Our experience in recent years has been that of very low interest rates. There was no return to be made from the savings book, and bonds with a longer maturity were not very attractive from a yield perspective. For many years there was hardly any reasonable opportunity to invest in the bond market, so it comes as no surprise that this investment vehicle has almost been forgotten.

However, the tide has turned in recent months. After significantly higher inflation figures, the central banks have raised key interest rates several times, and at the same time bond yields have risen sharply.

This creates new opportunities for bond investors to add according interest rate products to their portfolios.

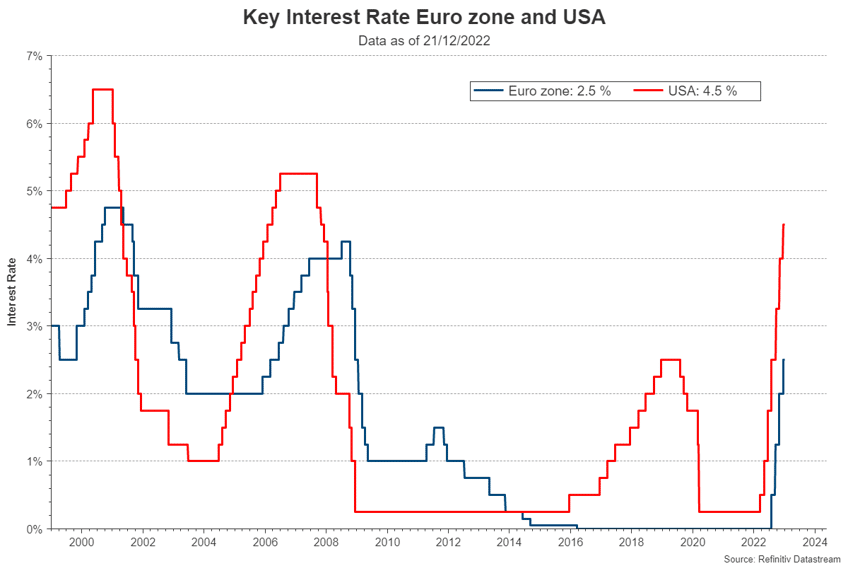

The leading central banks have increased key interest rates both repeatedly and significantly

Let’s first take a look at the central banks of the USA and the Eurozone. The tasks of central banks include stability and maintaining the purchasing power of the currency. In view of the rapidly rising inflation in almost all currency areas, quick and aggressive countermeasures by the central banks were of the utmost importance. One of the options in such a scenario is to raise key-lending rates, which indirectly leads to higher bond yields. This also makes loans more expensive, which should in turn lead to a cooling of consumption and the economy, and – as is the hope of central banks – also a decrease in inflation in the medium term. Key interest rates have risen significantly in recent months, with the US Federal Reserve leading the way and the European Central Bank following suit with some delay.

The longer-term view shows how aggressively the US Fed in particular has acted in recent months:

Source: Refinitiv Datastream, long-term horizon, data as of 21 December 2022

Please note: Past performance is no reliable indicator for future developments.

This long-term representation clearly illustrates two aspects:

- The previous cycle of interest rate hikes occurred in 2006/07 (and was followed by the Great Financial Crisis)

- From the financial crisis onwards, key-lending rates fell to almost zero percent, with the US Federal Reserve raising rates in the meantime but later lowering them again

- The current key-lending rate increases in the USA occurred almost to the 2007 level, while the ECB started much later

Both the US Federal Reserve and the European Central Bank have indicated that further interest rate hikes are to be expected for the coming months.

Effects on the bond markets – the yield is back!

As you can see in the chart, the key-lending rates in the USA (i.e. the Fed Funds rate) are already at 4.5%. This alone should have driven up the attractiveness of bonds. The following questions arise for investors:

- What bonds or what bond segment can cover the currently very high inflation?

- How can I invest in this asset class simply and in a way that makes sense?

Not all bonds are equal – investors should know where to invest!

