A long period of price stability ended in 2021 with an inflation shock. Inflation skyrocketed in Europe at that time due to supply shocks in three main areas:

- the energy sector,

- the supply chain,

- and the labour market.

The European Central Bank’s (ECB) problem was that it could not influence the oil exports from Russia nor China’s corona policy. The monetary policy can only mitigate the historically tight labour market by dampening demand and raising the nominal cost of investment. At the same time, the idea was to lead households to save more due to higher interest rates and thus push back consumption into the future.

The open question now is whether these supply shocks also have a structural effect on inflation – i.e. lead to structurally higher inflation. A non-linear version of the Phillips curve could shed light on this. This relates inflation to labour shortages and goes back to the British economist and statistician Alban Phillips.

Inflation, unemployment, and job vacancies

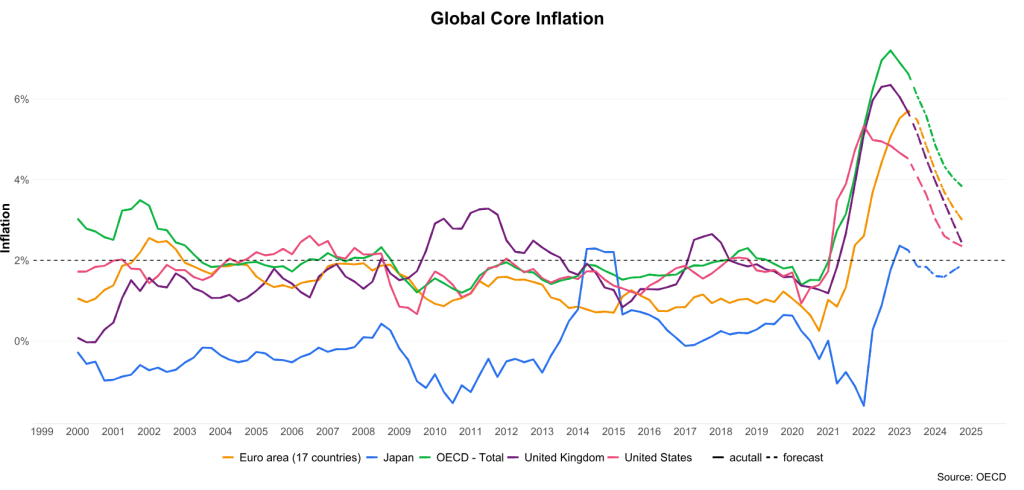

On the global level, inflation itself shows a mixed picture. Using estimates from the Organisation for Economic Co-operation and Development (OECD) and excluding food and energy, we can see that core inflation in the four largest economies, i.e. the USA, the Eurozone, Japan, and the UK, has developed as follows.

Inflation in the USA remains high but is already showing a faster downward trend and was never as high as in Europe to begin with. According to OECD forecasts, the core rate will be close to the Fed’s inflation target by the end of 2024.

In the UK and Europe, inflation declined more slowly and is now at a plateau. In the UK, inflation has declined faster than expected and both are now hovering at similar levels. However, the OECD estimates that the Bank of England can tackle inflation faster than the ECB. A possible explanation could be the higher sensitivity to the oil price, but also the weak economic environment in Germany.

Figure 1: Global core inflation rate – Eurozone – UK – Japan – OECD average – Source: OECD; Please note: past performance is no reliable indicator of future value development.

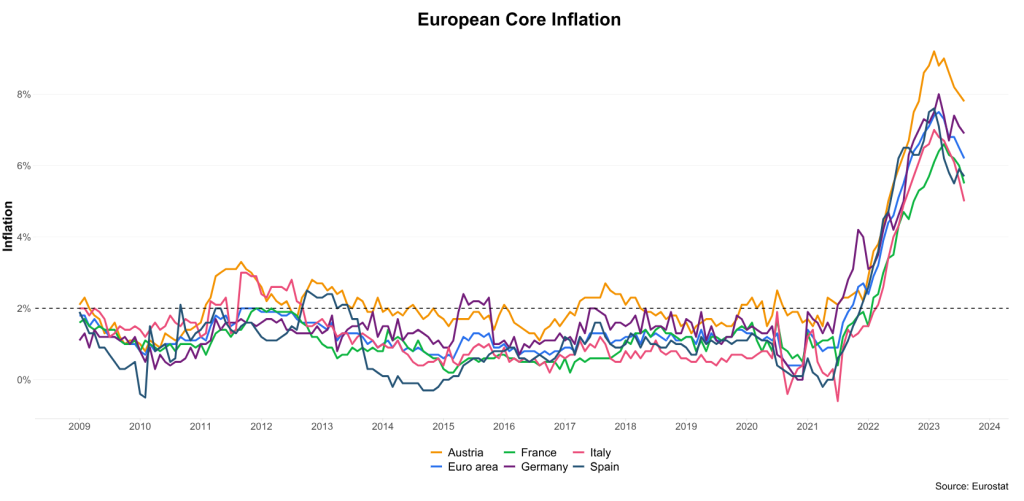

Also, the latest estimates in Austria suggest that inflation rate rose again in August from 7.0% to 7.4%, which in turn could indicate that the inflation wave has not subsided completely yet.

