Péter Varga, Senior Professional Fund Manager, is of the opinion that the interest rate increases announced by the central banks will come with several unwanted side effects. In this interview, he explains the reasons for his scepticism.

What is the driver of the high inflation that we are currently seeing?

Inflation always occurs when demand is bigger than supply. Due to the production backlog caused by Covid, almost all companies are working at capacity, and yet they fail to satisfy demand as a result of a lack in machinery, commodities, or parts. The latter two, in particular, are currently causing issues for numerous companies. The causes are rooted both in the pandemic and in the war against Ukraine.

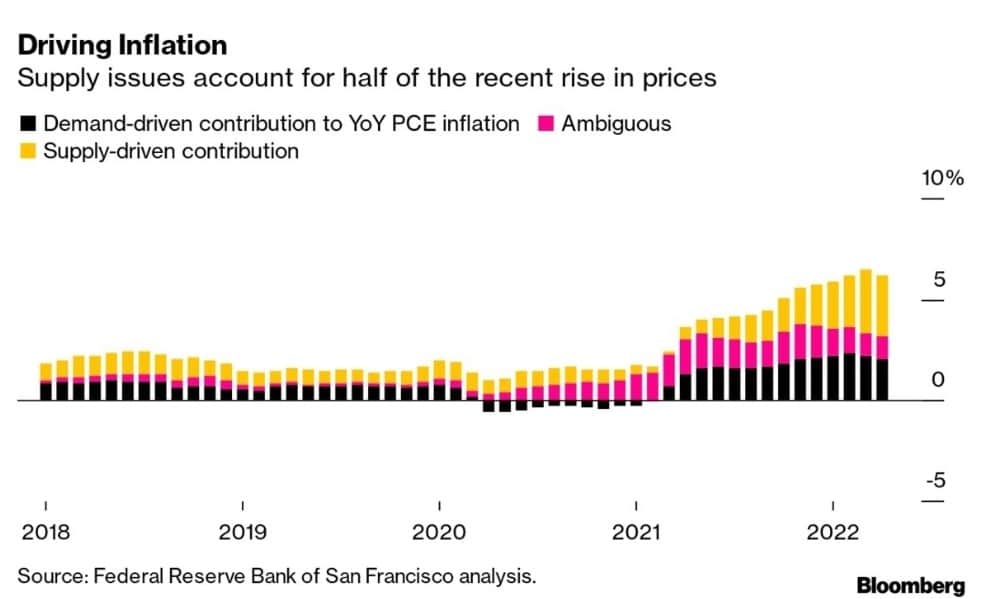

According to Federal Reserve Bank of San Franciso more than 50% of US-Inflation (PCE deflator) can be attributed to supply-driven and ambiguous facts.

What can the central banks do?

Neither the fight against the pandemic nor the termination of the war are ultimately up to the central banks. As a result, we will remain subject to high energy prices, which are a main driver of inflation. The central banks cannot pull more grain or fertiliser out of a hat by printing money. The only lever they have is to correct demand downwards. For this reason, they increase the purchase cost of goods and services.

How can this work?

Central banks can try to make this work by stepping up the interest rates on loans and inducing a higher propensity to save among consumers. This calms demand and reduces the price increase.

What effect does this scenario have on consumers?

The consumers feel it twice: first, their loan instalments (if they have a loan with variable rates) increase. And second, they feel it because of the rising prices for goods and services. The result is a significant loss in purchase power and a cash flow problem.

„The consumers feel it twice: first, their loan instalments and second, they feel it because of the rising prices for goods and services.“

Péter Varga, Senior Professional Fund Manager Erste AM

© Photo: Stephan Huger

What does this mean specifically?

If the wage increases fail to thwart these effects noticeably, more and more debtors will find it hard to pay their instalments in a timely fashion. Consumption will also suffer (with the inflation-adjusted value of our wages falling). Companies are facing a similar situation; they will be in trouble if they cannot increase their prices, and they will have to expect a decrease in demand.

In summary: what future scenario do you expect?

This is hard to answer. From my point of view, there are various aspects that will influence the future.

Wage increases: since the labour market is tight, we might see significant wage increases. This does not automatically have to lead to falling demand; in other words, we will be living with inflation and high nominal yields in the long run. The so-called wage/price spiral will advance further. Without wage increases and interest rate hikes by the central banks, the high inflation would push down purchase power noticeably.

Interest rate increases: in order to fight inflation, some central banks have already increased their interest rates or taken preparations to do so in due course. The effects do not only affect debtors, but also investors: the correction suggests falling asset prices, e.g. for equities that end up in a bear market. Or for real estate, which records falling demand as it has become unaffordable due to purchase power losses and an increase in the interest rates on loans. Consumers feel less wealthy and accordingly reduce their consumption.

Ukraine war: if the war ends and the commodity supplies pick up again, we can expect a much more relaxed situation. This situation clearly highlights the fact that in a world with cross-continental supply chains and optimised production processes, it is impossible to pursue imperialistic policies without significant consequences for the global economy.

This means that geopolitics will decide the fate of the global economy?

That’s right. This is why I want to appeal to all influential politicians: the fight against inflation is largely in your hands, and not in those of the central banks!

For a glossary of technical terms, please visit this link: Fund Glossary (erste-am.at)

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Turkish financial markets temporarily under pressure following political turbulence

The Turkish stock market has been turbulent recently: the arrest of Istanbul mayor Ekrem Imamoglu caused massive uncertainty. What does the political unrest mean for the Turkish economy and the Istanbul stock exchange?