A guide for times when finance without sustainability does not really work anymore.

The strong market growth in recent years of sustainable investment products has produced a variety – if not to say, uncontrolled mushrooming – of investment strategies that makes it hard to recognise such investments at first glance (and even harder to compare them).

In view of the compulsory sustainability advice within the framework of MiFID-II coming into effect in 2022, no asset manager wants to be without their own range of products in this high-growth market segment. The market is being flooded with sustainable (SRI – socially responsible investments) alternatives.

Many investors fail to take the time to look specifically for individual funds in the jungle of more than 1,000 products. And greenwashing is not easy to detect with funds either.

So, is there any relief in times where every player on the financial market is talking about sustainability?

KPIs, ratings, and labels

On the most granular level of the assessment of the sustainable performance of a fund, we resort to individual, very specific indicators from the ESG (i.e. environmental, social, and governance) spectrum. This makes sense if one wants to look at a very specific, partial aspect, e.g. the carbon footprint of the companies that a fund invests in. But unfortunately, this example already pretty much exhausts the rather limited bandwidth of reliable indicators. The data, whose volume has increased sharply within a short period of time, is not particularly systematic or comparable for us to be able to work with more than CO2 data. In the future, this will change due to the obligation to publish data on so-called extra-financial indicators, which will come into effect in 2023. At that point, the growing bandwidth of indicators from the ESG spectrum will also contribute to a more comprehensive evaluation of the sustainability of investments.

Prior to that, though, a rating method that is based on sustainability categories would seem tempting (so-called quantitative portfolio scores). In simple terms, every fund will receive a number of points that are derived mathematically as product of the specific weighting of the portfolio title and the associated ESG score. This method comes with numerous downsides. It only works with companies that have been rated by one of the traditional four big ESG rating agencies. This is not often the case for small or exotic companies, and it is even rarer for states. The company ESG ratings in turn are based on the so-called best-in-class method. This means the companies are rated within their respective sectors. It makes sense to compare Tesla with Toyota, Renault, and BMW, but less so with Carrefour, Tesco, or Metro in a portfolio context, since the challenges in terms of sustainability are different ones. Initial improvements of applying premiums and discounts as well as different grades of controversy on the basis of the respective sector go down that route. It does not help that the results of the ESG agencies differ from each other due to the focus of analysis, the interpretation of missing data, and individual weightings, which is detrimental to an objective rating system. This approach also fails to take into consideration that companies with bad ESG ratings in particular sometimes hold tremendous potential for improvement in their sustainability efforts, so the impact would be much bigger for these companies – which is exactly what sustainable investing is all about.

More and more scientific studies show that effective dialogue methods (i.e. for example engagement and the exercising of voting rights) create a more significant sustainability impact. Purely quantitative ESG portfolios do not take this fact into account.

This means that this method is tempting – as pointed out above – as a single number portrays comparability, but its meaningfulness is ultimately limited. Of course, ESG portfolio scores and ranking percentiles derived from them are a great source of additional information that may complement the assessment of an SRI fund. However, they are no quality benchmark for SRI funds: https://www.fngsiegel.org/media/private/SRI-Ratings_Rankings_Label_Europa.pdf (p. 5).

Quality labels have emerged as most convincing method of assessing the sustainability criteria of investments, not the least in the context of paths towards (more) sustainability for financial investments, the still unsystematic and hardly comparable database, and the various channels by which ESG improvements can be delivered. These are today probably the best tools in the toolbox of suboptimal benchmarks. They focus on the “how” rather than the “what”.

As person in charge of the German-speaking SRI quality label from FNG, the FNG Seal, I would like to introduce you to this seal that we created in 2015.

