The People’s Republic of China is one of the winners of globalisation. Since joining the World Trade Organisation (WTO) in 2001, the country has recorded rapid growth, moving up to second rank behind the USA in terms of economic output. And it will probably pass the US economy in the coming years with respect to GDP.

The struggle for global hegemony between the USA and China has become more intense, as reflected by the trade conflict, which has been heating up. However, the strong economic growth has also created asymmetries within the Chinese economy. Beijing tries to generate sustainable and balanced growth and face the challenges of the trade conflict with the USA on the back of a package containing several initiatives.

Growth has led to asymmetries in China

The growing heap of debt, overcapacities in traditional areas such as coal, steel, and cement, and environmental pollution have affected expansion. The country is therefore trying to overcome those challenges through numerous measures and to create new growth opportunities. In order to keep economic growth relatively stable, the government has already loosened the budget policy and suspended the planned slashing of debt. Additional infrastructure projects are supposed to set off new momentum. In particular, Beijing tries has launched three strategic initiatives to make the economy more balanced, more innovative, and more competitive and to further the country’s progress towards the global technological and industrial elite. These are the three central geo-economic initiatives:

- The “One Belt, One Road” initiative (OBOR, also known as “Silk Road”) aims at developing and expanding the markets along strategic trade routes;

- “Internet Plus”, and

- “Made in China 2025” are meant to push the Chinese industry to new levels and support the manufacturing and e-commerce sector.

Closing the gap to international standards in terms of material consumption and emissions by 2035

The “Made in China 2025“ strategy – presented in the 13th five-year plan – lays down China’s goal of restructuring its industry entirely and thus moving up to the league of top players in the industrial sector around the world. The ultimate, clear goal is to challenge the technological leadership currently held by the USA. The plan is to massively stimulate innovation and product quality. The improvement of production technology is one means to this end. Plans are also to optimise the structure of the industry and to close the gap to international standards in energy, material consumption, and emissions in the production process by 2035.

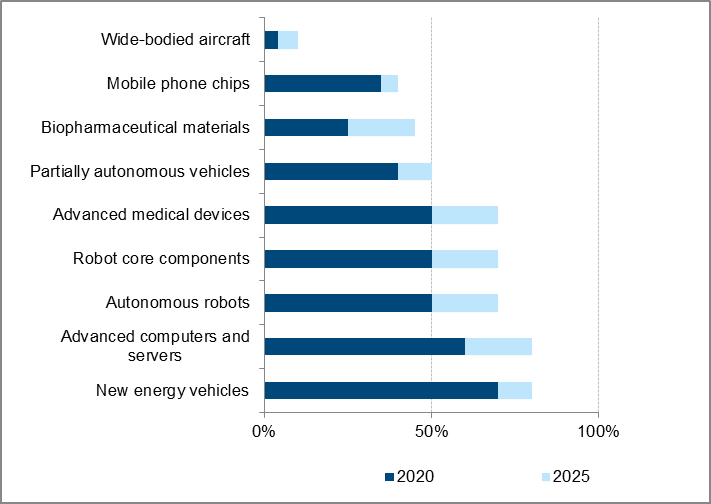

By boosting efficiency and integrity, Chinese services and production are supposed to advance to the highest echelons of the global supply chain. The country plans to increase the local value-added of key components and material from 40% in 2020 to 70% in 2025.

This means it is China’s goal to produce more and more high-quality parts “in-house” and to cut down on buying from outside sources: “Made in China” as quality seal. The strategy emphasises ten priority areas that the country will be focusing on: new, cutting-edge IT, numeric high-end machinery and robotics, aerospace technology, marine engineering, high-tech shipbuilding, modern railway technology, energy-saving vehicles and electromobility, electrical equipment, agricultural machinery, new materials, and biopharmaceutical products and medical devices.

Priority areas – Made in China 2025

Sources: Erste AM, Chinese Academy of Engineering, U.S.-China Economic and Security Commission

A very ambitious goal that will be difficult to reach within the targeted period (2025) without foreign know-how and capital. This means that the tariffs imposed by the US government are aimed exactly at these Chinese priority areas, trying to impede or at least delay the rapid development of China toward no.1 economic superpower. Accusations of the theft of intellectual property are part of that scheme.