Inflation still has to decline drastically for the European central banks to reach their inflation targets. Meanwhile, Japan has broken a three-decade tradition of near-zero price increases with a sharp rise in prices. OECD forecasts now foresee inflation at the two per cent target, which is a common target for central banks.

Figure 2: European core inflation rates; Please note: past performance is no reliable indicator of future value development.

Figure 2 shows inflation in the intra-European area for the four largest economies and Austria. The blue line represents the average inflation of the Eurozone.

After the euro crisis, the ECB tended to struggle with deflationary tendencies because of the uncertainty around the euro. Countries in the south of Europe were battling high unemployment rates because they could not absorb the shock of the euro crisis through devaluation. Growth was generally weaker and investment lower, so inflation was not a problem for the period following the euro crisis.

This changed with the pandemic. The zero-covid policy of the Chinese central government led to a global supply-side shock. Suddenly, important components for the production of goods in Europe were no longer available or could only be procured at much higher prices. In addition, Russia’s invasion of Ukraine caused natural gas prices in Europe to skyrocket.

We can now see a slight recovery in inflation rates, but the process is very slow. Austria is a negative outlier here. The large number and volume of one-off payments, pension increases, and generally loose fiscal policy during the pandemic put a lot of money into circulation. The consequences will probably continue to be felt and Austria will tend to be in the upper third in terms of inflation rates for the next few quarters.

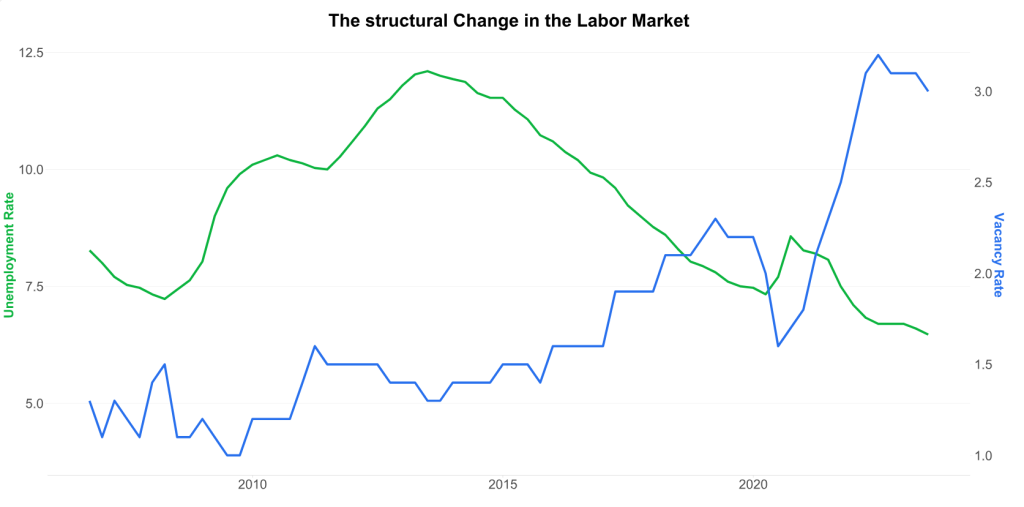

The phenomenon of the historically tight labour market

However, there is still a structural change in the labour market that could prevent inflation in both the USA and Europe from reaching the previous level for longer. The labour market has fundamentally changed after the pandemic. Prior to the pandemic, there were many job seekers in the market, and the unemployment rate was very high due to the euro crisis.

Figure 3: The structural change on the labour market; Please note: past performance is no reliable indicator of future value development.

