The US elections in November are not only important from a geopolitical perspective. The market participants, too, are trying to evaluate their implications for the capital markets.

Polls favouring the Democrats

In the polls, presidential candidate Biden is eight to ten percentage points ahead of Trump. This could be due to the negative economic development in conjunction with the (mis)management of the corona crisis and the national protests and riots. However, the gap between Biden and Trump was bigger just a few weeks ago.

While the polls at this point still favour Biden, the shrinking gap suggests that all is not lost for Trump. The economy is recovering, and the campaign rhetoric is extremely harsh and polarising. An additional fiscal stimulus a few weeks ahead of the elections could support consumer confidence, which has fallen.

A national majority is not necessary for a victory in the US electoral system. The president and vice president are elected by electoral delegates from the various States. Winning the relative majority of a candidate in a specific State means that all of the delegates of this State will vote for that candidate. The delegates per State are based on the number of members of the Senate and the House of Representatives.

100 Senators and 435 Representatives make up 535 electoral delegates. In addition, there are three electoral delegates for the District of Columbia, i.e. the seat of the federal government. An election victory requires an absolute majority of 270 electoral delegates. Swing states such as Florida are fiercely contested.

How does the election outcome affect the stock market?

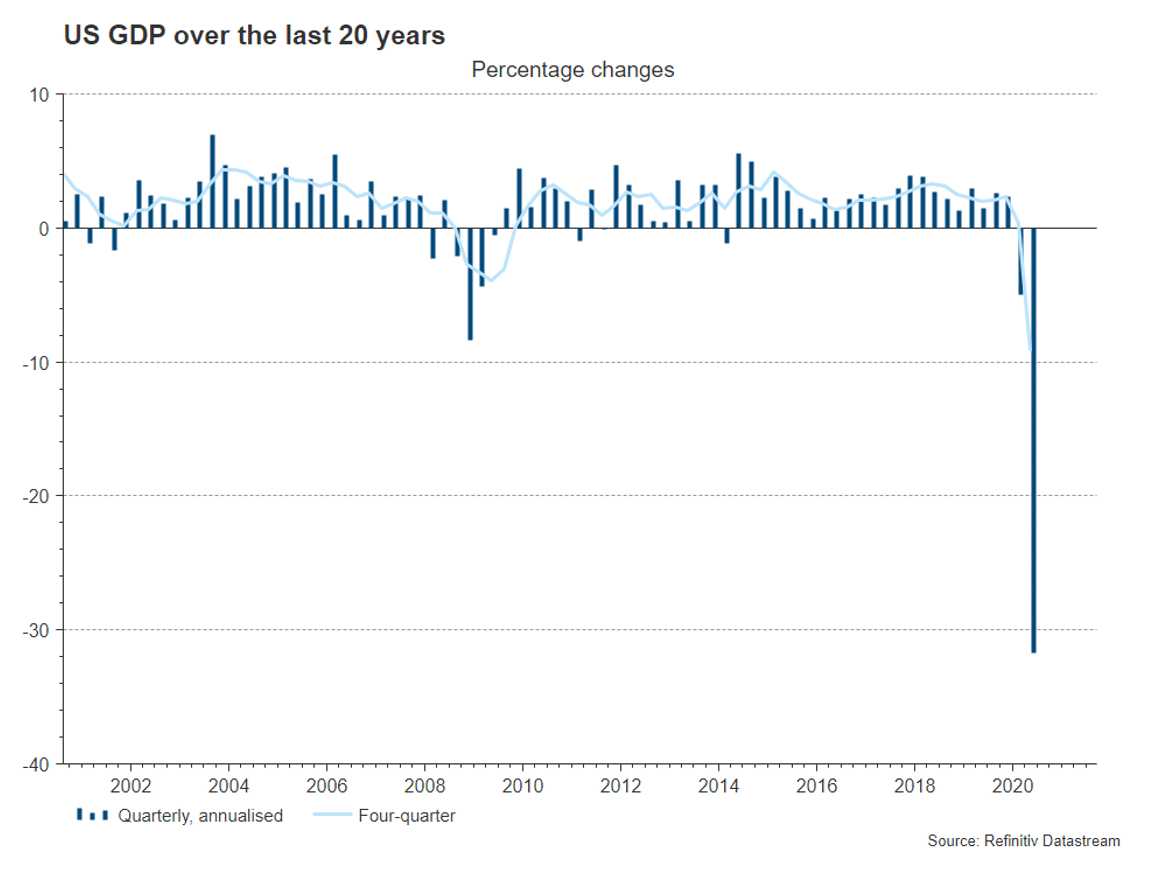

It is a historical fact that the equity indices would often perform worse during the weeks after a Democratic victory than after a Republican victory. Republican election programmes are generally regarded as rather more pro-business, maybe erroneously so.

However, this effect would quickly dissipate in the past. Looking back, we cannot see any clear correlation between political party and stock market performance during the entire term of office of the various presidents. This has less to do with announced vs. implemented election programmes.

On the Republican side, the stagflation in the 1970s (Nixon, Ford) and the recessions in 2001 (tech bubble) and 2007 (Great Financial Crisis) stand out. On the Democratic side, the boom years under Clinton and the recovery in the wake of the Great Financial Crisis are preeminent.

Election programme: protectionisms versus regulation

Only on the surface do the proposals levied by the Democrats present a bigger risk for equities than those made by the Republicans. Trump’s corporate tax cut to 21% is to be partially reversed to 28%. The healthcare system is earmarked for reform. Public healthcare is to be made available by choice.

We have also noticed a generally negative stance vis-à-vis companies with too much market power (oligopolies) throughout the campaign (e.g. the breaking-up of Big Tech). Also, oil and gas production is to be capped, and the minimum wage would be raised from USD 7.25 to USD 15 per hour.

The Republicans, on the other hand, want to de-couple economically from China, they favour more funding for the police, are against immigration, and want to curb the defence budget for foreign deployment.

Both sides argue for an investment programme that benefits the infrastructure. The Democrats focus on renewable energy in an effort to reduce carbon emissions. Both parties are in favour of capping drug prices.

It is unclear whether the tax hikes and more stringent regulation as suggested by the Democrats would hit harder than the protectionism (and the withdrawal of the USA from international organisations) and the conflict with China that would come with a Republican victory. Also, not all suggestions of election programmes are actually put into action. Only in a case where the president is from the party that holds the majority in the Senate is the likelihood of actual implementation elevated. At the moment, the Republicans hold the Senate majority.

Medium-term recovery trumps short-term noise

In the run-up to the elections, harsh rhetoric – especially against China – may affect the market sentiment negatively. After the elections, a victory for Biden could weigh on share prices as a first reaction, because prices are sometimes also driven by headlines of little substance (“tax hike”, “regulation”).

Also, Trump might not accept defeat and go to court. This uncertainty would also be detrimental to market sentiment.

In the long run, the strength of the economic recovery in the coming years will probably be driving the markets. This is ultimately due to one key parameter: the federal budget. The more expansive the budget policy (i.e. high budget deficits) – and both parties basically favour this approach – the more favourable is the outlook for the economic recovery and thus for equities.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.