Eurozone government bonds have ensured very good performance returns in the past years. The asset class has benefited from the zero interest rate policy and the very expansive monetary policy of the European Central Bank.

In recent weeks the prices of bonds from Eurozone countries have gone through a correction, above all German government bonds. The reasons for the specific timing of the correction are numerous and cannot easily be pinned down. In spite of slight improvements, we do not expect an interest rate reversal for the Eurozone at this point in time. The fundamentals for such a scenario are not in place.

Euro government bonds are an important component of a portfolio. From both risk and return considerations, a diversification across a broad spectrum of assets makes sense (e.g. by adding high-yield bonds, emerging markets bonds or equities).

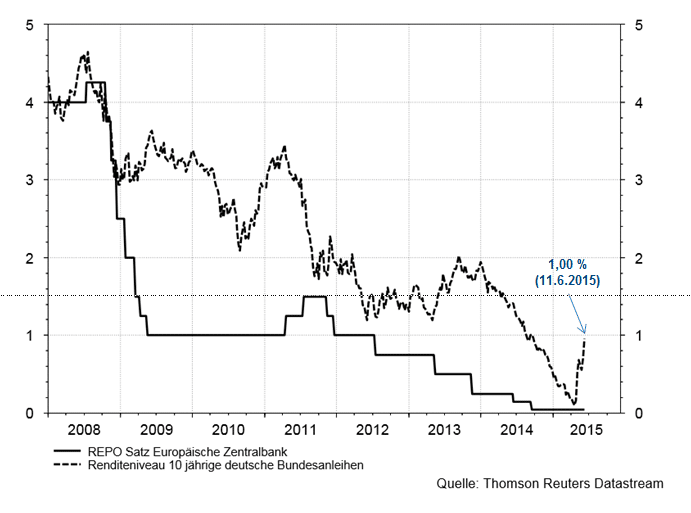

10Y yields of German government bond and key-lending rates Eurozone (2008-06/2015)

Source: Datastream; as of 11 June 2015

The chart does not allow for fees. Past performance is no reliable indicator for future development.

Forecast Erste Group Research

Significant correction of German government bonds

The correction on the government bond markets has been a substantial one. What at first glance seems like a minor increase of the yields of German government bonds from their low on 17 April 2015 at 0.05% to now 0.98% (as of 11 June 2015) did actually come with enormous repercussions on bond prices.

In the past three weeks, euro government bonds have lost the gains made in the first three and a half months of the year and have now entered negative territory (e.g. ESPA BOND COMBIRENT: -1.8% calculated value YTD)

Draghi expects high fluctuations on the bond market.

The monetary policy of the ECB has caused yields to decline drastically in the past months. This is not only due to the zero interest rate policy (in place since September 2014), but also to the purchase programme decided on by the ECB on 22 January 2015, which calls for the purchase of EUR 60bn worth of securities every month. The purchases are to be made until the end of September 2016, and at least until a sustainable correction of inflation has become noticeable. On 9 March the ECB started to buy securities denominated in euro issued by the public sector on the secondary market.

By and large we share the explanations made by Mario Draghi in his latest statement with regard to the recent yield increase in the Eurozone. – Roman Swaton: Senior Fund Manager Fixed Income

These are the declarations made by the ECB:

- Improved growth outlook in Q2 2015

- Higher inflation expectations, or in other words, the deflation scenario was priced out

- New, fundamental valuation from investors which previously were positioned in long maturities

- Strong supply of new issues both in government and corporate bonds

- Steepening yield structure curve of German government bonds, given that the ECB also purchased shorter maturities, which now pay yields of -0.2%, i.e. above the deposit facilities; in the peripherals, the ECB bought an above-average share of long maturities

- Volatility creates new volatility, because the cutting of losses triggers new forced sales

Lower liquidity due to massive purchases by the ECB

A crucial aspect has remained unmentioned: the increase in liquidity of German government bonds, which, globally speaking, are regarded as the second-most liquid bond market behind US Treasuries. – Roman Swaton

The institution of securities lending created by the ECB for bonds bought by the ECB is still under construction. The ECB is therefore not entirely free of blame for the current situation where investors now charge a liquidity premium even for government bonds that were formerly regarded as highly liquid.

Also, the regulatory changes of Basel III have caused the volumes on the trading books in the banking sector to decrease significantly, while at the same time the volume of bonds outstanding has grown further. The share of bonds managed by institutional investors, too, has risen; and according to the most recent global financial markets stability report by the IMF the herding behaviour among institutional investors (especially US funds) has increased, which does not comes as a surprise, given that similar benchmarks and risk systems (i.e. value-at-risk) are being employed.

Get used to higher bond volatility – Mario Draghi, President of the European Central Bank

What role does Greece play?

The impending default of Greece is a potential risk factor for the markets. That being said, Greek government bonds are of secondary importance in relation to the overall euro government bond market.

