Autor:

Autor:

Christian Gaier, Head of Fixed Income Rates, Sovereigns & FX, Erste AM

I would like to share my impressions from my latest investor conference in London that I attended on 16th January 2017. The conference was organized by Banco Bilbao Vizcaya Argentaria (BBVA), a leading global financial group with a strong franchise in 35 countries and a leading position in the Spanish market and in Mexico. For us, a perfect partner when it comes to research on countries and companies in Latin America (LATAM).

At the conference, top representatives from Central Banks in Colombia, Argentina, Peru, and Mexico shared their insights with us. The general tone for international investors turned out to be quite friendly. Please find out why.

2017 looks to be a turnaround for some LATAM countries

Although facing a tough environment, 2017 looks to be a turnaround year for some of the struggling Latin American (LATAM) countries. External factors weighing on them are the sluggish global growth outlook, expectations of rising US interest rates, tightening external conditions that potentially come with a negative impact on portfolio flows, and probably no upside surprises in commodity prices. On top of that, political risk is on the rise on a global scale with Mr. Trump as the new US president. This risk can be interpreted as asymmetric with a downside bias for LATAM.

We expect LATAM to post higher growth rates in 2017 than in 2016, with the exception of Mexico, the country the most exposed to changes in US trade policies. The major growth drivers are externally dominated and are based on improvements in terms of trade, which means that for every unit of exports sold a country can buy more units of imported goods. Peru, Colombia, and Argentina are also said to have a well-stocked investment pipeline. Furthermore, stable commodity prices during 2017 could generate more stable cash flows for states that strongly rely on commodities such as Chile, Colombia or Peru and could therefore act as buffer to higher US rates, which could in turn lead to tighter financial conditions.

About one third of emerging markets government bonds stem from LATAM issuers

Let us take a closer look at the market size. With regard to hard currency issues, Latin America makes up almost 40% of the total face value of bonds outstanding in emerging markets globally. We are talking about a total market value of about USD 170bn (source: JP Morgan). The local currency market is even larger with a market value of about USD 420bn and LATAM issuers accounting for 30% of this pie (source: JP Morgan). The relevance of the quality and rating of these issuers to the manager of an emerging markets fixed income fund is obvious.

LATAM currently offers the highest yields within the GEM (global emerging markets) universe

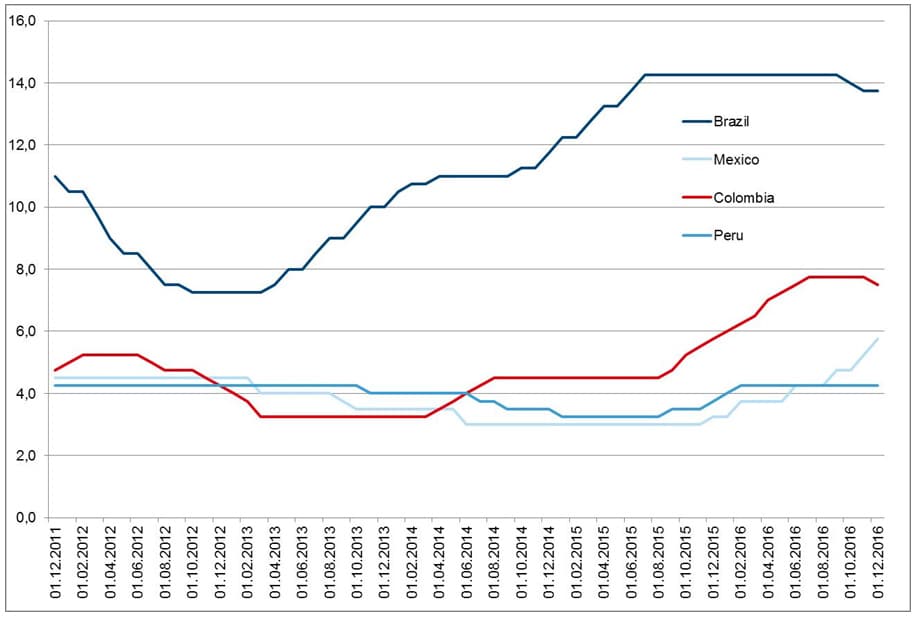

LATAM is the high-yield region in the emerging markets. Having struggled economically and politically already during 2016, these countries were forced to do their homework earlier than others. Current account and fiscal adjustments will start to materialize during 2017. The relief from inflationary pressure gives some of the central banks room to manoeuvre and to cut rates.

Key rates / central bank rates in comparison (Brazil, Mexico, Colombia, Peru) 2011-2017

Source: Bloomberg; data as of 26.1.2017

Heterogeneous fundamentals across countries in this region show the need of diversification and differentiation. LATAM assets make up a significant part of our global emerging market government bond strategies. From our point of view, the outlook for these bonds is positive, given the yield premium that they offer in comparison with euro-denominated assets. If you share this view, one of the following bond strategies could be interesting for you as well:

Emerging market bonds in US dollars and euros, with currency hedging:

Bonds in local currencies from emerging markets:

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Trump’s tariff plans: a game with no winners?

On 20 January, the world will once again look to Washington with anticipation as Donald Trump is sworn in as US President for the second time in front of the Capitol. In any case, his statements and plans are already the focus of attention on the financial markets.

Trump is planning high import tariffs for goods, for example from Mexico and China. The possible consequences range from the threat of a trade war to a comeback of inflation. In the end, will no one benefit from the planned tariff measures?