Many investors are opting for long-term capital accumulation by taking out a fund savings plan. This usually involves building capital by making monthly payments towards a selected investment fund over a longer period of time.

Falling share prices on the equity markets most often also result in losses to the capital paid into funds. Investors then often question their actions, fail to pursue the original strategy of long-term capital accumulation, and terminate the fund savings plan. In retrospect, this often turns out to be a mistake, as the financial markets have repeatedly recovered from crises in the past and the investment goal could have been achieved with the appropriate perseverance.

In the following we would like to give you a few tips that can help to get through difficult times – or in simple terms, “just hang in there”.

Here are our tips at a glance:

- Think long-term

- Invest only capital that is not needed in the short term

- Expect and plan for periods of falling prices

- Do not get influenced by market events

- Do not look at the portfolio all the time

1. Strategy: think long-term instead of short-term (no constant “in and out” strategy)

If you decide on a fund savings plan with a monthly deposit of, for example, EUR 100, you should be aware right from the start that it is not possible to get rich quickly with this strategy.

Rather, the aim is to save a fixed amount each month over many years. If the price of the selected fund falls but the monthly savings amount remains the same, more fund share units are bought automatically.

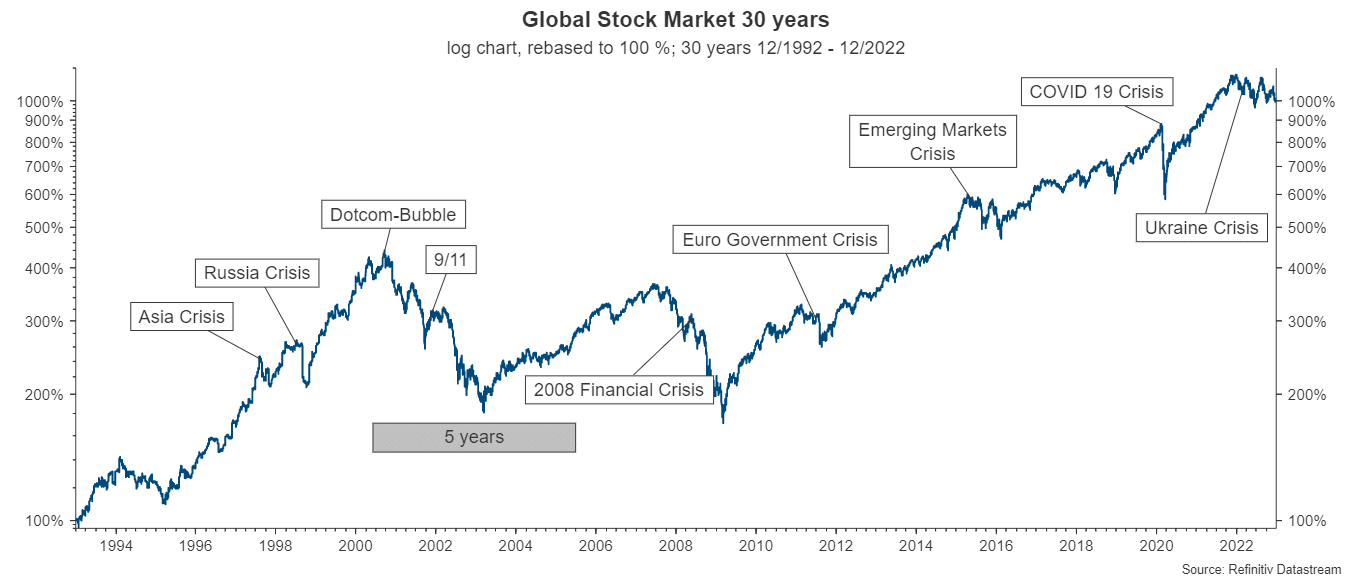

But how long does a long-term investment strategy take if the investment is built up in monthly tranches? Let’s take a look at the development of the global equity market over the past 30 years and find out whether a period of five years, which is popular investment horizon among retail investors, is sufficient to invest sensibly in the equity market.

Source: Refinitiv Datastream, period: 31 December 1992 – 30 December 2022

Please note: representation of an index, no direct investment possible. Past performance is not indicative of future development.

The long-term chart illustrates how the equity market has performed over the past 30 years. There have always been prolonged share price increases, as well as crises that have to significant losses on the financial markets.

In the chart we have placed a grey box for comparison purposes, which simply shows a five-year horizon within the longer period of 30 years. With such a short interval, it is very difficult to find the right time for personal investment.

Investors who want to invest in a high-risk investment and only have five years available should first ask themselves this:

- “As a ‘non-professional’, will I manage to catch a period in such a turbulent market where I can expect to achieve at least a positiv return?“

With a rather short investment period, it will be very difficult to answer this question in the positive. Perhaps the better – and rational – question would be:

- “What should my investment horizon be for me to be able to ride out the odd slump on the market?”

It might be advisable to take another look at the above chart. The following rule of thumb could be used:

- Recommended minimum holding period x 2 (since with fund savings the capital is built up slowly and the last deposit is only made at the end).

2. Invest only capital that is not needed in the short term

Let’s assume that an investor has chosen a fund savings plan with a monthly deposit of EUR 100. How much capital is that over time?

- After five years: EUR 6,000 (12 x 100 x 5 years)

- After ten years: EUR 12,000 (12 x 100 x 10 years)

Irrespective of this investment strategy, there should always be sufficient reserves in a savings book or savings account. Then you are also prepared for unplanned events, such as the repair of the car or the purchase of a new refrigerator and do not have to fall back on the invested capital.

The conclusion is therefore:

- You should allocate only that part of your capital to risky investments which you can spare for a (good) while. And you should also be prepared to lose a smaller or larger part of it without endangering your standard of living.

3. Expect and plan for periods of falling prices

Falling prices on the financial markets are the rule, not the exception. The time at which these occur is unpredictable. Particularly if you have opted for a monthly savings plan in an equity fund, for example, phases of falling prices can also offer an advantage. Because for the capital paid in, you will receive a higher number of fund shares during the period of low prices.

An important aspect for your own investment planning:

- Risky investments are subject to strong fluctuations both ways, i.e. up and down. However, solid investments have always recovered in the past.

If you have an investment horizon of 10, 15 or 20 years, a sudden short-term price decline is not really relevant.

4. Do not get influenced by market events

Every investment should serve a specific purpose and thus be carried out with a plan – an investment strategy. In addition to the selection of the appropriate investment instrument (e.g. a global equity fund) and an investment period that makes sense, the size of the position within your own portfolio also plays an important role.

- Or simply put: “The investment must suit me!”

Then even temporary market events should have little or no impact on the personal investment strategy.

5. Do not look at the portfolio all the time

It is important to make conscious investment decisions. And you should also know that you cannot influence or control all aspects of investment.

- You cannot influence price movements on the financial markets. It is therefore pointless to look at the price trend of your investment every day

If you are pursuing a long-term strategy, you should also give your investment sufficient time and leeway in terms of price fluctuations.

Conclusion

In addition to opportunities, every investment in the financial market comes with opportunities AND corresponding risks. These go beyond purely financial aspects. Price fluctuations strongly affect how we feel about our investment.

Particularly sharp price declines often lead to hasty decisions. Perseverance and “sticking it out” is then very often the most difficult aspect of personal investing. It is important to choose an investment strategy with which one feels comfortable in good and bad investment times.

Anyone who has opted for long-term fund savings by means of monthly payments has already defined an appropriate investment strategy for themselves.

Note: Please note that an investment in securities also entails risks in addition to the opportunities described.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.