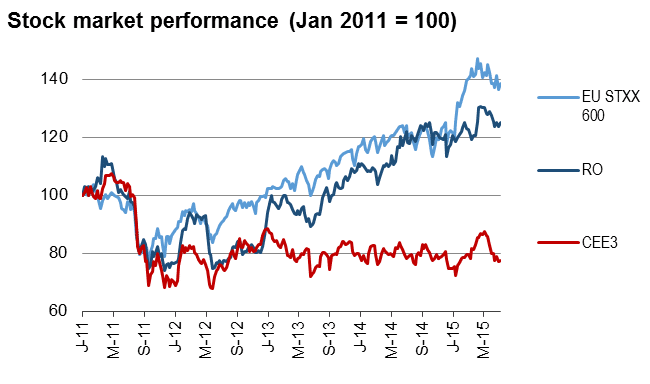

In searching for a perfect example of a sideways market one does not need to look further than at Central and Eastern European (CEE) equity markets. The CECE Composite, a Euro-based index of 23 Polish, Czech and Hungarian blue-chips (Bloomberg: CECEEUR), has been range bound for nearly four years, rarely trading outside a narrow range of ±8% from its mean over the period. A recent spike by 23% that started in January and lifted the index beyond this trading range was halted by the escalation of Greece-related risks. The only market in the region that has participated in the broader equity rally in Europe and the US in recent years has been the Romanian market.

Source: Bloomberg; Erste Asset Management.

Outlook is brightening

Looking into the second half of the year, there are reasons for turning more sanguine on CEE equity markets:

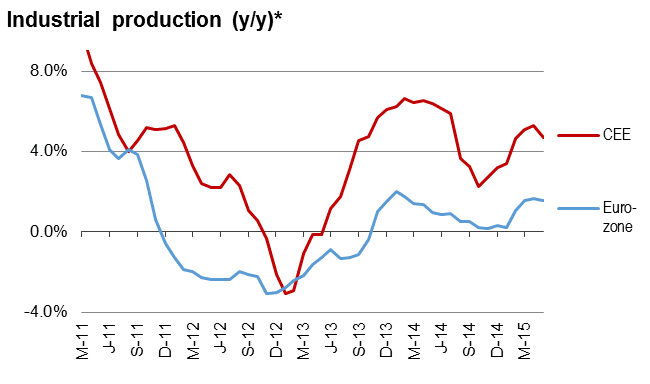

- Growth has been robust: Industrial production in the region continues growing twice as fast as in the Eurozone. Also manufacturing PMIs, which were 1.5-3 percentage points higher in CEE than in Western Europe in recent months, confirm that CEE economies are outgrowing their western European peers. The consensus outlook for the Eurozone suggests that economic growth will reaccelerate in the course of the year, thus providing support for CEE.

- Positive earnings outlook: After four years of decline, earnings growth is turning highly positive. According to consensus forecasts net profits will approximately double in 2015 and moderately grow in 2016.

- Improving profitability: The strong earnings momentum is mainly the result of better operating margins. The average EBIT margin in the market, which nearly halved since 2010 is expected to reach 13% in the current year, and ROE is projected to climb from 4.8% last year to 9%.

- Undemanding valuation: The market is trading on 12.9 times estimated 2015 earnings. Despite the pedestrian price performance in recent years, trailing multiples stayed stubbornly high due to the mediocre earnings performance. Now, as earnings are gaining momentum, forward multiples have dropped from above 15x in the fourth quarter 2014 to their current level of below 13. The discount to core Europe is higher than anytime in the past three years.

- Less challenging risk backdrop: After the avoidance of Grexit, most risk indicators are signaling falling uncertainty, which suggests that markets can expect a bit of tranquility following the turbulence in the second quarter. Greek issues will most likely stage a comeback, but for now Grexit is off the agenda.

- ECB is here to support: Monetary policy in Europe will remain highly accommodative in the foreseeable future. Quantitative easing is finally showing up in the data, and following the Greek spectacle, the ECB will even see less reason to switch to a more restrictive policy stance.

Source: Bloomberg; Erste Asset Management. *) 3-month rolling averages; CEE: GDP-weighted annual percentage changes of PL, CZ, HU, RO, SK.

Risks remain (as always)

While a number of factors signal a better economic and risk backdrop for CEE equities in the near term, both global and homegrown risks remain (in addition to any renewed deterioration of the Greek situation).

The most formidable risks are Chinese growth and financial market risks, which seem contained for the time being, and the rate of rising US rates. In contrast to their peers in the Eurozone, Japan and China the US Fed and the Bank of England have indicated that their policy rates will be lifted in the near future – with the Fed’s move being the much more important move, of course. While the rate liftoff in the US is probably the most widely advertised policy move in financial history, there seems to be still a gap between market expectations (assigning a probability of about 50% to a rate hike this year) and the Fed, which recently has sent stronger signals than before that the economic backdrop is set for a liftoff. While the longer-term fallout from a (moderate) hike should not be overestimated, the immediate response for risky assets such as CEE stocks will be negative.

Finally, also on the domestic front risks are looming, mostly in Poland. The political change in the course of the recent presidential elections are signaling a move towards a less market friendly and more nationalistic policy stance, as exemplified in the recent debate over the ‘repolonization of the financial industry’. Political uncertainty will likely increase in the run-up to the parliamentary elections this October, as investors fear an ‘Orbanization’ of Polish economic polic.

Bottom line: Yes, the backdrop for CEE stock market is brightening, but at the same time there are also good reasons for not getting carried away.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

US elections: are the billions of investments in green technologies at risk?

Two years ago, the USA initiated its energy transition with the Inflation Reduction Act. This was followed by billions in subsidies and investments in renewable energies. What will happen to the Act if Donald Trump makes a comeback to the White House? Is the “Green Rush” in danger of coming to an end?