With increased geopolitical uncertainties and the central banks’ interest rate turnaround, 2022 will be remembered as a year of great change and upheaval. On the stock markets, the year that is slowly coming to an end was characterized by high volatility due to these developments. Tamás Menyhárt, senior fund manager, therefore draws an initial summary of the stock market year 2022 and ventures an outlook for the coming months on the markets.

The markets have been volatile so far in the second half of 2022. Do you see prices rising again in the long term in the foreseeable future or will we have to prepare for a difficult environment in 2023 as well?

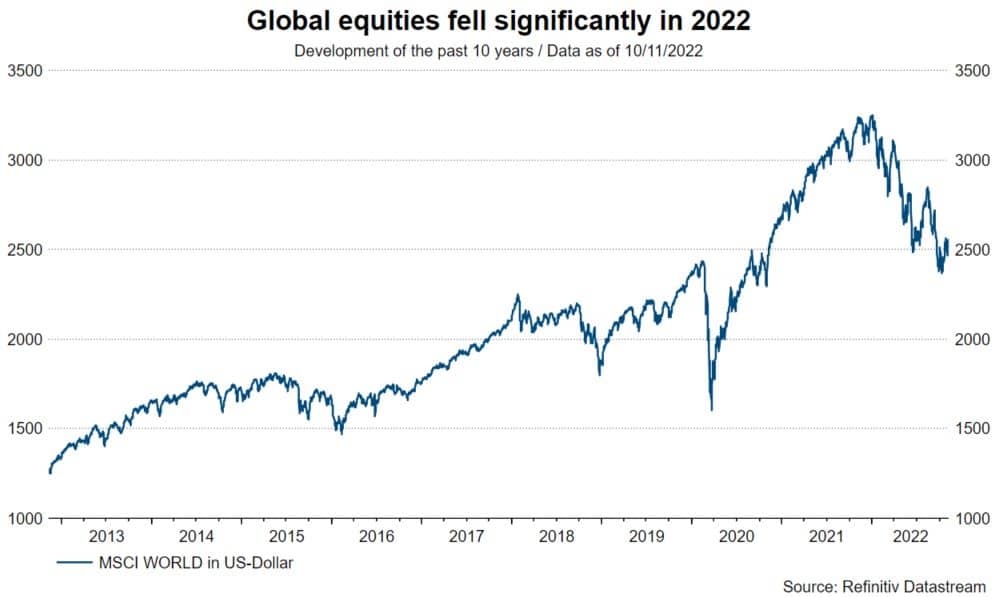

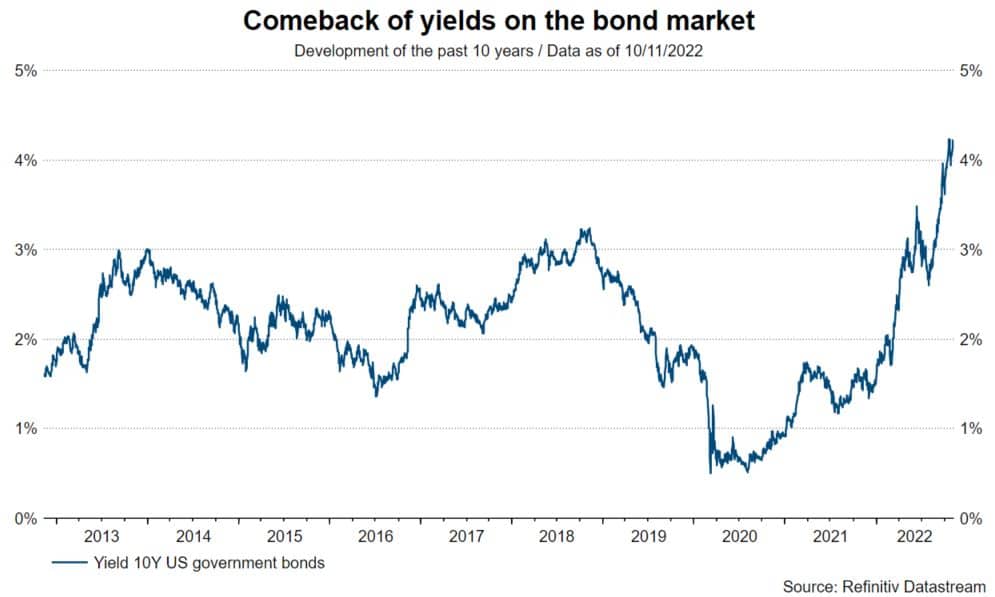

2022 turned out to be a tough year for equities. The main driver of the negative performance was the monetary tightening stance of central banks all around the world. We started the year with an inflation rate running well above the usual target of 2%. The Russian aggression in the Ukraine only made matters worse. As a result, 10-year bond yields in the US climbed to levels not seen since 2007. The increased risk-free rate has put equity valuations under immense pressure, as investors now demand a higher return on their risky investments. The S&P 500 currently trades at a forward P/E of roughly 16 times, whereas we kicked off the year at a multiple above 22x. This equals a contraction of almost 30%.

Note: Past performance is not a reliable indicator for future performance of an investment.

