In Germany the economy entered a technical recession in Q1. The main reason for this was falling consumer spending by inflation-stricken consumers.

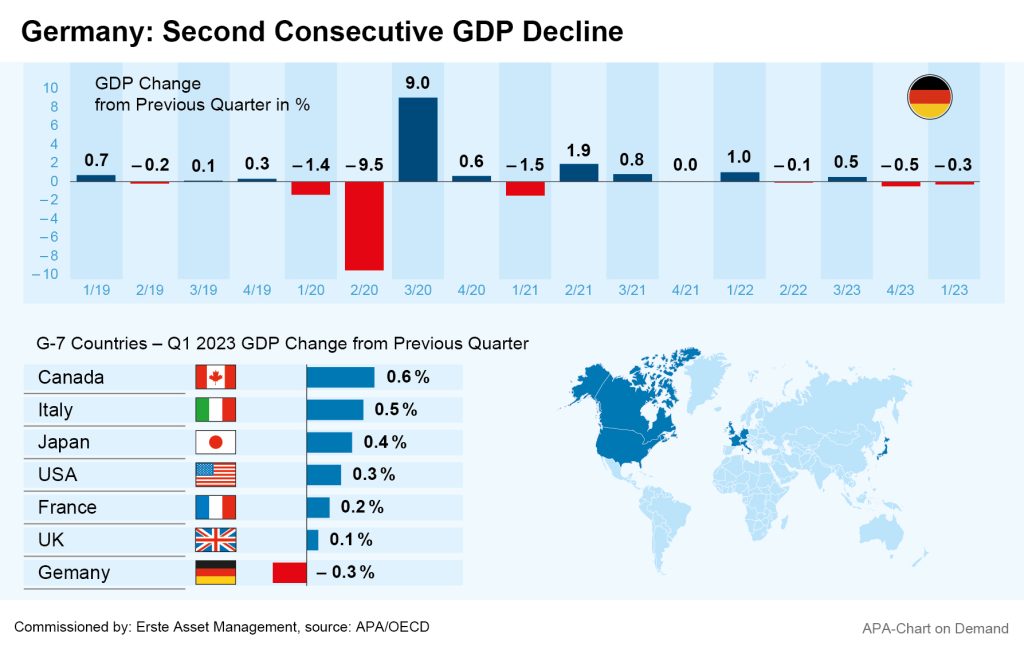

According to the latest figures released by the Federal Statistical Office, the country’s gross domestic product (GDP) dropped by 0.3 per cent between January and March compared with the previous quarter. This marks the second consecutive decline, as the GDP had already fallen by 0.5 per cent in Q4 of last year. What does that mean for the German economy and what is the outlook for the second half of the year?

Recession – one term, many definitions

Germany has entered a so-called “technical recession”, as the most common definition of a recession – two consecutive quarters of shrinking economic output – has been met.

Among economists, however, it is disputed whether this simple definition alone is sufficient to speak of a recession, i.e. a significant and general downturn after a phase of economic growth. This definition is merely the best-known of several approaches to defining a recession, with other attempts at an economic definition also take into account parameters such as production capacity utilisation, demand or the situation on the labour market.

Inflation and loss of purchasing power dampen private consumption

The German economy was impacted by shrinking private consumption, which declined by 1.2 per cent in the first quarter. One reason for this is likely to be consumers’ loss of purchasing power due to the high inflation. While employees’ gross monthly earnings saw the strongest increase since 2008, growing by 5.6 per cent between January and March in a YoY quarterly comparison, consumer prices rose by an even stronger 8.3 per cent in the same period, according to the Federal Statistical Office.

Government consumption also fell by 4.9 per cent in Q1. However, a positive stimulus for the economy came from investments, which grew by 3.9 per cent, as well as foreign trade.

Latest data shows improving consumer sentiment

A ray of hope for a recovering consumer sentiment comes from the latest indicators. The consumer climate index calculated by the market research institute GfK recently improved for the eighth consecutive month following noticeable wage increases. The institute forecasts a 1.6-point increase for its consumer climate barometer in June, bringing it up to minus 24.2 points.

The slight recovery was supported by expectations of higher wages, which also increased for the eighth month in a row. „Expectations of significantly higher, collectively agreed income increases are primarily responsible for the more optimistic mood,” GfK expert Rolf Bürkl said of the institute’s consumer survey. However, a strong upturn in consumer sentiment is not on the horizon short-term.

Consumer sentiment remains below the low level of spring 2020 during the first pandemic-related lockdown. Consumers are also more pessimistic about the outlook for the German economy than previously. “It appears that consumers are uncertain about how the German economy will develop in the coming months,” GfK market researchers said. Companies as well are currently expressing skepticism about the next few months. The business climate index calculated by the German ifo Institute in monthly surveys recently fell to 91.7 points from 93.4 points in the previous month.

Bundesbank and finance ministry expect slight growth this year, strong growth in 2024

The German Bundesbank also expects only slight growth in Q2. “In the second quarter of 2023, economic output is likely to increase slightly,” it states in its latest monthly report. Clearing supply bottlenecks, high-order backlogs and lower energy prices should ensure a recovery in the industry. “This should also support exports, especially as the global economy has regained some momentum,” states the German Bundesbank. The German government expects GDP to grow by 0.4 per cent this year. In 2024, a stronger increase of 1.6 per cent is expected.

Retail sales on downward course

In view of the loss of purchasing power and fluctuating energy prices, the experts at the German Federal Ministry of Finance believe that retail sales will continue downwards for the time being.

In March, retail sales recently declined by 1.3 per cent compared to the previous month; adjusted for inflation the drop is as high as 2.4 per cent, according to the Federal Statistical Office – the sharpest decline in five months. Compared to March 2022, the drop is 10.3 percent. “This is the sharpest YoY monthly decline in sales since the start of the time series in 1994,” the statisticians emphasised.

However, the slump may be over soon. “In the further course of the year, a gradual but moderate recovery of activity in the retail sector can generally be expected,” the latest monthly report of the Ministry of Finance states. As soon as a drop in inflation coupled with wage increases and tax relief measures bring real gains in purchasing power again, consumers’ purchasing mood should pick up as well, the ministry’s experts write.

Highest Point of Inflation Has Likely Passed

The German Institute for Economic Research (DIW) and the Munich-based ifo Institute believe that the peak of the inflationary wave in Germany has already passed. The ifo Institute’s barometer for price expectations in the coming three months fell from 21.5 to 19.0 points in May, the German researchers announced last Friday on their monthly business survey.

This would mark the lowest level in more than two years. Economists polled by Reuters news agency expect inflation to drop to 6.5 per cent in May, the lowest level in more than a year.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Eastern Europe: Economies expected to outperform Euro Area

Weakening growth in the eurozone has been an issue on the markets for some time now. In the Central and Eastern European countries, however, this is largely a non-issue. According to forecasts, the region is also likely to grow faster than the eurozone this year. Private consumption in particular has recently proved to be a growth driver. However, the tense situation in German industry is causing concern.

Shift in risks

Both the markets and central banks are pointing to a shift in economic risks from inflation towards growth. The focus is currently on the US labor market.