As the year 2020 comes to a close, the European Central Bank (ECB) and the European Parliament have put their respective programmes for the fight against the crisis on track for next year. The MEPs recently approved the approximately EUR 1.1tn Community budget for the next seven years, which includes EUR 750bn in Corona aid. To support the economy in the crisis, the ECB decided last week, among other things, to increase its PEPP pandemic bond purchase programme by EUR 500bn to EUR 1.85tn and to extend the purchases by nine months until the end of March 2022.

The ECB launched its emergency programme shortly after the pandemic’s escalation in March, with a volume of EUR 750bn, to buy government and corporate bonds. According to the ECB, the PEPP (Pandemic Emergency Purchase Programme) bond-buying programme is intended to help all sectors of the economy benefit from better financing conditions and thus mitigate the Corona shock.

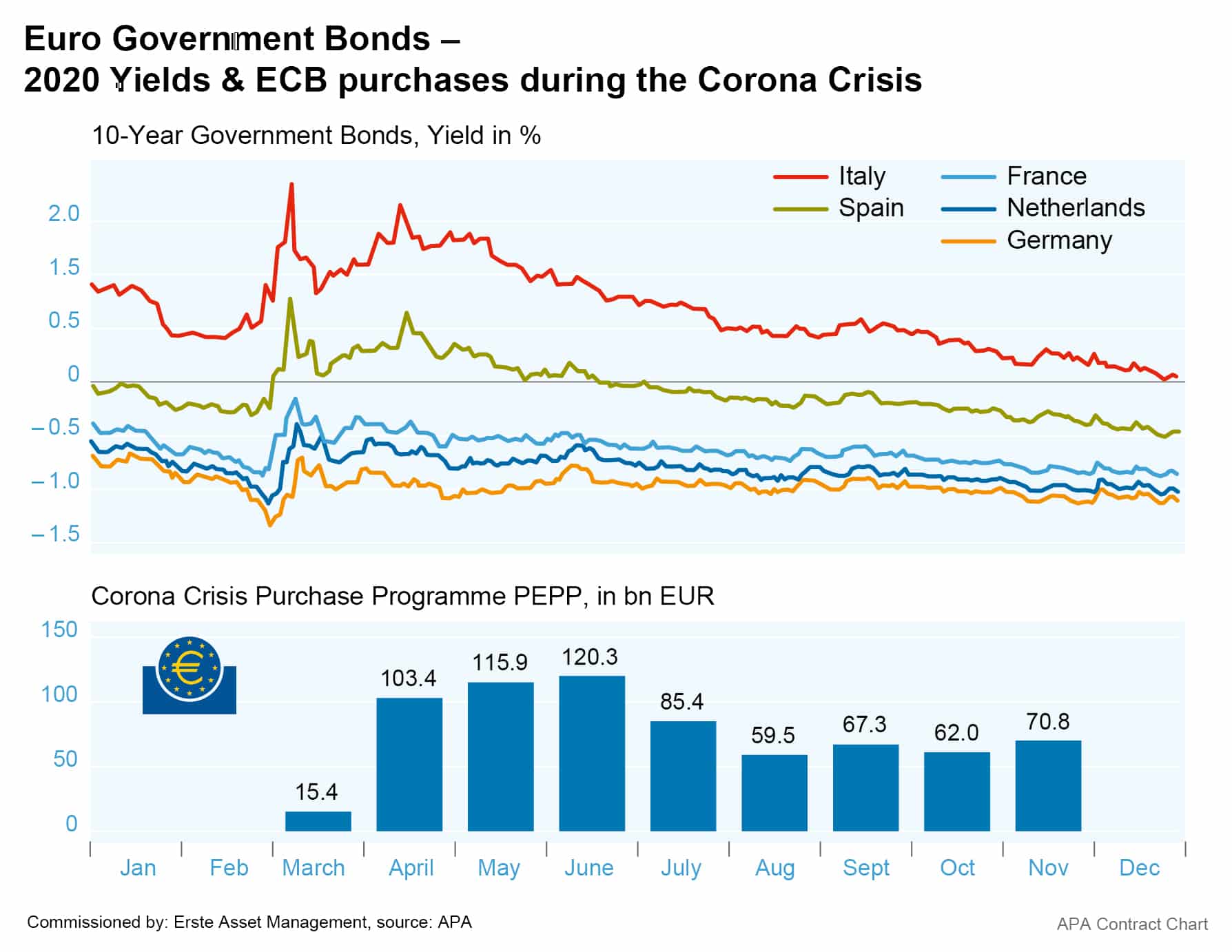

Bond-buying programme to help finance crisis programmes

In concrete terms, the bond purchases will lower interest rates on the bond market, allowing cheaper refinancing for states and companies during the crisis. For example, states can finance their multi-billion euro rescue programmes more easily if the ECB itself acts as a buyer of their government bonds.

While previous ECB bond-buying programmes were tied to a capital key based on the individual euro countries’ population size and economic strength, the central bank is allowed to deviate from this key in its Corona emergency programme. It is thus more flexible and can buy more bonds from the states particularly affected by the crisis.

As a matter of fact, when the crisis broke out, the prices of European government bonds fell and their yields shot up briefly. However, as the PEPP bond purchases started, bond prices rose again and yields returned to previous levels. After an initial increase in June, the ECB has now once again massively expanded its pandemic bond-buying programme.

With the bond purchases, the ECB is also fighting the current negative inflation and trying to raise the inflation rate back to an economically desirable level. Most recently, the inflation rate in the eurozone was –0.3 per cent, far from the ECB’s target of around 2 per cent.

Legal note: Prognoses are no reliable indicator for future performance.

Extension of liquidity injections for banks

In addition, private banks are to enjoy more favourable conditions for a longer period in the large ECB liquidity injections called “TLTRO III”. With these cash injections, the institutions can even get a premium when they borrow the money. In addition, three more of these credit operations are to be launched between June and December 2021.