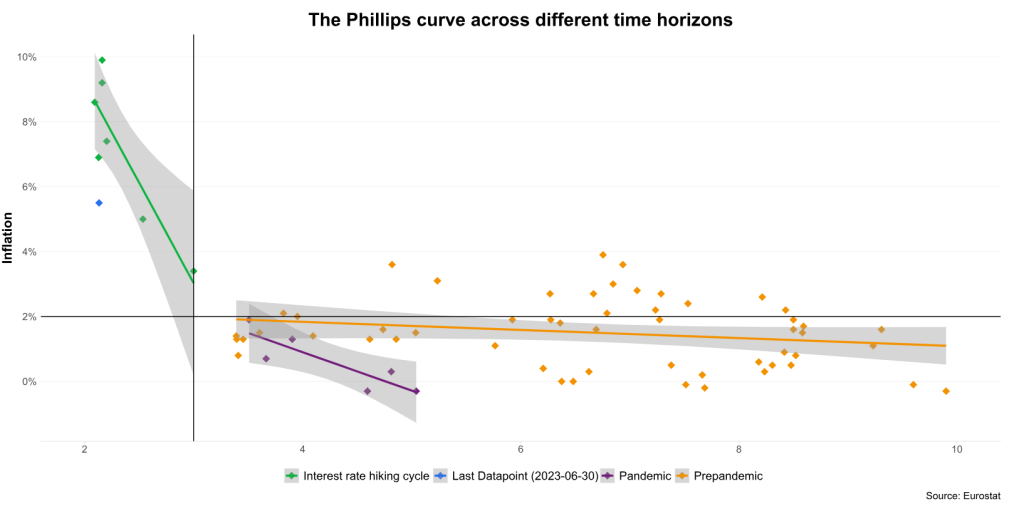

In addition, job vacancies, i.e. newly created or unfilled positions, were scarce, which had a negative impact on wage growth (figure 3). The ratio of unemployment rate to job vacancies is shown on the X-axis in figure 4; inflation is shown on the Y-axis.

Due to the aforementioned relationship in the labour market, the Phillips curve was horizontal for over ten years. Tightening in the labour market had no effect on inflation (see purple line). Also, the extraordinarily high unemployment rates in the immediate aftermath of the euro crisis were not deflationary because the ECB’s quantitative easing pushed interest rates to historically low levels, which led to a positive wealth effect. When interest rates fall, bond prices rise.

As a result of the pandemic, the relationship in the labour market changed. The unemployment rate fell while job vacancies increased. This trend was already present before the pandemic but was exacerbated during the period of 2020 to 2022. The Phillips curve also steepened (blue line). However, there was no price pressure due to the shutdown of the economy. Pressure only started when the economy reopened and important intermediate goods (primarily from China) and labour force were missing.

In the still ongoing cycle of interest rate hikes, both imported goods and labour were in short supply. Job vacancies relative to filled positions increased to 3% and have remained at this all-time-high level ever since. In Austria, the ratio is 4.7%.

The low ratio of unemployment to vacancies led to inflation becoming more sensitive; the Phillips curve became very steep (orange line). Thus, the fiscal policy has also become inefficient. Every additional euro the government spends does not increase growth, but inflation. That being said, a steep Phillips curve also has a positive effect.

Figure 4: The Phillips curve over different time horizons; Prepandemic = before 31.01.2020, Pandemic = 31.01.2020 to 30.06.2021, Interest rate hike cycle = 01.07.2021 to 30.06.2023; Please note: past performance is no reliable indicator of future value development.

Assuming that the Phillips curve remains stable (and consistently steep) with well-anchored inflation expectations, it supports the idea that a relatively small easing in the labour market in terms of a reduction in labour shortages can bring inflation down from the current high levels (see orange line).

The required easing in the labour market can be achieved either by an increase in unemployment or a decrease in job vacancies. As the central banks have often communicated, they assume a “soft landing”. This means that job vacancies will decrease without a drastic increase in the unemployment rate. However, this assumption is increasingly being called into question. The economy urgently needs skilled workers to drive the energy transition, decoupling from China, and digitalisation. Thus, it is increasingly unlikely that job vacancies will quickly reduce on their own without a recession.

The risk of structurally higher inflation in Europe has increased in recent years. Assuming that job vacancies remain at 3% (relative to filled jobs), the European average unemployment rate would have to rise to at least 9%-10% for the labour market to ease from an inflation perspective. At the moment, the unemployment rate is around 6.5%.

How should investors react?

In general, central banks (both the Fed and the ECB) are assuming a soft landing. However, the market is increasingly assuming no landing at all – meaning that inflation will remain high and thus interest rates as well.

