The times of low interest rates are drawing to an end. By raising the Fed funds rate for the first time in five years, the US Fed has marked the turn of an era. Is the time of cheap money over? We talked to the Head of Bond Funds with Erste Asset Management, Wolfgang Zemanek, about inflation, rising yields on the bond markets, and the effects on the global economy.

The US Fed has increased the Fed funds rate. Further hikes are in the pipeline. What does that mean for the bond markets?

The very loose monetary policy we have recently seen from many central banks (including the USA) due to the COVID-19 crisis helped to reduce the downside risks for economies caused by the pandemic. Given that the economy has recovered noticeably, many of these emergency programmes are not necessary any longer. Global inflation has increased drastically in the past months, putting the focus of central banks on the fight against inflation and on curbing inflation expectations. This is also the case in the USA, where the Fed has to regain its credibility as far as fighting inflation is concerned. To a certain degree, it is under stronger political pressure in this context than others.

Were investors caught off guard? How far could the key-lending rates be rising this year in the USA?

The US central bank is at the outset of a cycle of interest rate hikes that might exceed many market participants’ expectations especially during the first few months (from May onwards). From mid-December 2021, the US Fed has been telegraphing the imminent interest rate reversal to the market participants. The change in expectations by investors led to the re-assessment of the situation and to a significant increase in yields and the resulting losses across all maturities of the US yield curve. The market has an increase of 2% for the key-lending rates priced in for the end of the year. In the meantime, however, the larger part of these future rate hikes seems to have been anticipated by the market.

Will we see interest rate increases in the Eurozone as well? Is the ECB lagging behind?

The war in Ukraine is a humanitarian catastrophe that may also come with negative effects on the economic development of Europe. Due to its proximity to the hotspot, Europe is more badly affected than the rest of the world. The energy dependence from Russia alone holds increased macro-economic risk for many European countries. These considerations enter the assessment of the future interest rate policy of the ECB. The central bank wants to avoid mistakes in its policy in the future. In Europe, too, inflation has been on the rise recently. The ECB will therefore be tapering quantitative programmes such as APP (Asset Purchase Programme) in the coming months. Interest rate hikes, the likes of which we have seen across numerous countries already, are also heading our way in the Eurozone. We currently expect up to two interest rate hikes of 0.25% each until the end of the year from the ECB. If neither the war in Ukraine nor possible corona mutations cause strong recessive effects to materialise in the Eurozone economies, the period of negative key-lending rates in the Eurozone may be over in Q1 2023. This should subsequently make bonds more attractive again, even though the current losses are very painful for investors.

“Interest rate hikes are heading our way in the Eurozone.”

Wolfgang Zemanek, Head of Bond Funds, Erste Asset Management

© Bild: Huger

Interest rate increases and rising yields have a negative impact on the price of a bond. Why is that the case?

The holders of, say, a fixed-coupon bond with an annual coupon of 2% would probably sell this bond as soon as a comparable one with a higher coupon of, for example, 3% were issued (N.B. strongly simplified example assuming identical issuer and same remaining time to maturity). As a result, the price of the 2% bond would fall. The longer the remaining time to maturity of a fixed-coupon bond, the higher (as a rule) the sensitivity to interest rate changes in the market, i.e. the duration.

What can investors do to protect themselves against yield increases?

There are of course ways to deal with interest rate increases, e.g. by investing in bonds with low interest rate sensitivity or in high-yield bonds, which offer higher yields in order to compensate for the higher default risk associated with the issuer (i.e. debtor). The higher yield creates a certain degree of buffer against more significant losses. But it is not possible to avoid the effects of yield increases altogether. For high-yield bonds, the correlation to the equity markets is higher, which means more risk from that angle.

Is the time of cheap money over?

As pointed out earlier, we are not expecting a recession for now. Inflation should not remain as high as it currently is, but it should remain elevated all the same in comparison with recent years. We may also see higher interest rates and less additional liquidity from the central banks in due course.

The yields of US and euro government bonds have successively fallen over the past ten years. Is it time yet to call the current situation a trend reversal?

At the moment, it looks like a change of regime. In recent years, many central banks were fighting disinflation or deflationary tendencies. The situation has inverted against the backdrop of the events unfolding over the past two years. Rising inflation is back on the agenda. That being said, we do not expect the inflation rate to continue rising at this speed. The measures taken by the central banks should also dampen inflation expectations. If this scenario materialises, yields will not be rising forever, either.