While valuations have come down significantly, a material relief on this front can only be expected once terminal rate expectations (= the interest rate level at which central banks stop hiking) in the US and elsewhere stop rising. For illustration, the market currently expects the fed funds rate (= the interest rate set by the Fed) to go up to over 5%, whereas a month ago the expectation was for 4.6%, and in August it was only at 3.6% (!). Therefore, one of the main questions right now is at what time a slowing inflation rate will allow the Fed to pause its rate hiking cycle. Whenever that happens, equities should start performing again.

Financial markets have gotten used to a long period of cheap money. Now investors have to adopt to a higher yield environment going forward. If short-term rates stop rising, and the world economy manages to avoid a hard landing (= recession), then market participants will see positive returns again. However, the combination of higher rates and higher inflation will keep prospective returns more subdued than was the case in the previous years.

Note: Past performance is not a reliable indicator for future performance of an investment.

The quarterly reports and the outlook of some “tech heavyweights” have disappointed and caused significant losses in the shares of Amazon and Google, for example. Are these already signs of a possible recession in the USA?

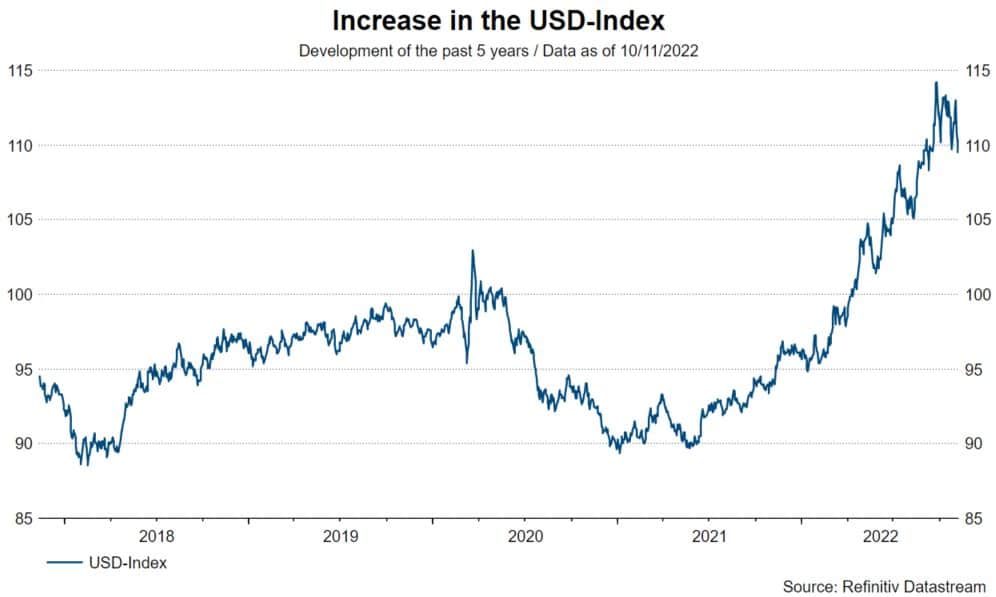

We are almost through with the reporting season, and overall, companies reported solid numbers. Among the S&P 500 companies, c. 70% were able to top analyst estimates, whereas more than half of the Stoxx 600 European names surprised positively. Earnings growth has slowed considerably versus the previous quarters, and there was a significant discrepancy in performance of the various sectors. Banks for example reacted positively, as it became clear that their net interest income (= the difference between a bank`s interest income and its interest expense), which is the main revenue source for most lending companies, benefitted strongly from rising interest rates. On the other hand, major tech stocks like Google or Amazon tumbled following their earnings announcements. This is due to a mix of lower advertisement and other spending from customers and negative currency translation effects from the strong USD.

Note: Past performance is not a reliable indicator for future performance of an investment.

Clearly, the lower level of spending can be explained by a slowing economy and recession fears. High inflation lowers the disposable income of many, and corporations are becoming more cautious with their spending in light of elevated inventories and a slowing demand. As a result, overall earnings growth among US companies fell to its lowest level since the third quarter of 2020.

What about the valuation of the stock market? Do you think that shares in general are now valued at a more realistic level again or is there still further downside potential here?

As discussed in the beginning, market valuations have come down quite sharply due to the increased yield environment. For most indices, valuation multiples are now below their 5- and 10-year averages. Therefore, I would argue that equities as an asset class do no longer look expensive and forward P/Es seem healthy. There are two factors which could put further pressure on valuations from here: an unexpected shock (i.e. further geopolitical escalation) and falling earnings expectations. While none of these can be ruled out, the risk to them is moderate. On the geopolitical front, a lot of the risks is well known and already priced in. Regarding earnings, it is important to understand that in contrast to “normal” recessions, the current economic slowdown is accompanied by rising price levels. Since earnings are measured in nominal terms, they can stay flattish even when profit margins decline. As a result, it is fair to assume that even in the case of an economic contraction, earnings will hold up better than in previous cycles.

Putting everything together, current equity valuations look healthy and the risk of further multiple contraction is moderate. The real trigger for equities will be when lower inflation data will allow for a less hawkish stance of central banks. Until then, investors will have to endure high volatility but should not lose sight of attractive entry levels for their long-term investments.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Sovereign defaults and their debt restructuring

A glance at history shows that it is not unheard of for a state to go bankrupt. How does an entire country actually go bankrupt, what are the consequences and how do you react to this in fund management? Fund manager Felix Dornaus explains this in his blog post.