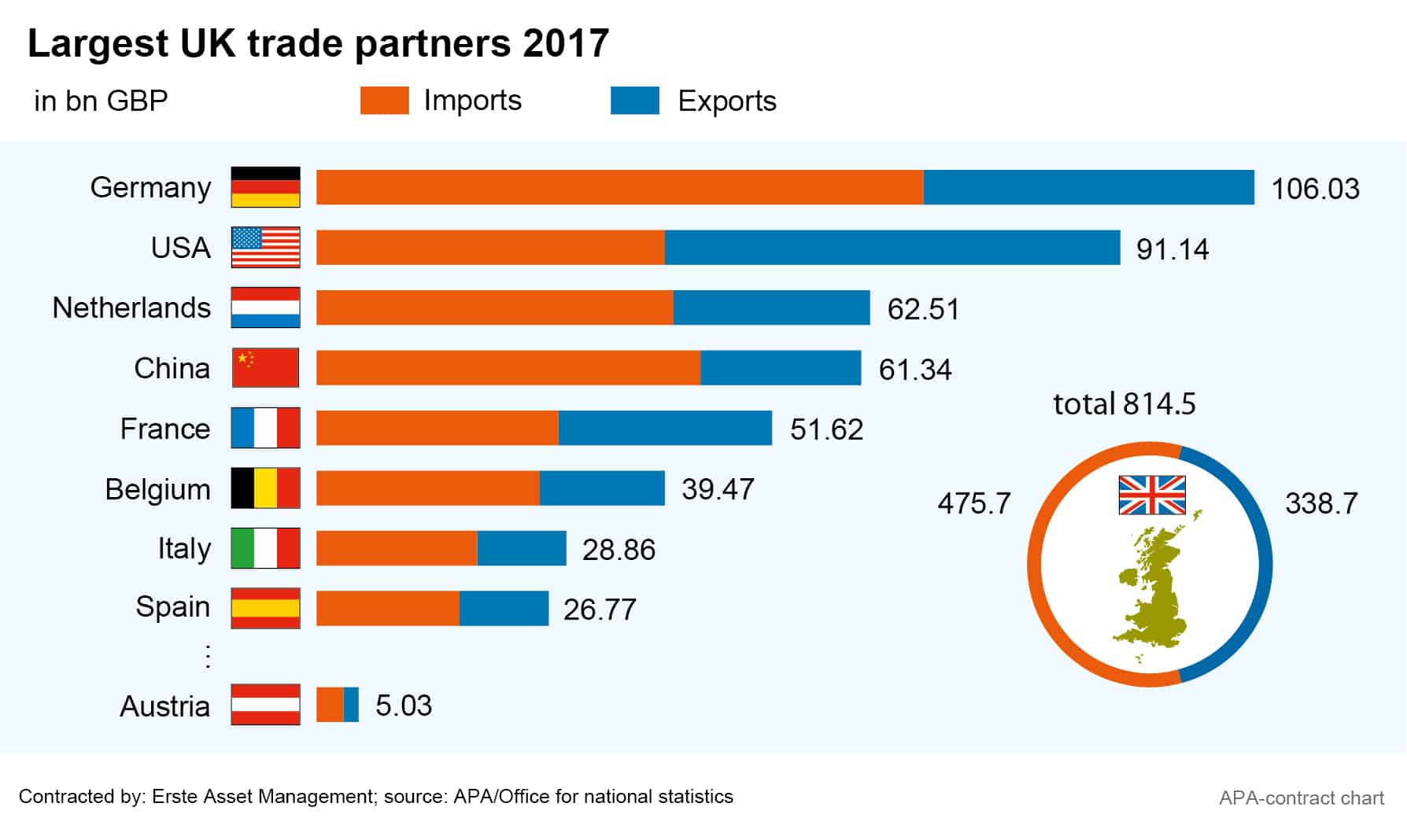

Last week, British Prime Minister Theresa May called on members of London’s parliament to “hold their nerves”: As of 29 March, Great Britain will no longer be part of the European Union. However, as the UK Parliament has now once more rejected May’s Brexit deal in a vote on Thursday, it is still not clear what relations between the former Empire and the EU will look like in the future.

Economic data recently provided a glimpse of the Brexit consequences. Gross domestic product (GDP) rose by only 0.2 per cent between October and December 2018 compared to the previous quarter (Source:Nationales Statistikamt (ONS), 11.Februar 2019). In December, production by British companies declined for the fifth consecutive month, with carmakers and the steel industry in particular cutting back production. As the Brexit approaches, experts see the uncertainty businesses are feeling increasing reflected in the investment mood. Even in the event of a compromise there would be a noticeable slowdown over the course of the year.

The magnitude of businesses’ uncertainty is already very much evident: instead of manufacturing the next generation of its SUV model X-Trail for the European market in England as planned, Japanese car manufacturer Nissan will manufacture the model in Japan. Ford is also making arrangements for moving its production from the UK. Aviation and arms corporation Airbus is threatening to shut down factories in the UK in the event of an unregulated EU withdrawal.

“Deal”, or “No Deal”?

Without a proper Brexit treaty the British would suddenly be subject to World Trade Organisation (WTO) rules only. A recent study by the Salzburg Centre of European Studies shows (Source: „Brexit: Folgen für Österreich und die EU“,6. Februar 2019), that a Hard Brexit would not only harm the UK as a business location, but would also result in an estimated immediate drop in the UK industry’s production of up to 7.6 percentage points compared with the previous year. As a result, production in the Austrian industrial sector could decrease by up to 4.5 percentage points, while Germany could suffer a 4.2 percentage point decline. The estimates for France and Italy are even worse.

A study by the Halle Institute for Economic Research (IWH) and the Martin Luther University of Halle-Wittenberg concludes that 612,000 jobs globally would be at risk after an unregulated Brexit: “In Austria, 2,000 jobs could be affected directly, and 4,000 jobs indirectly,” says study author Oliver Holtemöller. The study assumes that Britain’s imports would decline by 25 per cent as a result of an unregulated EU withdrawal.

© APA

With the – for now – once again rejected Brexit agreement, little would change economically until the end of 2020. The British would have to continue to comply with EU law, but no longer participate, explains Stefan Griller, Professor of European Law at the University of Salzburg. According to the university’s projections, this scenario would have a much smaller impact on industrial production in the UK and EU countries.

Conservatives, however, are particularly opposed to the border regulation between Northern Ireland and Ireland laid out in May’s deal. The EU does not want border controls between Northern Ireland and Ireland. The British, on the other hand, do not want border controls between the British mainland and Northern Ireland. A supplementary agreement to the Brexit treaty could at least partially mitigate this issue. But in order to negotiate such an agreement, Theresa May not only needs her members to “keep calm”, she also requires more time and the members to support her work. However, this the UK MPs clearly refused in the vote on Thursday. Furthermore, the PM also lost support among her own party again, which not only weakens her negotiating position in Brussels, but ultimately also makes a regulated and thus smoother Brexit less likely than ever.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.