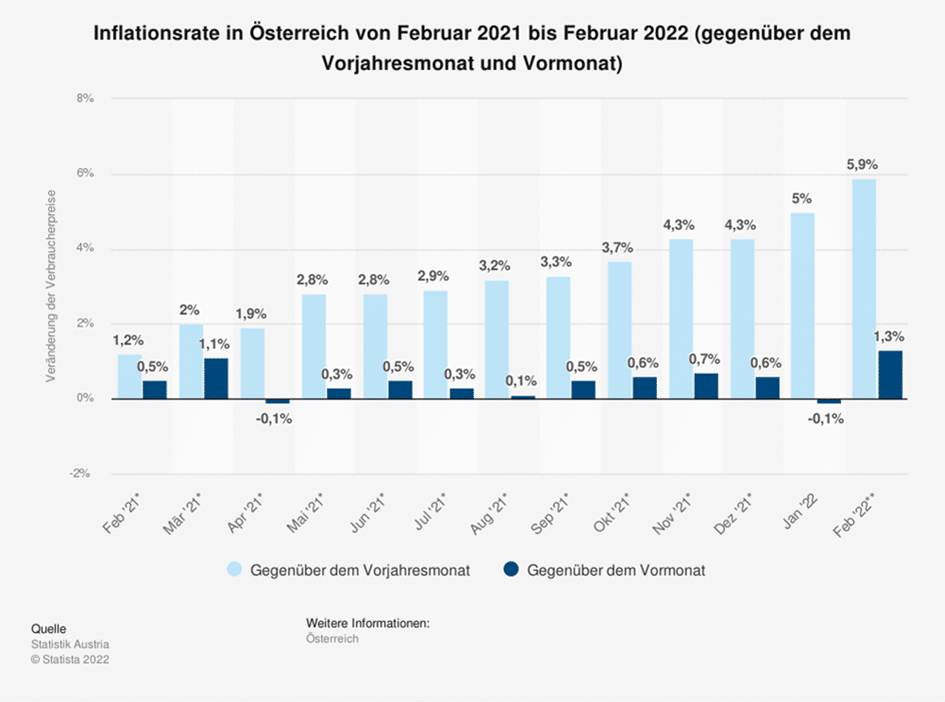

Inflation rates have increased massively. Will the trend continue at this speed?

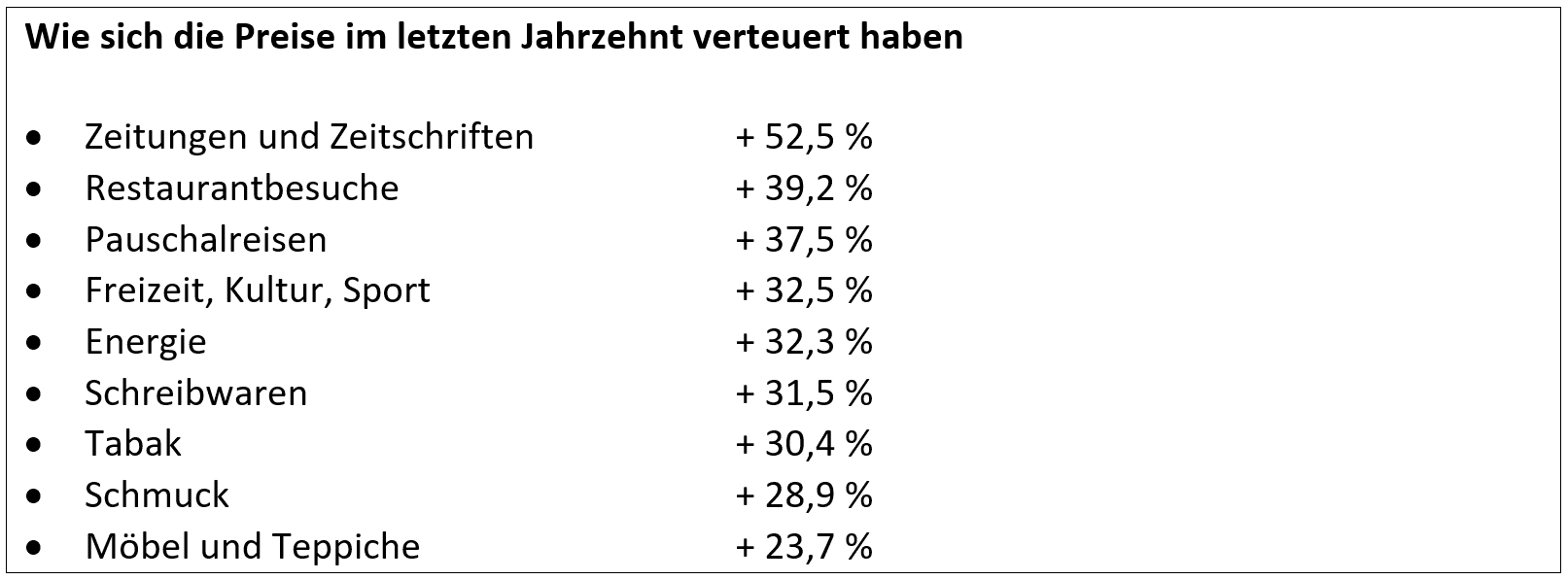

The increase in inflation rates was caused by enormous demand, supply chain problems, distortions due to the pandemic, and the drastic increase in commodity prices in the wake of the war in Ukraine. By the way, the increase in food prices has hit poor countries hardest. While central banks cannot directly thwart inflation that has been caused by higher energy prices, they can hamper so-called second-round effects (i.e. spill-over effects) via a restrictive monetary policy. This situation is imminent.

Who benefits from the high inflation rates?

Mainly debtors – and thus countries – as the value of claims decreases in real terms

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.