The year started strongly for European markets with investors favoring Italian banks and stocks. But then came the budget proposal of the new Italian government, changing the mood abruptly.

Italian Banks outperform at the start of the year

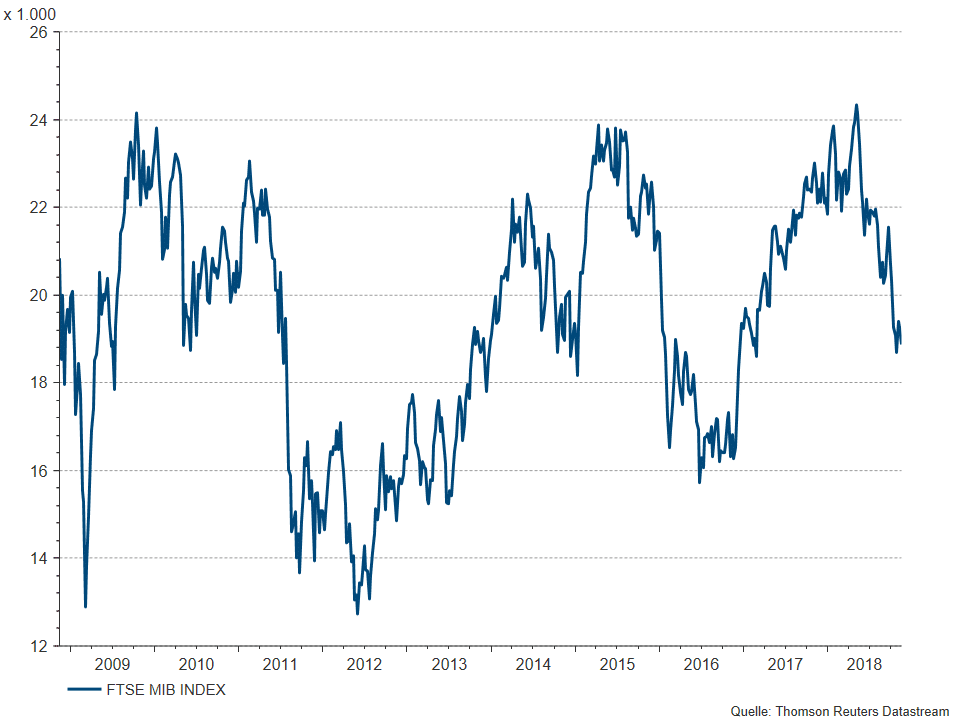

In January, the Stoxx 600, a broad index of European companies, reached its highest level since 2015. The same was true for European Banks (as measured by the Stoxx 600 Banks Index), which climbed almost 5% in the first month of the year. Italian Markets started out even better: the FTSEMIB-Index – which contains the 40 largest Italian companies – grew more than 7% in January and Italian Banks were among the best performing stocks, growing by more than 13%.

After years of disappointing economic data, the Eurozone was able to surprise positively in 2017. Political sentiment in Europe improved considerably, after the market-friendly French candidate Macron was able to defeat the populist threat posed by Marine Le Pen. Sentiment towards Italy saw a sharp improvement also. Following the bailout of Banca Monte dei Paschi, it seemed like the worst period for Italian banks was over. Unicredit – the biggest Italian lender by assets – successfully reduced its high amount of non-performing loans (NPLs), helped by a capital injection. Intesa San Paolo – the other major Italian bank – purchased the Veneto banks, thereby helping sector consolidation. At the beginning of 2018, Italian banks seemed to be on the right track, offloading a large part of their bad loans to private equity firms specializing in buying distressed debt.

Investor´s excitement about cleaner balance sheets was high at the start of the year, bringing the FTSEMIB to its highest level since 2008 in May, outperforming the broader European market.

Italian FTSEMIB-Index reaches highest level since 2008 in May this year

Market sentiment turns negative

If we look at the markets today, however, it is hard to believe that the aforementioned strong performance took place this year. Currently, all major European equity indices are down significantly on a year to date basis, with the Italian Index ranking at the bottom. European banks are down by over 20%. Among the worst performing banking stocks, we find many Italian names, declining by more than 28%. So what has changed?

A lot of the negative performance in European markets can be explained by external factors: the escalating trade war between the US and China, worries about the US economy being late cycle, and the era of cheap money slowly coming to an end are all weighing on investor sentiment this year. In addition to this, the EU also faces a significant domestic problem: Italy.

