Both equity and bond markets managed to carry the momentum of the good start into 2023 to the second trading week of this year. The broad US equity market gained about 2.6%, the European market about 2%. Due to the fall in yields on the bond markets – 10Y US Treasury bonds are traded at a yield of around 3.5% *) – the technology sector and, especially in Europe, the real estate sector outperformed the overall market.

Additional rate increases necessary

The positive factors clearly prevailed last week. For the time being, we can see a good combination of the labour market remaining in good shape and wage pressures rising less significantly. Therefore, the probability of second-round effects on inflation has declined. It is important to bear in mind the level of wage increases, which will make further interest rate increases necessary.

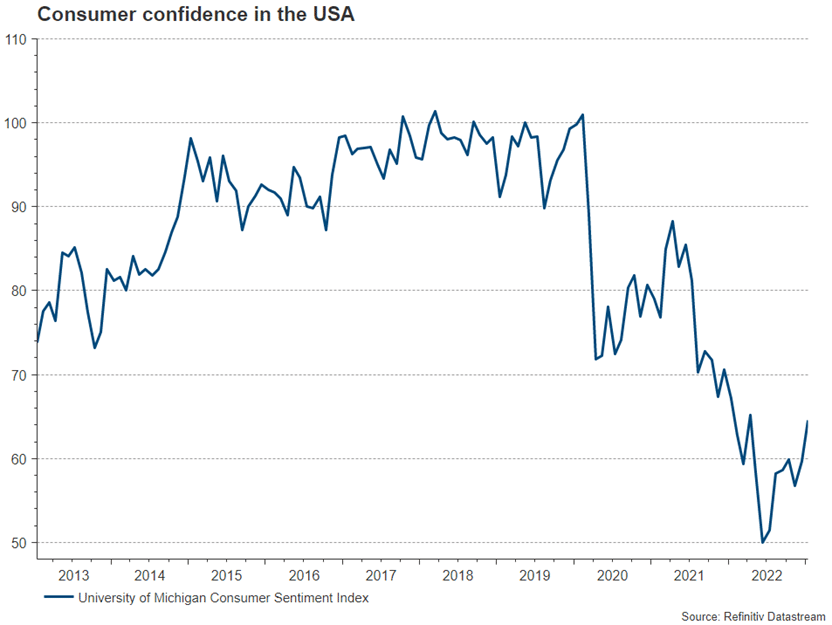

Consumer confidence in the USA on the increase

The US inflation rates were published last week exactly to the decimal point, as predicted. Headline inflation over the last twelve months was 6.5%, the core rate excluding the volatile energy and food components was 5.7%. A bigger surprise was delivered by the University of Michigan’s consumer confidence index: consumer sentiment, which had been trending downwards since the outbreak of the Corona pandemic mainly on the back of rising prices, came as a significantly positive surprise relative to estimates.

Note: Past performance is not a reliable indicator of future performance.

The important 12M forward estimate of inflation also fell to now 4.0%. One of the main goals of central banks is to contain inflation expectations.

The risk of recession is on the decline

In Europe, the steadily falling gas price helped to dampen inflation expectations a little. The renewed rise in crude oil and industrial metals, but also in the price of gold, illustrate that the price trend for commodities and precious metals remains volatile. The opening of China from the Covid restrictions has raised expectations of rising demand for these commodities and has overall contributed to a more positive assessment of the global economy. Numerous analysts are in the process of revising their forecasts, now assuming a lower probability of recession for the USA and especially for Europe.

European equity allocation increased in the Erste AM funds

In our mixed funds and asset management portfolios, we have left the equity portion at a neutral level. While the positive factors on the inflation side are boosting the markets, the possibly more negative factors affecting the economy and corporate results are still pending. In the equity segment, we took advantage of the positive momentum and the more favourable valuation of continental European equity markets and increased the allocation. We like small cap companies (i.e. companies with a stock market value in the two to three-digit million range). At the same time, we reduced the weightings of Japan and the USA. In Japan we can currently see an interesting change in central bank policy. The successor of the outgoing central bank governor, Haruhiko Kuroda, could once again bring the interest rate policy back into a somewhat less expansive range.

*) Source: Erste AM, 16 January 2023

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Please note that an investment in securities also entails risks in addition to the opportunities described.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

to the White House")

Best of Charts: The road (in)to the White House

Three weeks before election day, the race for the White House is wide open: While Kamala Harris is ahead in the nationwide polls, Donald Trump is currently likely to be ahead in the crucial “swing states”. In any case, the economic situation and mood in the USA are likely to play an important role in the race for the presidency.