At the same time, the ECB Governing Council decided on a new series of emergency loans for banks, so-called “Pandemic Emergency Longer-Term Refinancing Operations” (PELTRO), which are to be granted in four tranches next year. In addition, purchases under the older APP bond programme are to continue at a monthly rate of EUR 20bn.

As expected, the central bank left its key interest rate at the record low of 0.0 per cent, where it has been since March 2016. The deposit rate also remains at minus 0.5 per cent. This means that banks currently have to pay penalty interest when they park surplus funds at the central bank.

The decision on the EU budget was awaited particularly eagerly this year. Hungary and Poland originally wanted to use a veto to prevent the disbursement of EU money being conditional on compliance with rule of law principles going forward. To that end, they initially blocked the EUR 1.1tn EU budget package. Without a solution, the EU would have had to enter 2021 with an emergency budget and would not have been able to launch the Corona aid package.

A compromise clears the path for EU budget after Hungarian and Polish veto

However, the heads of state and government finally agreed on a compromise at their summit meeting. The compromise provides that the new procedure for punishing violations of the rule of law will be supplemented by an additional declaration. Among other things, it specifies which options Hungary and Poland have to defend themselves against the regulation’s application. One of these is a review of the regulation for the procedure by the European Court of Justice.

Thus, the EUR 750bn Corona stimulus package envisaged in the budget is on track and should now support a post-crisis upswing. In the view of the EU Commission, the rapid deployment of Corona vaccines could accelerate the economic recovery in the process. “We could see a return to pre-crisis GDP levels sooner than expected,” the EU EVP for Economy, Paolo Gentiloni, said recently. The first positive signs are expected in Q1 of 2021. Before that, however, a difficult winter lies ahead, Gentiloni said.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Trump on fire!

Donald Trump is getting serious and imposing temporary tariffs on his major trading partners. He is also escalating the war in Ukraine and increasing the pressure on Europe, which will hopefully soon be galvanized into unity with a new German Bundestag.

Rising inflation expectations and yields: a risk for market sentiment?

Two developments on the stock markets have stood out since the beginning of the year: rising inflation expectations and significant increases in government bond yields. Could market sentiment soon turn frosty in view of this?