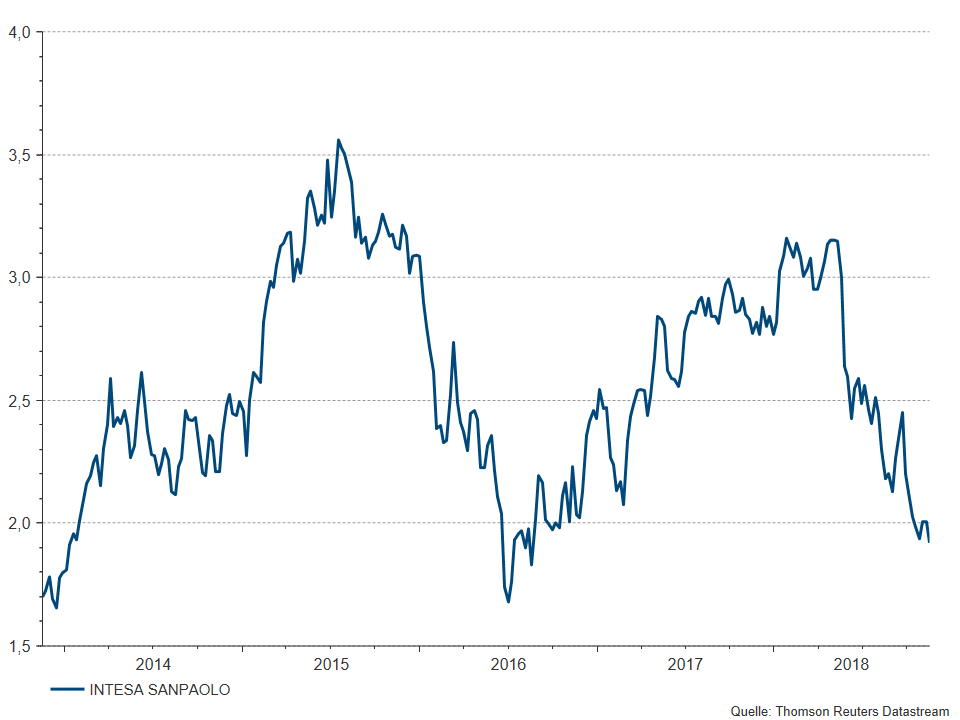

Intesa San Paolo – Italy`s seconds largest bank – lost more than 40% from its high in May 2018

Italy`s debt and asset quality problem

Italy has the 3rd largest economy in the Eurozone. Government debt-to-GDP stands at around 130%, the second highest ratio after Greece, and the highest debt level in nominal terms. Economic growth has been subdued for decades, and nominal GDP is still lower than it was before the financial crisis. The mediocre performance of the Italian economy has had a negative impact on the asset quality of banking loans. In late 2015, non-performing loans (NPLs) accounted for almost 16% of total loans outstanding in the Italian banking system. After selling off parts of the bad loans, this ratio came down to c. 11% in 2017. NPLs affect banks earnings in a negative way, since they have to be provisioned for, showing up as an extra cost on the P&L (profit and loss) account. Further, once a loan cannot be fully recovered, its value has to be written down on the balance sheet. This reduces the assets of the bank, and thereby also lowers the bank`s equity.

The budget dispute between the Italian government and the EU

Due to the country`s high indebtedness and the high share of NPLs, investors became nervous when the newly elected government – consisting of a populist left-wing and a radical right-wing party – unveiled their budget proposal for the coming years. The targeted deficit was announced at 2.4%. By itself, this number does not seem too excessive. The problem lies in heavy spending: the government plans to lower taxes, lower the retirement age, and introduce a basic income to the poor and unemployed. The European Commission (EC) also believes that the Italian government judges GDP-growth too optimistically. Therefore, the deficit could end up higher than the projected 2.4%.

In light of these doubts, the EC did not accept Italy`s budget proposal, and asked for a new budget – an unprecedented move in the EU. The government did not back down from its position, maintaining tension between the two parties. In theory, the EC could fine Italy by 0.2% of its GDP, should the country make no changes to its spending plans. This would equal more than 3 billion euros.

