Alexandre Dimitrov, Manager des Aktienfonds ERSTE STOCK RUSSIA

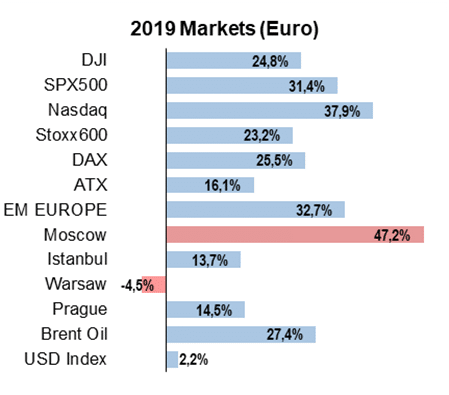

Equity investors had every reason to be cheerful last year: share prices were up pretty much across the board in 2019. The Dow Jones gained almost a quarter, while the US technology share index Nasdaq even soared by 38 percent. But these were outdone by the shares listed on the Moscow stock exchange, which increased by 47 percent (see the table below).

In this interview, Alexandre Dimitrov, fund manager of ERSTE STOCK RUSSIA, explains the reasons behind the share price gains. He expects growth to speed up in 2020.

Change in stock market value 2019 (in Euro)

Source: Bloomberg

The Russian equity market saw a fantastic year 2019, contrary to the expectations of most observers. Where did this strong performance come from?

(c) LUKEOIL

This positive performance was due to a variety of factors: on the one hand, the oil price rose by 27 percent (Brent; in euro; source: Bloomberg), which also drove shares in the oil sector up. OPEC had announced production cuts. The share price of Lukoil reached an all-time high, while Gazprom gained 80 percent. On average, oil shares gained 47 percent in 2019. The interest rate cuts by the Russian central bank from 7.75 percent to 6.25 percent also contributed significantly to the newly sparked bull market. In addition, the foreign exchange reserves of the central bank increased to USD 500bn, which gives the bank quite a bit of leeway with regard to its interest rate policy. Lastly, the rouble gained 12 percent relative to the euro over the year 2019 (source: Bloomberg).

All of that sounds very positive, but the sanctions against Russia and also the economic growth, which is on the weaker side, could result in a slowdown in 2020?

To be fair, the political framework has been challenging since the Ukraine crisis, and we have lived with the sanctions for a number of years as well. Investors have to take this into account as political risk. But I should also point out that three quarters of the Russian equities are held by US investors. Things may therefore not be as bad as they seem. Of course, new conflicts could crop up at any time and affect stock exchange performance. As investors, we get our bearings by looking at the economic framework, the interest rate policy, and the earnings history and forecasts in the corporate sector. This approach has paid off, because it is these parameters that are relevant on the stock exchange in the long run.

What is the outlook for Russian equities in 2020 according to Erste Asset Management?

At +1 percent in real terms, the Russian economy recorded rather restrained growth last year. The consensus expects an acceleration to +1.8 – 2.0 percent for 2020 (source: consensus estimates, Bloomberg). The rising real income, driven by the low unemployment rate of 4.6 percent, is a positive factor. Much like 2019, the entire equity market will be fuelled by the high dividend yield of about 7 percent and rising dividends by state-affiliated companies in 2020. As for the interest rate policy, the central bank has room to manoeuvre for further rate cuts. Stock exchanges are fond of falling interest rates and stable prices.

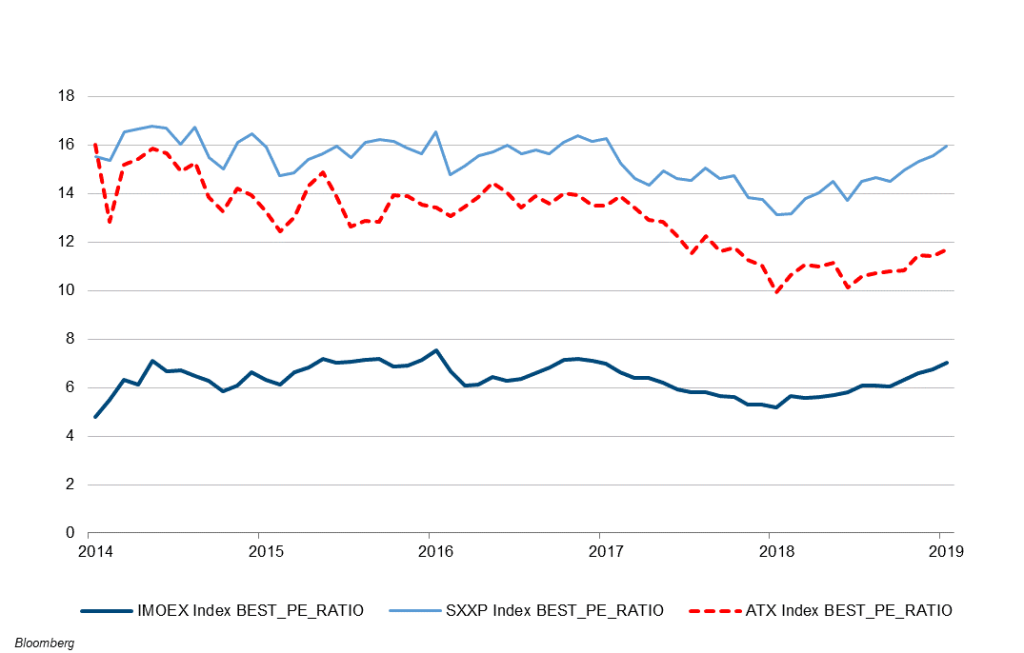

Price/earnings ratio relative to Europe and Austria

This means that as a tendency, company earnings will be on the rise?

