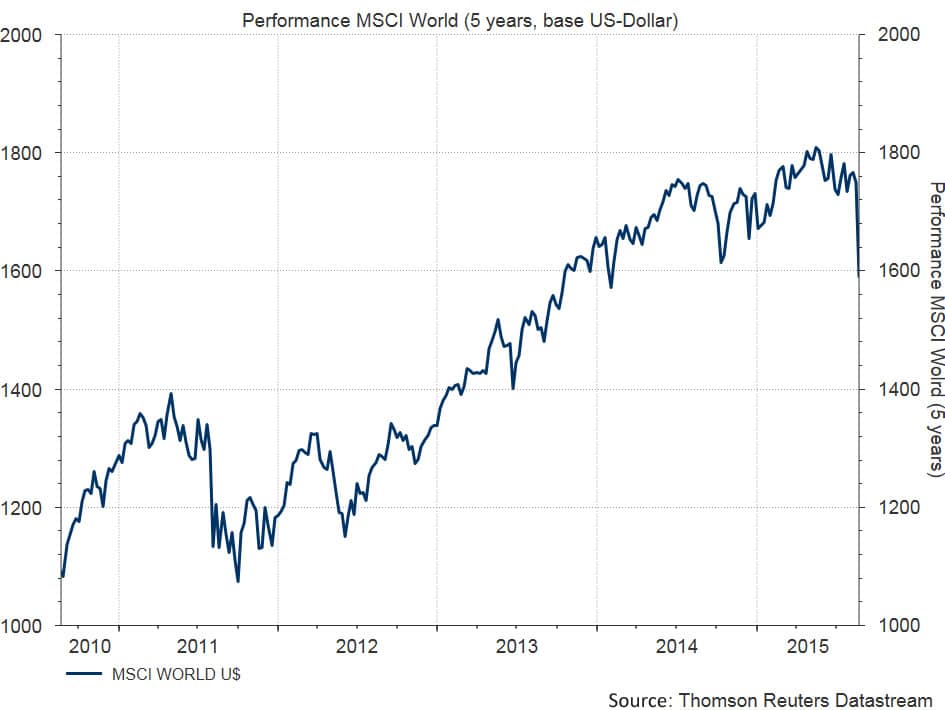

Market correction

Equities, bonds affected by default risk, commodities, and emerging markets currencies are currently subject to corrections, which, noticeably, have now gone beyond the purview of emerging markets: while the emerging markets equity index declined by almost 6% (Performance-Data Source: Bloomberg, MSCI) last week, the index for developed markets lost 5.3% (Performance-Data Source: Bloomberg, MSCI). The fear that the economic weakening in the emerging markets might come with significant spill-over effects for the industrialised countries has increased. This prompts the question whether a phase of profound corrections is upon us in the risky asset classes. The question alone has caused the risk aversion of investors to rise. The liquidity is temporarily parked in safe havens such as US Treasury bonds, the euro, and the Japanese yen.

Devaluation of the renminbi

The most recent price declines were triggered by the devaluation of the Chinese currency relative to the US dollar of more than 4% on 11 August. The markets did not only see the positive effects such as the emancipation from the US central bank and from the US dollar and a more flexible currency but also the possible negative effects such as a devaluation race. The uncertainty alone over how much the renminbi will depreciate has caused depreciation pressure and actual depreciation among emerging markets currencies. At the moment the Chinese currency is about 3% below the exchange rate that had been set by the Chinese central bank on Friday. It would be a comforting signal if the central bank were to intervene and keep the exchange rate stable.

Increase of the Fed funds rate

The market corrections were exacerbated by the expectations of imminent raises of the Fed funds rate in the USA. This underlines the diverging development in the developed and the emerging markets. It makes sense to argue in favour of the key-lending rate to exceed zero percent in view of an unemployment rate of 5.4% in the USA. That being said, the policies of the US central bank are not only relevant for the USA, but also for the global economy. The rising deflationary pressure coming from the emerging markets would certainly go better with monetary loosening than with tightening. Indeed, the inflation expectations priced into the market have already fallen drastically.

Negative spiral

Meanwhile a spiral has been set off: price declines cause capital outflows and a decline in risk appetite. This in turn triggers price declines. In such an environment arguments based on valuation are of little relevance. Calming signals from the Chinese and the US central bank would help the situation, as would additional stimulus packages in China (a cut of the key-lending rate, public investment). However, the economic environment in the emerging markets will remain weak. We can only hope that the deflationary forces on the developed markets will remain in check. At least the most recent indicators in the industrialised economies such as the purchasing managers indices in the Eurozone have suggested continued growth slightly above potential. In the meantime nominal, credit-safe government bonds are the only ones to offer protection against capital losses.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

to the White House")

Best of Charts: The road (in)to the White House

Three weeks before election day, the race for the White House is wide open: While Kamala Harris is ahead in the nationwide polls, Donald Trump is currently likely to be ahead in the crucial “swing states”. In any case, the economic situation and mood in the USA are likely to play an important role in the race for the presidency.