, the interest rate should be at the equilibrium of savings and investments of an economy. However, there are periods when this function seems out of order.

Former FED-Chairman Ben Bernanke created the “Global Savings Glut”-hypothesis which makes an important extension to the classic theory of the determination of interest rates: savings and investments – and therefore the interest rate – are not only affected by domestic developments, but by global trends.

He explained that an additional wave of savings created a misbalance between supply and demand and led to lower interest rates. These savings were basically exported by prospering Asian economies (developed as well as emerging markets) with the rise of China as the tipping point. Investors were looking for safe havens for their savings abroad. US Treasuries offered safety and liquidity at the same time – the yield was only of minor interest. Consequently, if a higher supply of yield-insensitive savings meets unchanged demand, the interest rate will decrease.

As a result, the “Global Savings Glut” theory merges the megatrend of increasing (excess) savings abroad due to a higher standard of living with the long bull-market in US bonds and highlights the importance of global developments for US Treasury rates.

The “Global Savings Glut” has peaked in 2014 and been constantly reduced since then. The main reason was a fully saturated demand for USD assets by those investors. They were able to turn to other assets and currencies because their level of USD reserves was sufficient. This view proved correct as no country faced a currency crisis during the pandemic.

As a consequence, the reversal of the Global Savings Glut results in reduced excess savings in the USA (independent of the asset class) and should lead to a rise in the US neutral interest rate.

Transition to capital-light economies

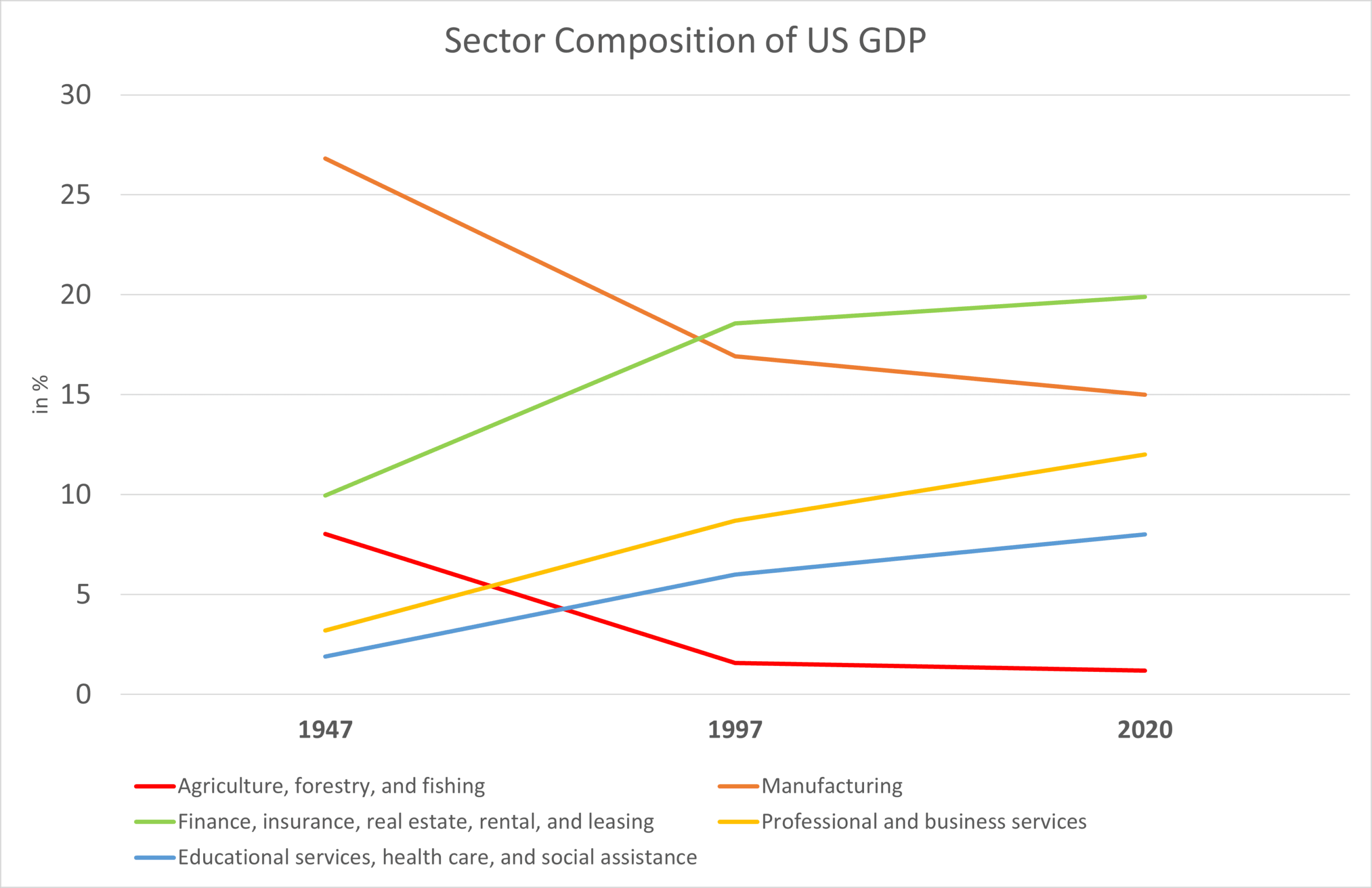

The Global Savings Glut resulted in a structural change of the capital supply side. But the demand side saw a change as well as economies evolve and change their focus over time. In developed economies, a steady transition from agriculture and manufacturing to other sectors has been observed since the end of WWII.

This graph shows the former importance of manufacturing and agriculture in the US, beginning in 1947 (26.8% and 8.0% of GDP). Over the next 73 years, other sectors gained more traction and reducing the importance of manufacturing and agriculture (15.0% / 1.2% of GDP 2020).

As a result of this transition, the new important sectors are not as capital-intensive in terms of required equipment. Consequently, the capital needed for the whole economy decreases just due to a change in the sector composition of the GDP. These economies are becoming “capital-light economies”.

Note that this structural transition has overlapped with the Global Savings Glut in the past 20 years. Both effects are fading in the USA (and other developed markets) at the same time. This is an important issue because even if this structural change in sector composition is expanded to middle-income countries and emerging markets (especially China), the decrease in global investment demand would be softened due to the fact that this transition has already taken place in the (economically more relevant) developed economies.

As a result, the reversal of the “Great Savings Glut” and the trend towards differently composed economies should lead to a higher neutral interest rate. Interestingly, the supply as well as the demand side are affected.

Conclusio: Case for an increase of the neutral interest rate has strengthened

Based on three major structural changes in politics (Return of the Big State), society (Demographics), and economy (Reversal of Global Savings Glut), the case for an increase of the neutral interest rate over the next ten years has strengthened. Both sides of the equilibrium – savings and investments – are affected and participate in this rising environment. Due to the nature of these structural changes, the structural transitions are regarded as fundamental issues with an impact for a long period of time. It seems that the decade-long bull-market in bonds has finally come to an end and the neutral interest rate could rise again.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.