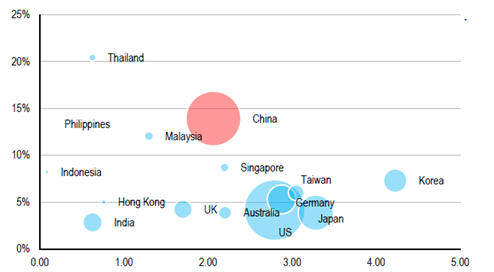

With its 2017 budget of EUR 226bn, China recorded the second-biggest volume of R&D expenses in the world behind the USA, which means it had quintupled since 2005. Adjusted by purchase power, (in PPP), China has already surpassed the USA in 2018.

R&D spending in % of GDP and 5Y growth rates

Source: Erste AM, Chinese Academy of Engineering, U.S.-China Economic and Security Commission

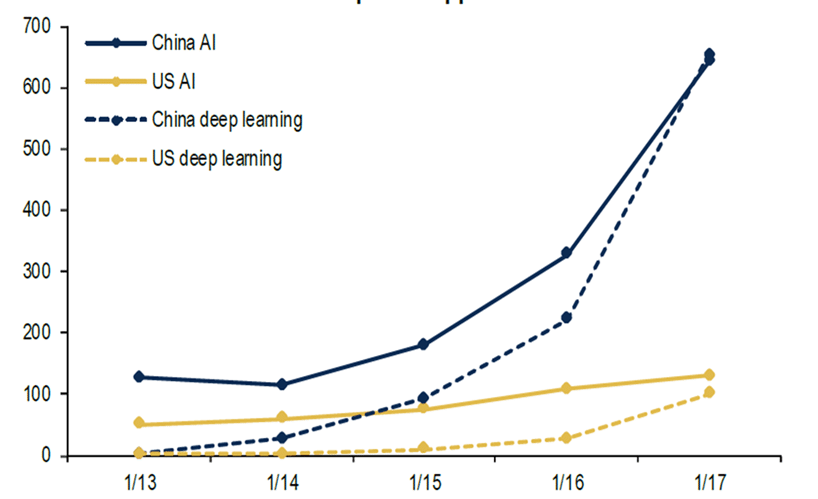

A quarter of all start-ups above USD 1bn are being founded in China. The country has already caught up with its competitors in patents (see chart below) and has thus illustrated its innovative prowess. The current market environment in China promotes research and development in particular. In addition to tax deductibility, the Chinese education system is beneficial to this angle as well: every year, it produces three million graduates in the areas of science and technology – five times more than in the USA, but at wages an eighth of those in the USA. One also has to bear in mind the more flexible and easier introduction of products as well as test phases as far as statutory requirements are concerned. All of that is very supportive to the innovative prowess of the country.

Megatrend Artificial Intelligence (AI)-related patents

Sources: Erste AM, UBS

Development leaps through take-overs in Germany and Austria

At the same time, Beijing has upped its efforts to ensure development leaps in the core areas through take-overs and strategic investments. The Chinese producer of white goods, Midea, hopes to generate strategic benefits by acquiring the German robot manufacturer Kuka. Kuka, in turns, hopes to use the alliance to open a door onto the world’s largest market for automation.

This example shows that Chinese partners can open doors when it comes to tapping new markets, while they get access to technological know-how. In the aerospace industry, the government-held Chinese arms manufacturer and aviation group AVIC took a majority investment in the Upper Austrian aviation supplier FACC several years ago. The company focuses on the processing of plastics and develops and produces aeroplane interior equipment for manufacturers like Boeing, Airbus, and Embraer. The positive development in civil aviation with an annual growth rate of 5% – with the Asian region recording above-average rates – has already led the company to move part of its production to China. The trade conflict between the USA and China should not really affect FACC, given that the trade barriers will mainly focus on military goods.