Investor nervousness reflected in higher Italian yields

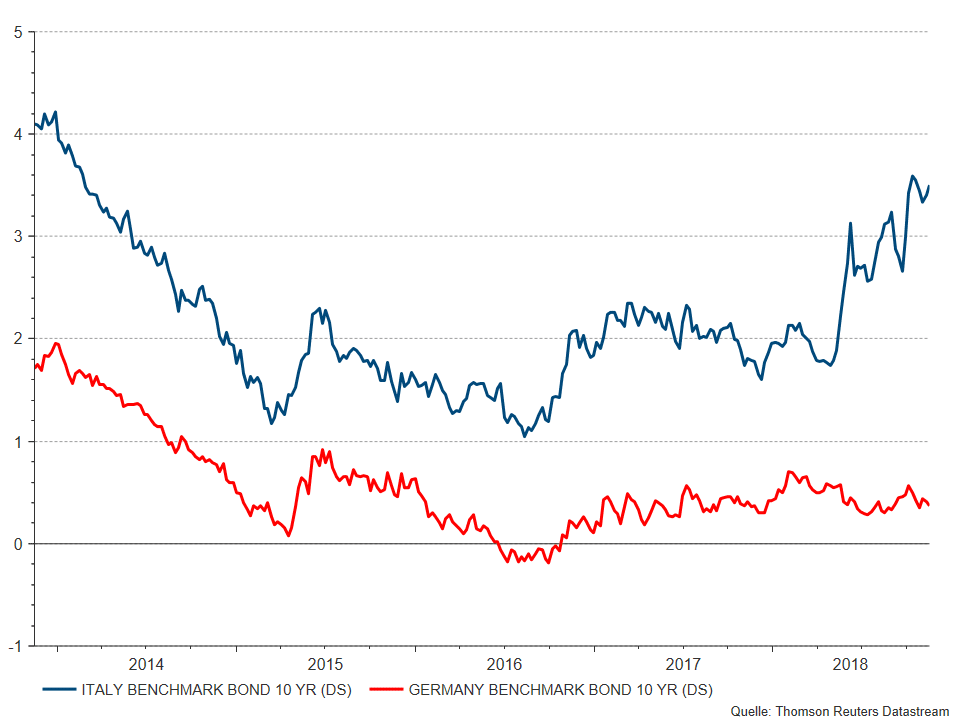

From an investor point of view, the Italian dispute comes at a very bad time. Eurozone growth is still solid, but slowing compared to last year. Nervousness on markets is already elevated due to trade tensions between the world`s two biggest economies. Further, the ECB is gradually paving the way for monetary tightening: QE (Quantitative Easing, standing for the ECB buying government and corporate bonds) is expected to end this year, and the first rate hike is expected towards the end of next year. Italy has a high amount of debt to refinance, and monetary tightening will not make this exercise cheaper. The spread between the 10 year yields of Italy and Germany – a measure of market fear – is hovering around 3%, the highest in more than 5 years. A level of 4% is said to be critical for both, the Italian state and their banks.

The rise in Italian bond yields is also a negative for Italian Banks. Banks in Italy are large holders of Italian debt. An increase in yields results in lower bond prices, shrinking the bank`s assets and again, their equity.

Spread between Italian and German 10 year yields climbs to highest level in more than 5 years

Outlook for European and Italian banks looks challenging

Going forward, the Italian situation will likely be the single most important factor determining the performance of banking shares in Europe. Fundamentally, the picture looks much better for banks than it did a couple of years ago. Capitalization of banks is stronger, asset quality has improved significantly and costs are held under control. Many banks returned to revenue growth in the last years through higher net interest income and higher fees. Also, the big regulatory changes seem to be over. Valuation of the sector is attractive, with a 30% discount to the broader European Market (based on price/earnings for 2019 of SX7P vs. SXXP) and a dividend yield of higher than 5%. For banking shares to outperform, however, investors have to be certain that the third largest Eurozone economy does neither plan to leave the Euro, nor will it run into a debt-crisis. Recent comments from the Italian government point to no quick solution. Positive triggers would come in the form of a lower budget deficit, or a change in government. The most likely scenario however seems to be a prolonged dispute between the EU and Italy, making the environment for European banking stocks a difficult one.

Disclaimer:

Forecasts are not a reliable indicator for future developments.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Turkish financial markets temporarily under pressure following political turbulence

The Turkish stock market has been turbulent recently: the arrest of Istanbul mayor Ekrem Imamoglu caused massive uncertainty. What does the political unrest mean for the Turkish economy and the Istanbul stock exchange?

Environmental stocks: How is the sector faring in the current volatile environment?

The first quarter had a few surprises in store for the markets. The US tariff announcements shook the markets to the core and caused a volatile stock market environment. The environmental technology sector was not spared either. What is the outlook for the sector? We asked fund managers Clemens Klein and Alexander Weiß in a double interview.