– not only a topic for race drivers")

Have you ever been to the Monte Carlo F! Grand Prix? If so, you may have witnessed the problem of turning into a curve too late. The race car hits the crasher barrier faster than the driver can react, and a lot of money has to be thrown at the repair job.

So, what does a car race have to do with financial markets? The bond markets show similar performance criteria. If you are positioned at the wrong end of the yield curve, it may cost you a lot of money.

Germany has the yield curve with the best rating

The yield curve, or more precisely, yield structure curve, shows the yield with reference to the remaining time to maturity. Usually, the longer the money is tied up, the higher the yield is (longer remaining time to maturity = higher risk = higher yield). Let’s have a look at the current yield curve for European benchmark bonds (German government bond).

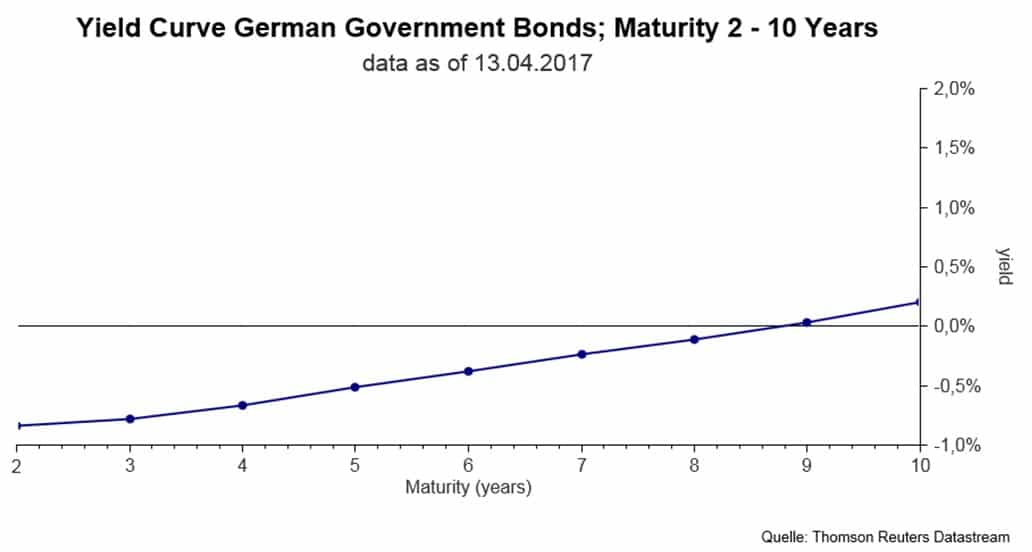

The chart illustrates the German yield curve as of 4 April 2017 for a remaining time to maturity of two to ten years:

Chart: Yield structure curve for German government bonds 2Y to 10Y

Sources: Datastream, as of 4 April 2017

The chart also contains the zero percent line. Curve-sketching involves a number of aspects. We shall start with the objective criteria “location of the curve” and “yield in percent”

- Slope of the curve: the yield of short remaining time to maturity is significantly below that of the yield of long remaining time to maturity. In this case, the yield curve is referred to as steep (which, historically, is the normal state of affairs; it is therefore also called the “normal yield curve”).

- Location of the yield curve: the yield in percent, i.e. the absolute height of the curve, is more interesting. In view of the delineated zero-percent line, it is easy to see that up to a remaining time to maturity of 8Y, bond yields are negative. The yield only switches into positive terrain from 9Y onwards (albeit at low levels).

We can now take the next step and ask ourselves what this means for potential investors:

- Nominally speaking, German government bond yields are negative or at least very low (at long maturities). Taking into consideration fees at the time of purchase and for the depositary account during the life of the bond, this investment is not particularly attractive in terms of return rates.

- The adjustment for expected inflation yields the “real rate of return”, which is even less attractive for this investment.

Why yields are currently so low and the prices of these bonds are so high

High prices manifest high demand. But who buys such bonds? Buyers are mainly institutions and institutional investors who (have to) invest in these bonds for various reasons such as:

- The European Central Bank within the framework of the bond purchase programme

- Insurance companies and pension funds

- Banks for their own account

- Investment funds due to the fund terms and conditions

We would like to use an example to show what such an investment means for a retail investors.

The aforementioned yield curve depicts the yield of actual bonds. For this example, we have chosen a bond with 2Y of remaining time to maturity. Specifically, this is the 0.00% Bundesrepublik Deutschland 2017-19 (ISIN: DE0001104677) bond.

Bond profile:

- Launch date: 2 March 2017, issue price 101.89 %

- End of maturity: 14 March 2019, redemption price 100.00 %

A negative yield means: investors who have paid EUR 101,890 at issue will not be receiving any interest for two years and at the end only get EUR 100,000 back. This means that an investment in this bond clearly results in a certain loss of capital!

What this means for our investors

An investment where it is clear in advance that capital will be lost cannot be called a good investment opportunity. Investments in euro government bonds with top to high ratings are not particularly attractive. This also applies to investment funds that invest in such bonds. Investors should therefore look for alternative investments. Going back to the F1 Grand Prix in Monaco: it is time for a pit stop and a change of tyres.

Conclusion:

As the example of the German government bonds shows, euro government bonds with very good to good ratings are currently very expensive. This translates into the yield level, which in some cases is even negative. And a negative yield means that investors know in advance that they will get back less money than they paid in.

There are also investments with attractive yields. However, they come with a certain degree of risk – because without risk it will be impossible to achieve a positive performance in the coming years, both nominally and even more so in real terms.

For risky investments, broad diversification is key, much like investment funds offer it.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.