No, this is not an article on football, and any football reference is purely coincidental. This is an article on the football nation whose economy is (finally) showing positive trends and has (finally) been awarded a one-notch rating upgrade by two rating agencies, S&P and Fitch, this year. Only one notch away from the much-desired investment grade rating, the Croatian economy remains on sound footing before tackling its last challenge.

Long story short

When compared to its peer group of SEE countries, Croatia could very well be labelled a laggard. While most of its peers have experienced a double dip recession in the past ten years (exhibiting positive growth rates in between), Croatia’s GDP remained below the line of positive growth for most of that time. Structural imbalances, political instability, high public debt coupled with a high budget deficit and rising interest rate costs due to the lost investment rate rating back in 2013 brought the economy to the tipping point where radical change was needed to reverse existing trends.

Recipe for success

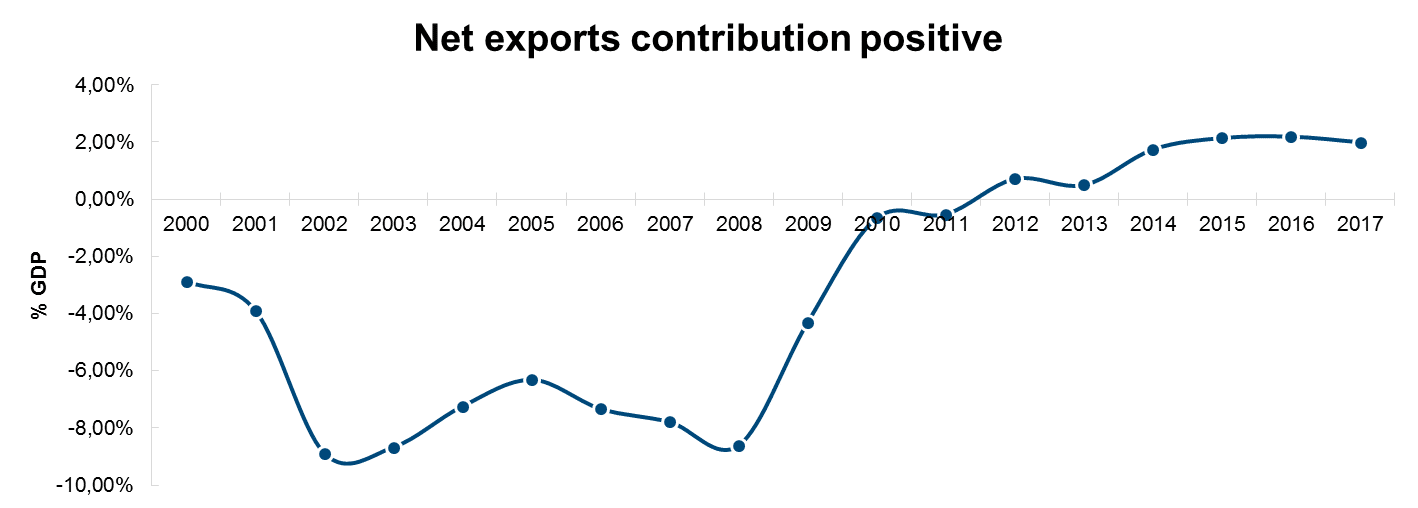

Change (although far from radical) came in the shape of a mini tax reform, record-beating tourist seasons, and improved exports dynamics. The mini tax reform targeted middle class workers by increasing the tax-deductible part of their income and introducing a lower tax rate for their income bracket. This way household demand, which makes up almost 60% of the Croatian GDP, was able to restore its pre-recession growth rate of 3.5%. Exports made huge progress as well, considering that net exports as part of GDP was deep in the red until 2012. This was the result of both booming economies among Croatia’s main trading partners and a hefty 20% contribution of Croatia’s main export product, i.e. tourism, to GDP.

