In recent days, equities and other risky asset classes have come under pressure despite the fact that in the year to date the optimism about an economic recovery has been on the rise. Is that a case of “buy the rumour, sell the fact”? Had the good news already been priced into the market? Or is there another mechanism that could be driving the future development?

Economic growth exceeding expectations

The economic indicators for Q4 2020 exceeded expectations in most countries. The estimate for global GDP growth in Q4 has been revised from 1.3% to 1.8% (relative to Q3) in the year to date (source: Erste AM). The negative effect of the containment measures on economic activity was less significant than envisaged. The manufacturing sector and trade in goods have been particularly strong, surpassing the pre-covid level at the end of 2020.

In terms of growth figures by country, the strong development of the USA (due to public stimulus measures) and Northeast Asia (good epidemiological management; high demand for goods, especially in the IT sector) are standing out. Naturally, the contact-intensive service sectors were most badly hit. The Q1 indicators suggest a deterioration of global growth to 0.5% relative to the previous quarter. However, this decline falls short of previous expectations. For the foreseeable future, the launch of the vaccine programmes, the ample fiscal stimulus packages in the USA and the UK, and generally higher savings ratios among consumers suggest an imminent acceleration of growth. Of course, there are regional differences.

Optimisms: will we be reaching reach pre-covid levels as early as mid-2022?

This environment has caused the upward revision of medium-term (3Y) economic growth projections for some important countries. According to the forecasts, the pre-covid levels (Q4 2019) will be reached sooner than expected, depending on the respective country of course. For example, the European Commission now expects that we will be reaching pre-crisis levels around mid-2022 rather than at the end of 2023. This leads to a slight increase in the medium-term inflation outlook (again, depending on the respective country), because it means better resource utilisation on the labour market and in production(i.e. the negative output gap is smaller than expected). At the moment, consumer price inflation is below the central bank target in the respective countries (which could be reached sooner than expected as well in some cases).

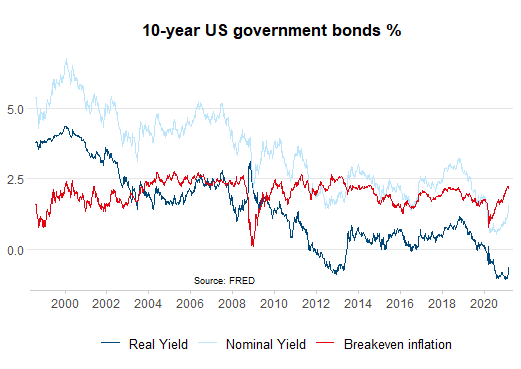

Rising government bond yields

On the financial market, the improved growth and inflation outlook has led to rising government bond yields. The most important referential yield, the 10Y US Treasury bond yield, has increased from 0.91% on 1 January to meanwhile 1.47%.

Two developments are worth pointing out:

- The velocity of the increase has accelerated

- Since January (and in contrast to last year), the increase in nominal yields has not been driven by rising inflation expectations anymore, but by the increase in real yields

The rate of inflation priced into bonds is currently 2.21%, up from 2% at the beginning of January (as of 4 March, 2021; source: Bloomberg). By comparison, the yield net of inflation increased from -1.09% to -0.75%. In recent days, the yield increases have caused the prices of numerous other asset classes to fall. How can that be the case, given the recent rise in growth optimism?

Chart: Structural decline in real yields

Asset prices: growth vs. interest rates

Basically, there are two reasons for falling asset prices: either the future cash flows (or dividends, in case of shares) are called into question by disappointing news, or the interest rates are rising. Recently, the economic news has improved, as a result of which interest rates have increased. This highlights an important underlying condition of the economy: higher growth translates into higher real interest rates. When average income is up, people need an incentive not to spend everything on consumption but instead to invest it. Unfortunately, the bandwidth of sensitivity between real interest rates and growth is wide (0.5% to 2%).

Growing dividends have a positive effect on the share price. Rising interest rates, on the other hand, tend to affect the share price negatively. One of the most important equations in finance illustrates the relationship between interest rates, growth, and asset prices: the price of an asset is the sum of its future cash flows, discounted to the present day.

Generally speaking, the following applies:

- The higher the interest rate, the lower the present value of the future expected cash flows

- The farther in the future the cash flows are being generated, the bigger this effect is (as measured on the basis of the so-called duration). Indeed, last week asset classes with long duration (and high valuation, e.g. technology shares) were hit the hardest

Two core topics

The movement of the real interest rates has a significant effect on the movement of asset prices. One important reason why numerous asset classes have recorded substantial gains in recent decades is that real interest rates have fallen more significantly than the growth prospects.

This results in two core topics:

- When yields are rising structurally (i.e. in the long run), the relationship (i.e. correlation) between equities and bond yields switches from positive to negative. Short-term yield increases could be occurring at the same time as short-term share price decreases, in contrast to what has been happening from the 1990s to now.

- For the medium-term share price performance, the question of whether real interest rates are rising is less relevant than whether they are rising more or less significantly than growth expectations

Challenging yield curve management

As long as the explicit and implicit goals of the central banks such as full employment, long-term inflation at 2%, financial stability, and low interest rates to be able to finance government debt do not get into conflict, everything is alright. However, for the financial market and the government debt momentum, the monetary policy is more crucial (low key-lending rates and high liquidity boost asset prices and vice versa) than for economic growth and inflation (low correlation between unemployment and consumer price inflation, as measured by the Phillips curve). This resulted in a boom on the financial markets. The spreads for country risk have fallen despite rising government debt (e.g. in Italy).

The central banks continue to signal a sustainably ultra-expansive monetary policy: no rate hikes are to be expected in the foreseeable future. At the same time, the expectations for the first interest rate increase priced into the market have moved up: a full step up has been priced in for the USA for March 2023. At the moment, the issue is not that inflation expectations might get out of hand, but that the forward guidance issued by the central bank has become slightly untrustworthy. What makes things tricky at the moment is that yield increases could actually be playing into the central banks’ hands. They reduce the risk of an overshooting on the markets (financial stability). Of course, moderate and slow yield increases are far preferable, as they allow for simultaneous verbal interventions of the “monitoring closely” kind. However, if yields were to continue rising sharply (i.e. by more than growth expectations), the central banks’ yield curve management would become more obvious, because in that case central banks would (probably) try to contain the speed of yield increases with more than just “soft” statements.

Conclusion: the environment will remain supportive to the financial markets. The central banks will contain any excessively strong and quick yield increases. Volatility (i.e. price fluctuations) will probably increase, given that the valuation of many asset classes are above average due to the previous decline in yields. Real yields might have just embarked on an – albeit slight – upward trend.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.