In the automotive sector, too, Chinese players have been busy setting up strategic alliances. The investment of the Chinese car manufacturer Geely in the German automotive group Daimler came as a surprise to many earlier this year. That being said, Geely had previously already pushed its expansion through acquisitions of the Volvo passenger car segment, the US producer of flying cars, Terrafugia, or the English London Taxi Company, thus securing itself leaps in innovation.

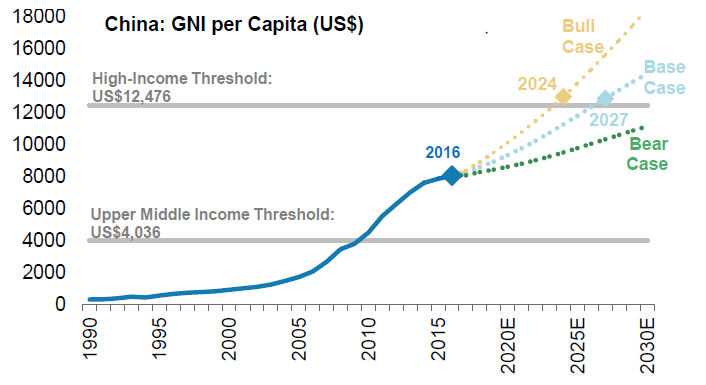

China: GDP per capita

The rolls of the markets and the regions along the value chain will be changing alongside the rapid development of the Chinese economy. Strategic alliances with Chinese companies and their production is gradually replacing the image of a source of suppliers from cheap-labour countries. Many countries see this fact as opportunity and threat at the same time. Relationships could be established on a level playing field if China were to do away with some of its protectionism.

Alibaba, Baidu, and Tencent turning China into internet giant

The strategy “Internet Plus” complements the restructuring goal. It is supposed to integrate internet technologies such as mobile internet, cloud computing, big data, and internet of things into traditional industries so as to improve the flow of information and efficiency and minimise costs.

At the same time, China supports start-ups, e-commerce companies and fintechs. We expect to see a wave of new enterprises being set up, given that the young population is increasingly drawn to the attraction and the quick success of such start-ups. The strategy aims at changing entire business segments and integrating the rural areas of the country into the economy transforming them.

Successful internet giants such as Alibaba Group, Tencent Holding, and Baidu, which are not state-held, are regarded as archetypical models. However, the Chinese state levies its protectionism to keep control over private internet use, because foreign web platforms such as Google, Facebook, and Amazon are still not permitted.

Market with more than 4bn people: One Belt, One Road to sort it out

The third Chinese initiative, i.e. the “One Belt, One Road” strategy, which the Chinese President Xi Jinping presented in 2014, is based on the idea of combining a land-borne economic belt, i.e. an overland Silk Road (an economic corridor along the Eurasian continent all the way to Western Europe), with a maritime Silk Road of the 21st century (a network of maritime trade routes, that connect Asia with Africa and Europe).

According to the Chinese government, a total of 65 countries around the globe have so far indicated interest in cooperating, which would create a potential market of 4.4bn people. This way, China tries to pursue its strategy of safeguarding its geo-economic interest such as bigger influence on global trade, reduce overcapacities, and build economic activity and infrastructure in Western China. Investments in the Eurasian region such as Afghanistan or Pakistan would promote economic growth and political stability in that region and curtail economic migration.

Thus, the Chinese government addresses a combination of external and internal risk factors with its strategic package that could compromise the resilience of the Chinese economy in the short run. If Beijing reduces its economic protectionism and opens up to strategic alliances on a level playing field, even the US sanctions would not be able to prevent the country from developing into the world’s no.1 economic superpower.

Disclaimer:

Forecasts are not a reliable indicator for future developments.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Strong US labor market report: just an outlier?

In September, the US labor market performed surprisingly well, with significantly more new jobs created than expected. This has pushed back concerns about an impending recession, which is positive for the financial markets. Was the strong labor market report just an outlier, or is the US Federal Reserve perhaps on the right track to achieving the hoped-for “soft landing”?