SEE-ing is believing

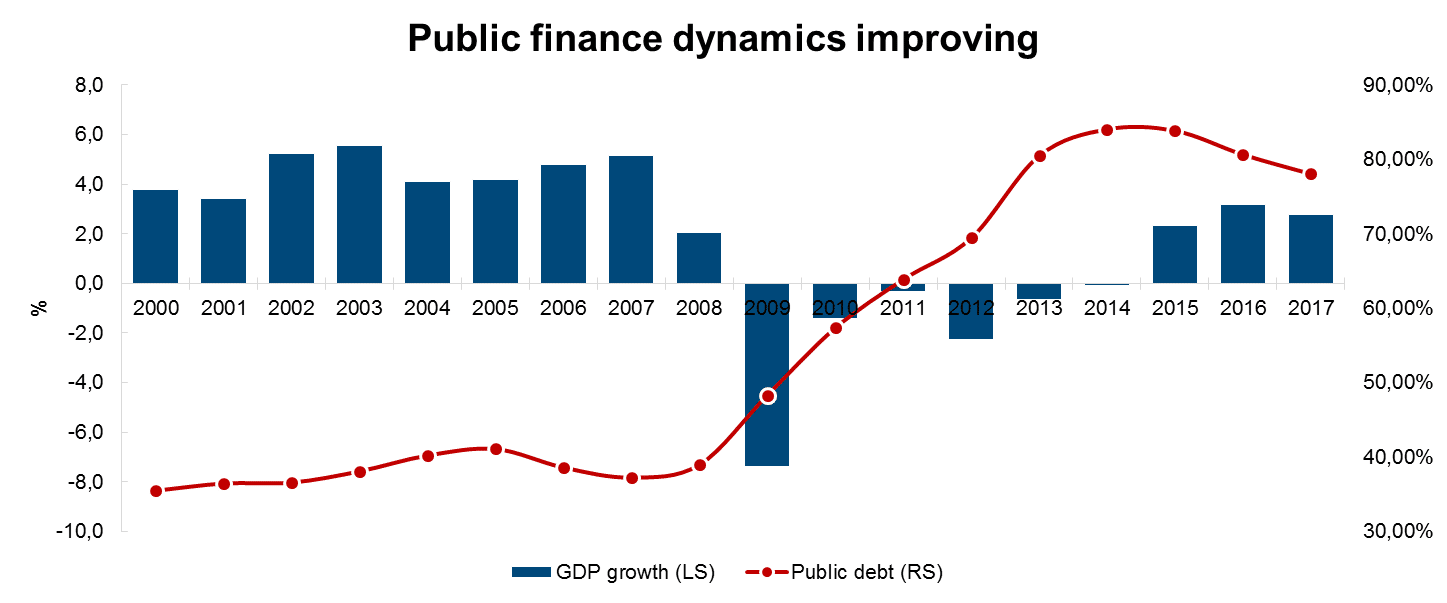

Macro numbers of all our SEE peers look seemingly alike, showing robust growth rates but also a build-up in inflation numbers for those that are financing their growth through higher budget deficits. Croatia is far from it, though. Households are still deleveraging, inflation is anchored around a tame 1.5% level, which supports the ongoing loose CNB monetary policy, banks remain well-capitalised with NPL ratios falling below 10%, and everything looks set for another good year. Public finance dynamics are also improving. Public debt has finally reversed its trend and is currently at 78% of GDP. Government officials expect it to decrease by an annual rate of 2.5%, ambitiously setting their target at 70% for 2020. The EU Commission acknowledged those positive trends by allowing Croatia to exit EU’s Excessive Deficit Procedure in June last year. Most analysts expect the government to be able to maintain fiscal deficits below 3% going forward.

Looking ahead

Current macro and fiscal dynamics coupled with announcements of yet another stellar tourist season lay a solid basis for Croatia to reclaim its lost investment grade rating. It goes without saying that the all-time low spreads show that markets are (once again) way ahead of rating agencies. It remains to be seen whether we will keep up with the pressure. As always, the ball is in our court.

For more information, please visit:

ERSTE BOND DANUBIA

https://www.erste-am.at/de/private-anleger/fonds/erste-bond-danubia/AT0000831409

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.