The EUR 64bn worth of Greek government bonds as illustrated in the following graph account for only slightly above 1% of the market capitalisation of liquid Eurozone government bonds in the investment grade segment. The ECB and other Eurozone central banks hold EUR 27bn of the total EUR 64bn, which means that Greek government bonds held by private-sector investors in terms of total Eurozone government bonds account for only 0.6%.

Roman Swaton cannot explain the yield increase of German government bonds with the unclear outcome of the negotiations of Athens with its creditors. If anything, the so-called flight to quality would have supported German government bonds in the past. Greece might only explain the widening of spreads on the bonds of other peripheral countries.

Market capitalisation Eurozone Government bonds

USA

Market participants expect to see an increase in the Fed funds rate in the USA this year. Recent labour market data have been so good that the first interest rate hike might be implemented as early as September. The assessment with regard to possible increases in the Fed funds rate changes in accordance with the available data, which also further the nervousness of market participants. But one should also bear in mind that any interest steps would be on the smaller side.

Whereas the governors of the Fed expect the Fed funds rate to be raised twice by the end of the year, the market currently only has one hike priced in, which would be equal to an increase of the Fed funds target rate from 0.25% to 0.50%.

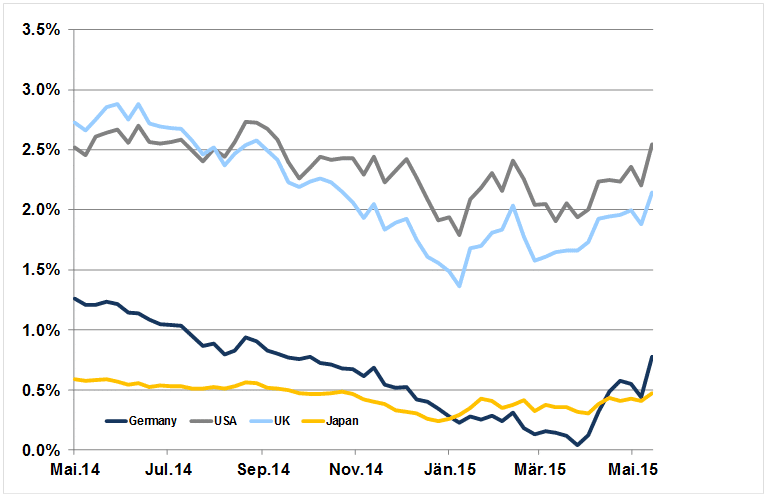

10Y government bond yields by comparison (Germany, USA, UK, Japan)

Source: Datastream; as of 8 June 2015

The chart does not allow for fees. Past performance is no reliable indicator for future development.

Eurozone: economic growth slightly improved

With the exception of the emerging countries, global economies are expected to experience a slight acceleration in growth in Q2. Along with the Eurozone, Japan and the USA have also seen some improvement. China, Brazil, and Russia, on the other hand, have reported weaker economic data. For example, imports slumped by 17% last month. Russia is not expected to record any upswing as long as the conflict with Ukraine has not been settled.

Forecast Erste Group Research

Source: Erste Group Research; as of 10 June 2015

Spectre of possible deflation expelled

The ECB analysts expect to see an inflation rate of 0.3% in 2015, of 1.5% in 2016, and of 1.8% in 2017 in the Eurozone. Market analysts on the other hand expect slightly lower rates of 0.2% in 2015, 1.3% in 2016, and 1.6% in 2017. The inflation swap rate for two years is currently traded at 1.1% (up from 0% at the beginning of the year).

Globally speaking inflation is very low at 1.5%; it might rise to 2.0% by the end of the year due to base effects if the oil price were to remain stable at its current level.

Interest rate reversal or time to invest?

The yield level seems very low in a long-term evaluation, which, however, is in line with the relatively weak economic growth and the low inflation. The fundamentals do not suggest a sustainable bear market in bonds. We do at least in the medium term not expect bond yields to rise on a sustainable basis. The market does not expect the ECB to raise interest rates before 2018. Unfortunately the market participants have to settle in for a longer period of elevated volatility due to the low interest rates and yields.

Why euro government bonds?

Even though yields still seem relatively low, the – from a long-term perspective – higher return vis-à-vis money market investments, the (on average) good rating of Eurozone government bonds (A+), and the, compared with other asset classes, still clearly higher liquidity make a compelling case for an investment in euro government bonds.

The positioning of our fund management team:

a) Euro government bond fund

We are slightly overweighted in the peripherals at the moment. With regard to interest duration, we act very opportunistically, but are currently close to the benchmark. The next targeted longer-term refinancing operations (TLTRO) have been scheduled for the middle of June; they might calm the markets in case of strong demand. – Roman Swaton

b) Asset allocation

Euro government bonds are weighted in accordance with the risk positioning of the investment strategy. Within the bond segment we currently prefer high-yield bonds and corporate bonds from the emerging markets. We are neutral in equities. – Gerhard Beulig

For detailed information about the weighting of euro government bonds in our mixed funds, please refer for example to YOU INVEST.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.