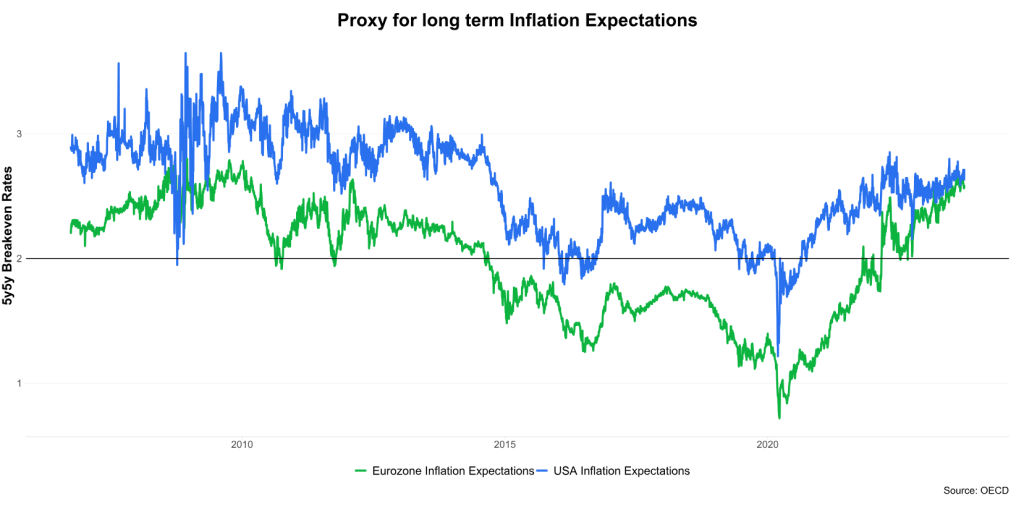

Long-term inflation expectations have increased in Europe in recent years. In general, inflation and interest rates used to be lower than in the US. Now, Europe is at a similarly high level to the USA, although it is worth noting that on both sides of the Atlantic long-term inflation expectations seem to be anchored above the central banks’ inflation target. However, while GDP growth in the USA is at 2.1%, in Europe it is only at 0.5%.

Figure 5: Eurozone inflation expectations – USA inflation expectations; Source: OECD; Please note: past performance is no reliable indicator of future value development.

These circumstances are being priced into the markets as we speak. Interest rates at the short end of the yield curve remain high, while long-term rates are currently still rising. As a result, we can see a slightly steeper yield curve. Provided inflation continues to prove persistent, short-term rates would then remain high while long-term rates would rise (long-term bond prices would fall). Hence the following conclusion:

Conclusion

If one believes in a sustainable steepening of the Phillips curve, the interest rate duration risk (more information on duration can be found here) in the portfolio should only be increased slowly – for example, up to the 5Y range as in the case of the funds with a fixed maturity. If no easing can be observed in the labour market, the interest rates for longer-term bonds could approach those of shorter maturities.

Another argument is that with products closer to the money market, such as ERSTE RESERVE CORPORATE or ERSTE RESPONSIBLE RESERVE, you retain your options for uncertain times. Waiting is not directly linked to losses in coupon payments. As an investor, you currently get a higher interest rate for 2Y German bonds (3.2%) than for 10Y German bonds (2.9%).

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Risk notes ERSTE RESPONSIBLE RESERVE

For further information on the sustainable focus of ERSTE RESPONSIBLE RESERVE as well as on the disclosures in accordance with the Disclosure Regulation (Regulation (EU) 2019/2088) and the Taxonomy Regulation (Regulation (EU) 2020/852), please refer to the current Prospectus, section 12 and the Annex “Sustainability Principles”. In deciding to invest in ERSTE RESPONSIBLE RESERVE, consideration should be given to any characteristics or objectives of the ERSTE RESPONSIBLE RESERVE as described in the Fund Documents.

Advantages for the investor

- Investment in selected bonds from sustainable (ethical) issuers.

- Good security through issuers with very good to medium credit ratings.

- Small price fluctuations due to investments in bonds with variable interest rates or short remaining terms.

Risks to be considered

- Rising interest rates can lead to price declines.

- Deterioration in credit ratings can lead to price declines.

- Capital loss is possible.

- Risks that may be significant for the fund are in particular: credit and counterparty risk, liquidity risk, custody risk, derivative risk and operational risk. Comprehensive information on the risks of the fund can be found in the prospectus or the information for investors pursuant to § 21 AIFMG, section II, “Risk information”.

Risk notes ERSTE RESERVE CORPORATE

Advantages for the investor

- Broad diversification in selected short term or variable-rate corporate bonds.

- No currency effects due to currency hedging.

- Opportunity to earn attractive annual payouts.

Risks to be considered

- Deterioration in credit ratings can lead to price declines.

- Rising interest rates can lead to price losses.

- Capital loss is possible.

- Risks that may be significant for the fund are in particular: credit and counterparty risk, liquidity risk, custody risk, derivative risk and operational risk. Comprehensive information on the risks of the fund can be found in the prospectus or the information for investors pursuant to § 21 AIFMG, section II, “Risk information”.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Trump’s tariff plans: a game with no winners?

On 20 January, the world will once again look to Washington with anticipation as Donald Trump is sworn in as US President for the second time in front of the Capitol. In any case, his statements and plans are already the focus of attention on the financial markets.

Trump is planning high import tariffs for goods, for example from Mexico and China. The possible consequences range from the threat of a trade war to a comeback of inflation. In the end, will no one benefit from the planned tariff measures?

Autumn on the stock markets will be anything but boring

Election campaign, interest rate turnaround, sluggish growth in Europe – there should be no sign of autumn fatigue on the stock markets. What will the coming (and certainly exciting) weeks bring for the markets and how can investors prepare for them?