Donald Trump is getting serious and imposing temporary tariffs on his major trading partners. He is also escalating the war in Ukraine and increasing the pressure on Europe, which will hopefully soon be galvanized into unity with a new German Bundestag.

Anyone who thought that Donald Trump was craving disproportionate attention only in the first few days of his new term will have found themselves sadly mistaken in February. The Republican US President remains “on fire” and is unsettling a broad front. In contrast to the many symbolic political announcements in January, the latest escalations are disruptive in nature and definitely come with a negative impact on the economy.

It wasn’t a bluff after all!

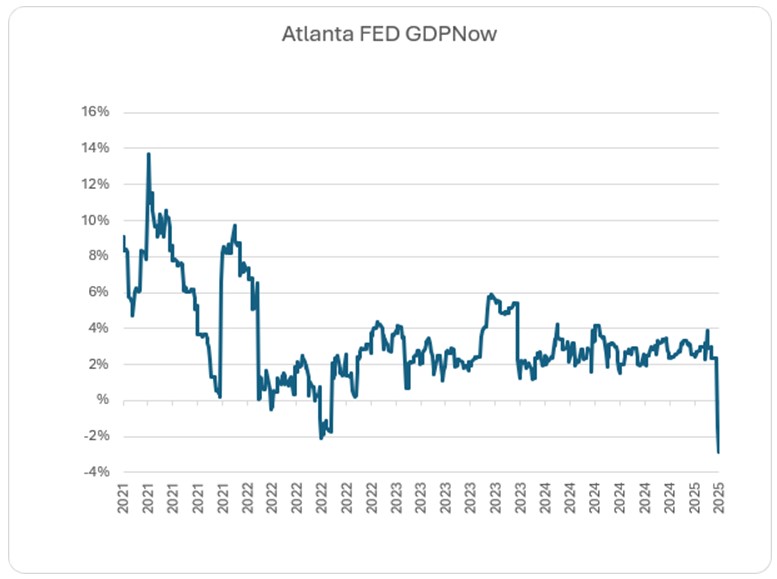

First and foremost, we should like to mention the tariffs that have now actually been imposed on Mexico and Canada. With a 25% tariff on almost all imports from the direct neighboring countries, as well as the additional levies on Chinese imports, which have been increased to 20%, more than 40% of total US imports are affected. The negative effect on the economy and inflation should have dawned on him just two days later and so the levies for the direct neighboring countries are off the table again. However, this does not mean that the issue of tariffs and thus a possible trade war are off the table, as he has recently also targeted the EU and agricultural imports. The US economy continues to grow robustly, but in recent weeks some sentiment and economic indicators have surprised on the downside. For example, the much-heeded Atlanta FED GDPNow index – which estimates US economic growth in the current quarter on a weekly basis – recently fell by a surprisingly sharp degree into negative territory.

While one should not attach too much importance to individual indicators, the growth risks have definitely increased. Past performance is not a reliable indicator of future performance.

Source: LSEG Datastream; Data as of 5.3.2025

Europe’s (forced) comeback

Not only the tariffs, but the escalation surrounding the Ukraine conflict was also a turning point. The public exchange of blows in the Oval Office and, in particular, the cancellation of American military aid are putting pressure on Ukraine and, with it, the whole of Europe. It will be all the more important for Germany to have a new federal government and a new chancellor very soon after the general election, in contrast to Austria. In view of the ongoing changes, an agreement between Paris, Berlin, and Brussels would probably be more important now than it has been for decades. After all, the designated Chancellor Friedrich Merz is not afraid of thinking big – the arms and investment package of up to EUR 1.5 trillion, announced before the start of the coalition negotiations, is surprising. The EU Commission seems to be making a U-turn as well, having recently attracted attention with deregulation measures in the automotive industry. Perhaps Donald Trump will not only make America great again, but also Europe, albeit indirectly. On the trading floor, Europe has already made a successful comeback. While European equity indices are up almost 10% in the year to date, their American counterparts have recently even slipped into negative territory. The trend could continue, but in the long term, US earnings momentum still seems more advantageous. Regardless of the exact regional positioning, the past few weeks have shown that diversification in the portfolio context remains the order of the day.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Best of Charts: What’s coming, what’s going, what’s staying from 2024?

We can look back on an eventful year on the markets – although 2025 is also off to a somewhat turbulent start (at least in terms of domestic politics). In our first ‘Best of Charts’ of the new year, we look at what will remain of the stock market year 2024 and what we can expect in the coming months.

The first 100 days

The first 100 days of Donald Trump’s second presidency are behind us. What has happened since then? Will the structural changes continue at this pace?