The Presidency of the Council of the European Union caught Romania in a difficult position, both from a political and macroeconomic perspective. Following multiple blows to judicial system from part of the Government ruled by the Socialist Democrat Party, Romania’s commitment to the European values has been rightly called into question. Moreover, Romanian Government ability to lead through a tough European agenda including Brexit negotiations, trade relationship with the US and immigration issues is another difficult point as domestic challenges take the limelight.

A new fiscal revolution

Mounting pressure on the budget deficit and the Government’s attempt to keep it within 3.0% of GDP led the Minister of Finance to announce at the end of last year a new fiscal revolution, after the one introduced for 2018. The Government approved through an Emergency Ordinance key fiscal changes for 2019, with major negative impact on key sectors of the economy, such as financial, energy and telecom.

The main fiscal measures include a progressive tax on banking assets, which is linked to money market rates. This effectively is a blow to monetary policy independency, as hikes would lead to a permanent increase in money market rates, with negative impact on banks profitability and thus affect financial stability. As a consequence, banks will most likely revise their strategy and tighten lending conditions. Moreover, the Government introduced a turnover tax to companies operating in the energy and telecom sectors. These taxes will significantly reduce potential economic growth, tighten financial conditions and lead of lower investments. On February 4th, the Central Bank Governor will have a formal meeting with the Government, where we expect these issues to be discussed and potential amendments to be proposed.

The Ordinance also includes changes to the mandatory private pension system (Pillar II), after many months of speculation. Although the approved version waters down the initial proposed changes, the implications remain significant and even question the future of the Pillar II in its current structure. The Government decided to lower the management fees paid to the existing pension fund managers significantly, while demanding these managers to increase substantially the capital requirements. In the long-term Romania is facing a significant demographic problem and thus jeopardizing the future of the private pension system while increasing the public sector pensions creates the perfect formula for failure.

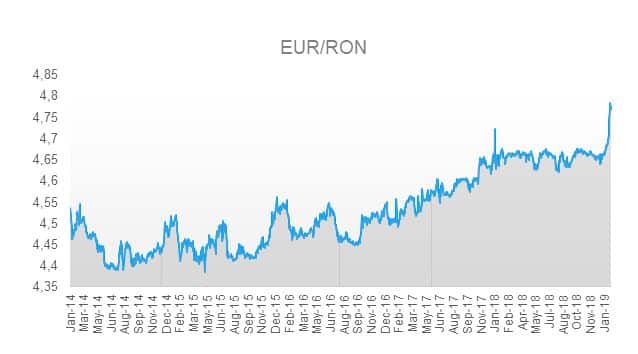

Source: Bloomberg for the EUR/RON chart

A clear downtrend in RON assets

Investors’ cautious view on Romanian assets due to deteriorating macroeconomic fundamentals and significant policy uncertainty started being reflected more significantly in the assets’ prices. Facing a twin deficits challenge, RON lost 2.3% against the EUR this year, making it among the worst performing EM currencies year-to-date. The tight grip of the Central Bank on the currency prevented large movements in 2018, although the ballooning twin deficits increased market expectations of a weaker RON. As annual inflation dropped to 3.3% in December, within the inflation target interval of 1.5% – 3.5%, the Central Bank allowed RON to depreciate in nominal terms against the EUR more substantially than in the past. In the long-term, some of the new taxes could be passed on to consumers, while RON depreciation will add to the inflationary pressure. Thus, the Central Bank is caught between a rock and hard place, trying to juggle both money market rates and the exchange rate. Fighting RON depreciation through FX intervention will lead to higher money market rates, which could put pressure on the financial system stability through the higher tax rate. However, given the important FX pass-through to inflation, too much RON weakness could jeopardize the inflation target.

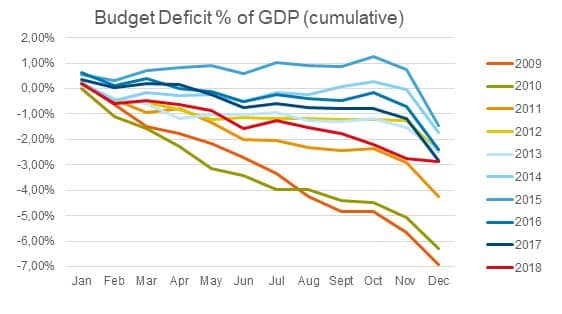

Source: Ministry of Finance for the Fiscal Deficit chart

Quo vadis, Romania?

The fiscal deficit for 2018 printed at 2.88% of GDP on a cash basis, barely below the 3.0% threshold, and the Government is yet to publish a budget draft for 2019. The fiscal package approved at the end of last year is unlikely to cover the gap and keep the deficit within the 3.0% of GDP limit, especially when considering the planned hike in pensions starting in September this year. Consequently, we could see further fiscal tightening measures announced in the coming weeks. In light of this, we are cautious on the RON until there is further clarity on the fiscal package and potential changes to it.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.