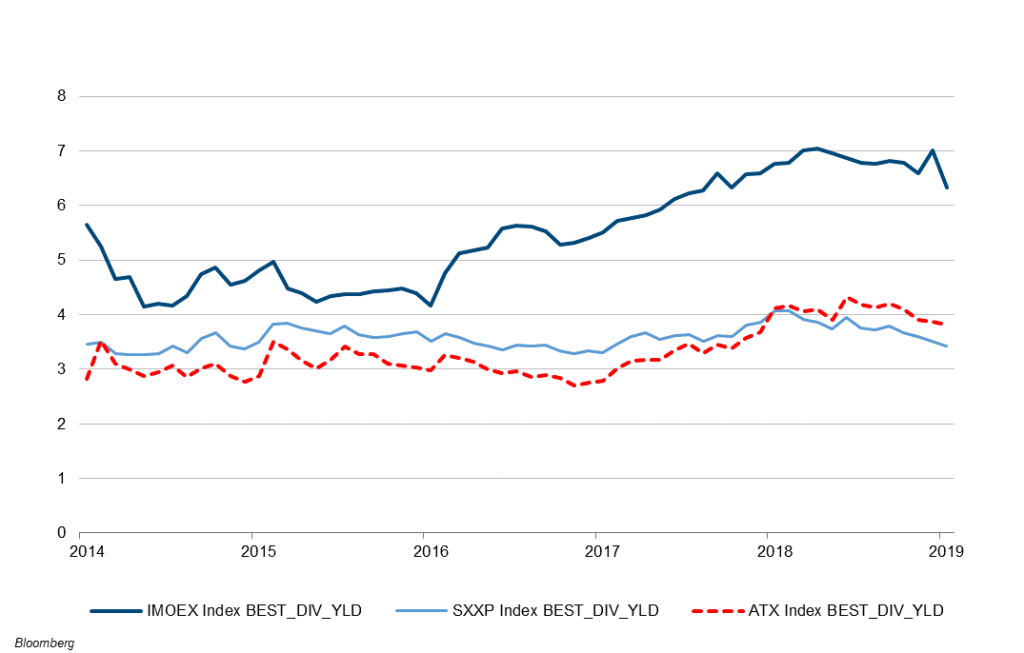

Yes, telecom companies could post earnings growth of about 17 percent, consumer goods even 20 percent. In the financial and real estate sectors, earnings are expected to rise by 10 percent to 20 percent. All in all, the earnings situation therefore comes with upside potential. At a price/earnings ratio of 7x and a dividend yield of 7 percent, Russia commands the lowest equity valuation and at the same time the highest dividend yield among its stock exchange peers.

Expected dividend yield 2020 for Russia, Europe, and Austria

What companies have caught your eye?

A good example (heavyweight in the portfolio) for the market performance and the expectations is Lukoil. This oil company is now paying out 100 percent of the free cash flow it generated and has also already launched its second share buyback programme. Overall, we expect the dividend yield to rise above 10 percent in the coming two years. Lukoil is heavily weighted in the equity fund ERSTE STOCK RUSSIA. Other prominent examples of companies that have stepped up their dividend payouts considerably are the mining company Norilsk Nickel, one of the main beneficiaries of the demand for batteries, the world’s largest natural gas producer, Gazprom, and the largest Russian mobile telephony provider, Mobile TeleSystems.

It is not straightforward for retail investors to buy Russian shares directly. Equity funds such as ERSTE STOCK RUSSIA offer investors a comfortable opportunity to buy several of the most attractive shares, starting from EUR 50 per month. What is your current positioning in the fund? What sectors do you prefer for 2020?

ERSTE STOCK RUSSIA holds a concentrated portfolio of 27 shares that we regard as attractive and imbued with upside potential. Energy accounts for 40 percent, but given that the sector already posted significant gains in 2019, we have now slightly shifted our focus to financials, consumer goods, and telecoms. We continue to find good investment opportunities in the metal and mining sector. Generally speaking, we prefer companies with strong balance sheets and high dividend payouts; and ideally, they should be market leaders in their segment.

Conclusion:

After the strong year of 2019 at the stock exchange, chances are that share prices will continue to rise on the Moscow stock exchange in 2020. The accelerating economic growth, the extremely low share price valuation, and the high dividend payout ratio make Russian shares one of the most attractive stock exchange segments. The political situation should neither improve nor deteriorate. Investors have to be prepared for share price fluctuations, be it up or down. A long holding period is advisable.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.