Wholistic and strict testing methodology / required and voluntary standards

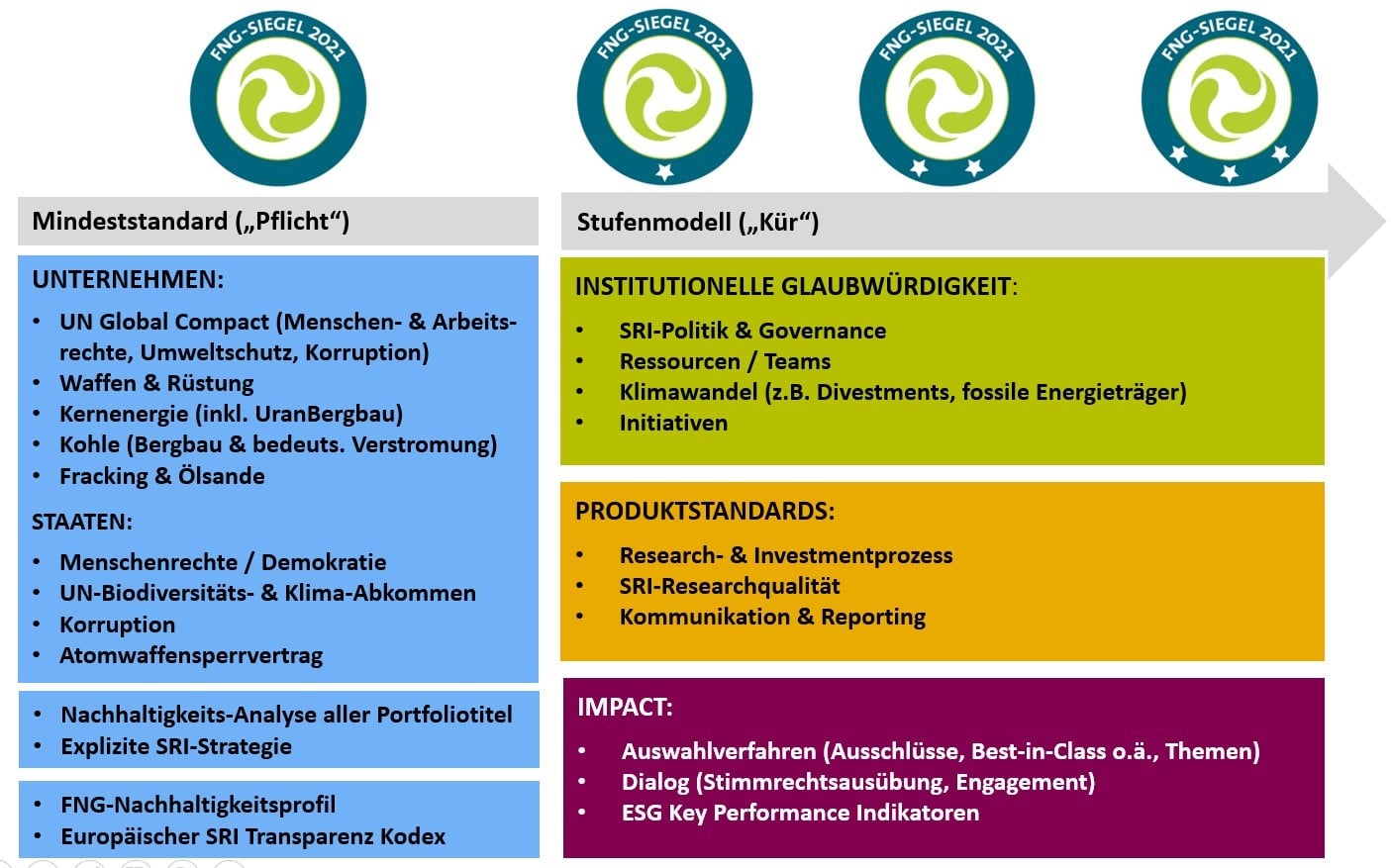

A sustainability fund is more than just the collection of individual titles in a portfolio. Therefore, the focus of the auditing process for the FNG Seal is not only on the investments per se, but all activities of the fund provider – i.e. the infrastructure of the fund – are being scrutinised. To this end, we have developed a comprehensive and multi-layered methodology in a stakeholder process that took us three years and by way of which we can look at individual sustainability approaches that differ from each other. This wholistic approach allows us to evaluate the different paths to (more) sustainability.

The wholistic methodology of the FNG Seal is based on a required minimum standard. This includes criteria of transparency and takes into account work and human rights, environmental protection, and the fight against corruption as laid down in the worldwide acknowledged UN Global Compact. Also, all companies in the fund have to be explicitly scrutinised in terms of sustainability criteria, and the product has to demonstrate an explicit sustainability strategy. Investments in nuclear power, coal mining, significant energy production from coal, fracking, oil sands, and arms are out of bounds. High-value sustainability funds that excel in institutional credibility, product standards, and impact (title selection, engagement, and KPIs) can get up to three stars (voluntary standards).

We use a catalogue of 80 questions to analyse and evaluate for example the sustainable investment style, the resulting investment process, the ESG research capacities related to it, and the engagement process, if any. In addition, elements such as reporting, the monitoring of controversies, an external sustainability advisory board, and the investment company as such play an important part as well. The more layers a fund has and the more intensely it is active across the various layers, the higher its sustainable quality and the potential to achieve indirect or direct impact are.

Cooperation of proven and independent competencies

A quality seal hinges on a certain degree of strictness, independence, and credibility. The audit, i.e. the analysis of the fund, is done by the University of Hamburg, where five chairs and 20 researchers are based at one of the world’s largest know-how centres of sustainable finance. The audit process is also monitored by an independent advisory committee that consists of various members of civil society, among them experts from Österreichische Gesellschaft für Umwelt und Technik (ÖGUT; Austrian Society for Environment and Technology), the University of Augsburg, the impact network GIIN, and the WWF Germany. Funds have to undergo this audit every year.

EU regulatory framework

In addition to the fact that, as part of the efforts by the EU around the issue of sustainable finance, the regulatory framework will soon lay down what kind of criteria financial products have to fulfil in order to be deemed sustainable, the FNG Seal acts as quality benchmark for sustainable investments and provides a pre-selected universe of sound, solid, and externally audited sustainability funds.

It therefore pays off to keep your eyes open when searching for a sound, credible sustainable investment opportunity. When in doubt, ask for specific proof for the sustainability of the investment that you are considering. This may be quantitative indicators in the climate realm or other fields of sustainability that are important to you; it may be ratings (if they are well-made) or renowned quality seals that make a wholistic statement about the quality of sustainability of the financial product in question.

Detailed information and overview of the funds that have been awarded the FNG Seal.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Is the AI Rally Nearing its End?

Following this week’s interest rate cut by the US Federal Reserve, shares related to artificial intelligence (AI) applications are once again in the spotlight. Investors are hoping that AI will have a positive impact on the business figures of the key players. With the ERSTE STOCK TECHNO fund, you can invest in the most important companies in future technologies.