Last week, volatility returned to the stock markets. The US leading index fell by more than 3.3 per cent. The European markets fell by 1.2 per cent (source: Refinitiv Datastream). The reason for the losses was the tension between hopes for a less restrictive US Federal Reserve and actual inflation and economic data. Producer prices in the US, released on Friday, rose 7.4 per cent year-on-year, more than analysts had expected. The previous day, signs of a slowdown in the labour market had fuelled hopes for a less restrictive monetary policy. The number of applications for unemployment benefits in the USA rose for the third time in a row by 62,000 to 1.7 million – the highest level since the beginning of February.

This week, the financial markets are once again in for an exciting ride: the US Federal Reserve will hold its last meeting of the year on Wednesday. Against the backdrop of the mixed economic data described earlier, we expect the Fed to reduce the pace of its rate hikes from the previous steps of 75 basis points (100 basis points = 1 per cent, note) to 50 basis points. We do not believe that it will be able to send a clear signal of the end of the rate hike cycle as early as December. This will be followed by the European Central Bank (ECB) meeting on Thursday: most economists expect a hike of another 50 basis points. The ECB also wants to decide on important key principles for reducing its balance sheet, which has been swollen by years of bond purchases. ECB President Christine Lagarde had held out the prospect of a measured and predictable reduction in bond holdings.

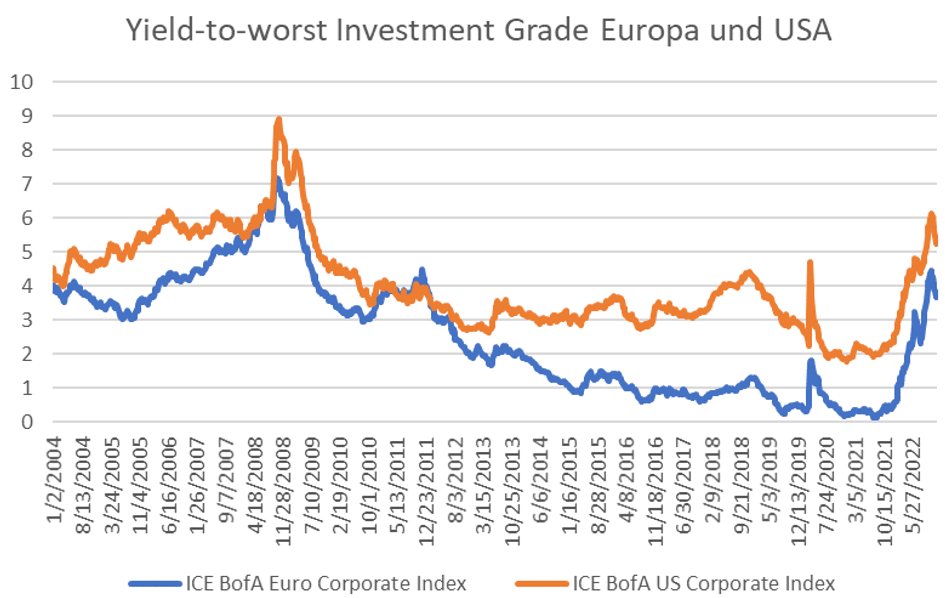

Robust companies

In general, we will keep the risk appetite of our portfolios slightly below the strategic risk budget. The risks of recession have increased, as we have often described. In our opinion, this is already partly reflected in the market prices of some asset classes. This is especially true in the segment of corporate bonds with an investment grade credit rating where we see yield levels averaging over 5 per cent in the US (source: Bloomberg). Even in the event of a global recession next year, we expect the high-quality companies in the investment grade segment to weather it well.

Correction potential for commodities

Energy and industrial commodities are moving in an environment of physical scarcity. OPEC’s policy continues to supporte for example crude oil. Nevertheless, we see a higher correction potential in the event of a recession than for other asset classes. The situation is similar for industrial metals. The necessary and government-supported expansion of renewable energy has a positive effect on the one hand. However, market and valuation aspects also speak against this segment.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.