A bond is a promise by a debtor (issuer of the bond) to repay the capital raised in full at the end of the term and to service the promised interest on time. Issuers of bonds are

- states (government bonds)

- or companies (corporate bonds)

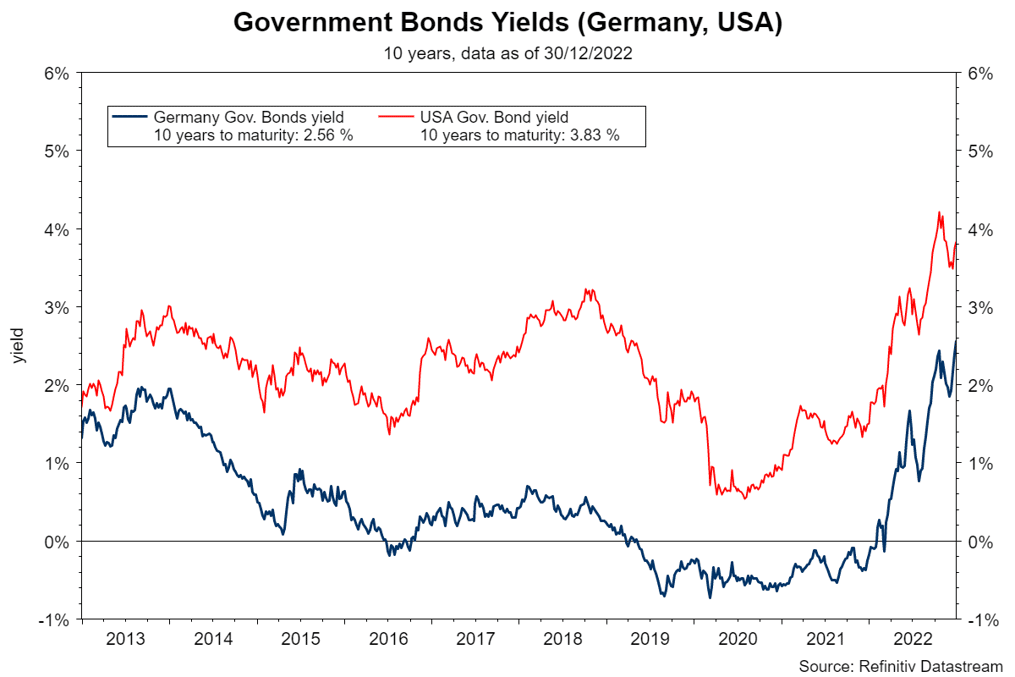

Option 1: government bonds

First, let us look at the yield of government bonds with high ratings, i.e. those from the USA and Germany.

Source: Refinitiv Datastream, long-term horizon, data as of 27 December 2022

Please note: Past performance is no reliable indicator for future developments.

Shown in blue is the yield of the 10Y German government bond (i.e. 10Y to maturity). The yield was negative for several years but has soared significantly in recent months to currently 2.5%.

In comparison (red line), the yield of the 10Y US government bond, i.e. the US Treasury bond, is currently just under 4%. An increase in yields is good for investors who want to reinvest, but it also means losses for investors who have invested at lower yields.

With inflation above 10% in Austria (as of November 2022), the question that arises for government bonds is how a yield of 2% or 4% is supposed to offset an inflation rate of about 10%.

This question is more than justified. If inflation does not subside significantly in the coming years, government bonds are probably not the right investment to preserve the real purchasing power of an investor’s capital.

Option 2: corporate bonds

When companies issue a bond, they usually have to offer a higher yield than comparable government bonds. This yield premium is also referred to as spread and depends on the quality – i.e. the rating – of the respective company.

The rating is assessed and awarded by independent rating agencies. It is usually expressed in letters, where AAA (the so-called triple A) represents the best possible credit rating level. The lower the credit rating, the higher the probability of an issuer’s default – and the higher the interest rates the company has to pay for its bonds. For investors, this means that they have to carefully weigh the potential return and the risk of default for every investment.

