The countries of Central, Eastern and Southeastern Europe are among the most important economic growth markets for Europe. But while the CEE economies grew at an above-average rate in 2018, a Vienna Institute for International Economic Studies (WIIW) forecast published last week concludes that economic growth in some of these countries could slow down in the coming years. However, according to the WIIW forecast, not all countries are affected, and the reasons for this are diverse.

Growth by and large between 2 and 3 per cent

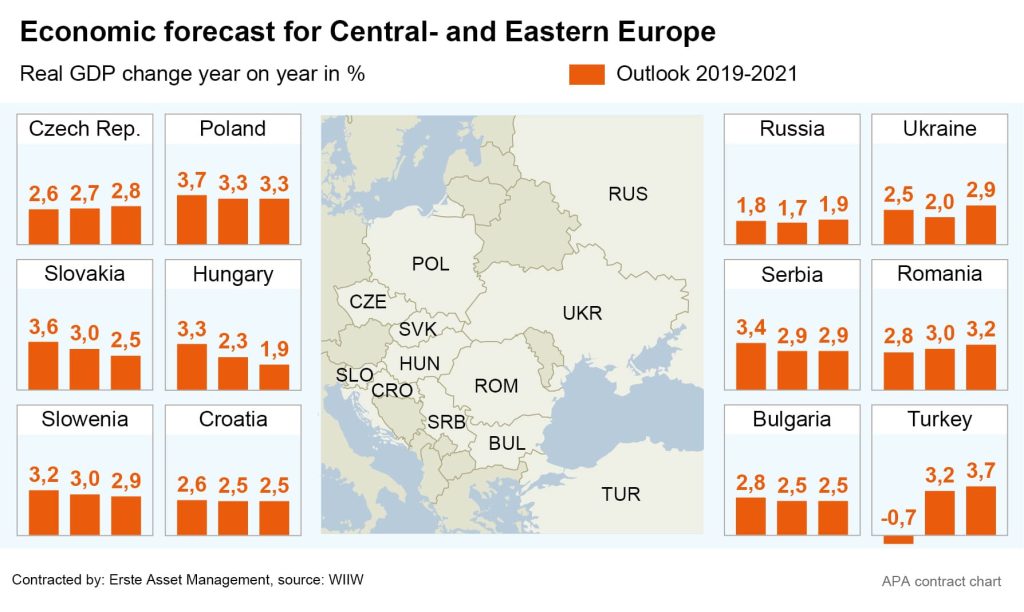

For example, the Czech Republic, Poland, Croatia and Slovenia, are all showing signs of largely constant economic development, with GDP growth in the forecast period (2019 to 2021) expected to be well above 2.5 per cent – in the case of Poland even well above 3 per cent. And while relatively low annual growth of between 1.7 and 1.9 per cent is expected in Russia, this constitutes a constant development rather than a deterioration.

Recession in Turkey

At first glance, the two exceptions are Hungary and Turkey. While Hungary’s GDP increase could drop from 3.3 per cent to 2.3 next year and to 1.9 per cent the year after that, a recession of minus 0.7 per cent looms in Turkey this year. After Poland, Hungary has recently been the region’s fastest growing economy. The fact that the picture here could be somewhat clouded by comparison is mainly due to the fact that the EU member has already used up a large part of its budgeted Community funds. In Turkey, there are already signs of significant renewed growth of 3.2 and 3.7 per cent for 2020 and 2021 respectively.

Global economy weakening

The main reasons for the slight downtrend, according to the WIIW economists, are global factors such as a generally slower growth of world economy, the consequences of US protectionist measures and the potential effects of Britain’s withdrawal from the EU. In the case of the Brexit, the extent depends strongly on whether the British can still agree on a treaty with the remaining EU states. Fortunately, a “hard Brexit” without agreements is still anything but certain.

While increasing tension is evident in the labour market and property prices in Central and Eastern Europe, this is not a problem on an aggregated level, according to the WIIW. In addition, currencies are proving surprisingly stable: “Inflation is surprisingly low in the majority of the region, especially considering the rapid rise in wages and the rise in oil prices last year,” the study authors explain.

The challenge of qualified labour shortage

In order to ensure solid long-term growth in the CEE countries, WIIW recommends decisive action to tackle the challenges facing the region, in particular the sharp rise in wages due to the shortage of qualified labour that is further exacerbated by remarkable demographic changes. The Vienna Institute considers rapid automation in the export-dependent industry a priority. The study authors also call for increased investment in education and training to make Central, Eastern and Southeastern Europe fit for the new digital economy.

Stock market players still in buying mood

Just how exciting the region remains for investors is shown by the development on the capital markets. The CECE index determined by the Vienna Stock Exchange for the stock exchanges in Budapest, Prague and Warsaw, for example, has risen by 4.1 per cent on a euro basis since the start of the year, with individual fund products showing even stronger results.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

The Sahm Rule: What is behind the recession indicator?

The Sahm Rule, an important recession indicator in the US, was triggered at the beginning of August – causing uncertainty on the markets. We explain what is behind the indicator and why everything could be different this time.

US draft budget: “The rules of the game for renewable forms of energy are changing”

The recently published US budget draft also contains interesting passages on the future of the Inflation Reduction Act and the associated subsidies for renewable energies. In an interview, environmental equity fund manager Alexander Weiss explains what the draft means for investors and why the market reacted positively to it.

Eastern Europe: Economies expected to outperform Euro Area

Weakening growth in the eurozone has been an issue on the markets for some time now. In the Central and Eastern European countries, however, this is largely a non-issue. According to forecasts, the region is also likely to grow faster than the eurozone this year. Private consumption in particular has recently proved to be a growth driver. However, the tense situation in German industry is causing concern.