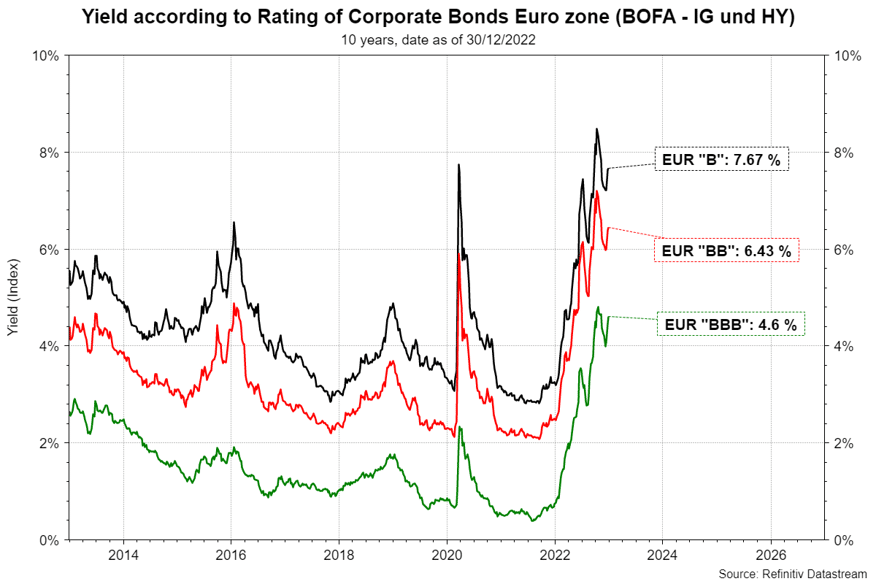

The development of yields for different credit ratings clearly shows how high this compensation for the risk taken currently is:

Corporate bond yields by rating, Eurozone (BOFA – investment grade and high-yield) / 10Y, data as of 27 December 2022

Source: Refinitiv Datastream, long-term horizon, data as of 27 December 2022

Please note: Past performance is no reliable indicator for future developments.

The chart shows the market segments BBB, BB, and B of corporate bonds from the Eurozone. The yields are currently in the range of about 4.5% to 7.5% and thus clearly above those of German government bonds.

The high-yield range (BB or B) is traded at a yield above that offered in the past ten years. At such high levels, a rate of return seems possible that can also cover inflation in the medium term.

Some bond segments have turned attractive again

The significant rise in yields is evident across all bond segments. For investors who are already invested, this has manifested itself in painful losses. However, for newcomers and of course also for existing investors, there are opportunities to buy or expand positions that have not existed in the past ten years.

As we have seen, however, not all bond segments are equally interesting. For those looking to earn a return that can at least cover inflation, corporate bonds can be quite interesting. But investing here is not so easy, because:

- Where do you find the right corporate bonds, and

- How can you spread your risk sufficiently?

A fixed-income fund could be the solution

There is always a certain degree of default risk associated with corporate bonds. Moreover, it is not easy for retail investors to find and buy such bonds. Corporate bonds often come with a high denomination, which makes it very difficult for retail investors to diversify across individual securities. And it is not advisable to put all your capital on just one issuer. Rather, it should be spread across many issuers from different sectors. The principle of risk diversification is particularly important when investing in corporate bonds.

A fixed-income (or bond) fund does just that for investors. The paid-in capital is used to purchase many bonds from companies from different countries, industries and/or rating segments. The greater the risk, the broader the diversification should be. In corporate bond funds, you will therefore often find considerably more than 100 different bonds.

Investors do not have to search for suitable bonds themselves and can invest in such a fund with small amounts as a one-off payment or in tranches, or even save monthly.

Conclusion

After yields have risen noticeably in recent months, investing in the bond market has become much more interesting again. However, if you want to cover inflation with your investment, you should take a closer look and also have to take certain risks.

This may be a good time to ask your bank about investment opportunities, e.g. in corporate bond funds.

Legal note:

Prognoses are no reliable indicator for future performance.

Please note that an investment in assets also entails risks in addition to the opportunities described.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.