Technology shares have outperformed all other sectors in the past ten years. After a strong correction, the market has rebounded. How does Bernhard Ruttenstorfer, Senior Fund Manager of ESPA STOCK TECHNO, see the future of technology shares?

The correction around the middle of October did not really surprise you?

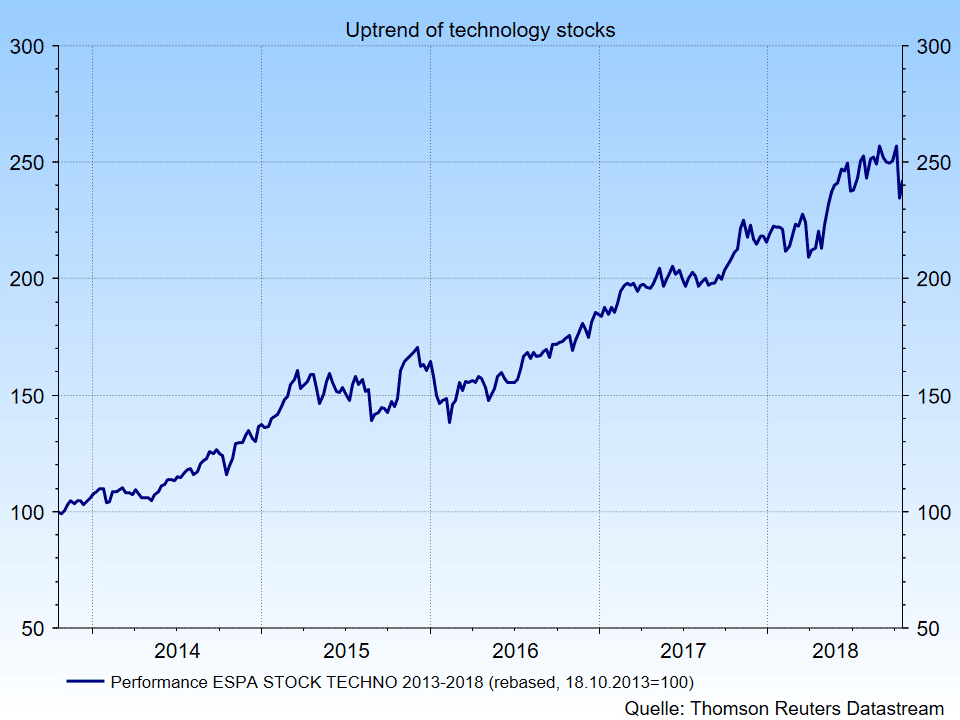

That’s right, technology share prices had been on a significant upward trend since 2008. Of course, it had been interrupted a few times, which is also healthy, but such breaks would never last long. Generally, growth shares currently command high valuations relative to value shares, and there are good reasons for that. We can still see rising sales and profits for technology companies. Many business areas are not yet developed, many innovations have not yet matured.

Disclaimer: Forecasts are not a reliable indicator for future developments.

So, everything “A-ok” then with technology shares?

Of course, there are stumbling blocks that the market and the companies do not foresee. For example, let’s look at social media: Facebook has recently had problems in the area of data protection, having passed on user data to the company Cambridge Analytica. Politicians now want to up their game in terms of regulation. They want to contain the dissemination of fake news. This means that laws could come into effect that would curtail social media. Stricter regulation could cut sales and boost costs. In Europe, we have received the first taster in the shape of the General Data Protection Regulation (GDPR).

What product trends and innovations will be the future drivers of the technology sector?

Bernhard Ruttenstorfer, ESPA STOCK TECHNO: “Facebook and Twitter are not going to dissolve into thin air”

Generally speaking, we can see broad demand across numerous sectors. The technology companies do not only target “normal” customers but also industrial clients. In the car sector, the IT share is constantly on the rise. Some manufacturers are currently testing safety assistance systems and autonomous driving systems. Communication in the car is becoming more and more important, e.g. through digital displays. Electromobility, too, requires more IT in the car. In industrial production, the field of robotics is becoming more relevant. This concerns the establishment of links between factories so as to facilitate faster and more flexible production. In manufacturing, robot-operated production lines are being modernised. Mercedes manufactures an electric version on the normal production line. Here, supplies and every move have to work in real time. In the field of medical engineering, we will soon see hearing aids with integrated live simultaneous interpretation. They contain a lot of technology due to the required IT link, powerful processors, and strong batteries. All of that has to be compact and light.

What is the situation on the smartphone market?

Smartphones are not the big money-spinners anymore, but we remain very keen on social media. Some titles like Facebook and Twitter have been punished by the market for being late to certain trends. This was also confirmed by low sales growth in their latest quarterly figures. However, these providers will not be dissolving into thin air. The question is: is there a new provider who can call out the established services? If that is so, Facebook could for example just buy it, as we have seen in the cases of Instagram and WhatsApp. While these were expensive deals, it was the right decision.

Let’s talk about ESPA STOCK TECHNO. How is the fund positioned in the current environment? What shares are you betting on?

ESPA STOCK TECHNO invests in the most important technology companies worldwide. The USA dominates the field. At the moment, we are overweight in the manufacturers of semi-conductors. Hardware and storage space producers are underweighted relative to the technology index. We are also pursuing the odd single-title bet. For example, we hold the biggest overweight in Nvidia, the market leader in Artificial Intelligence. Autonomous driving, e-gaming, and artificial intelligence at data centres are also interesting themes for the fund. The software vendor Workday has developed HR software that operates fully on cloud-basis. We can also see strong growth potential in Electronic Arts und Activision Blizzard in the live-streaming of e-gaming tournaments. In Europe, our Villach-based “local hero” Infineon has been driving the development of the Internet of Things, industrial and robotic communication, and energy management. ESPA STOCK TECHNO covers all these themes and companies.

What is the earnings outlook for technology companies?

The consensus estimates by analysts forecast aggregate earnings growth of 20% for 2018 and 2019. In 2020, earnings are expected to rise by 10%. All of that amid double-digit sales growth. This means the outlook is good. Set-backs of share prices, the likes of which we saw around the middle of October, have to be considered when taking investment decisions.

The interview with Bernhard Ruttenstorfer was conducted by Dieter Kerschbaum.

Overview ESPA STOCK TECHNO

Advantages for the investor

- Participation in the most important global high-tech companies.

- Opportunity to achieve substantial capital appreciation.

- Broad diversification in global technology companies.

Risks to be considered

- The net asset value of the fund can fluctuate considerably (high volatility)

- Due to investments denominated in foreign currencies, the net asset value of the fund in euros can be negatively impacted by currency fluctuations

- The investor bears the risk of the global high-tech sector and the issuer risk of the participating companies

- Capital loss possible

Risk notes according to 2011 Austrian Investment Fund Act

ESPA STOCK TECHNO may exhibit increased volatility due to the composition of its portfolio: i.e. the unit value can be subject to significant fluctuations both upwards and downwards within short periods of time.

Disclaimer:

Forecasts are not a reliable indicator for future developments.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

The Tariff Man

Last Sunday, the US government announced new tariffs on goods from Canada, Mexico and China, only to suspend them again shortly afterwards. How might the trade conflict develop? Is the EU also threatened with new tariffs?

What effects could DeepSeek have on the technology sector?

The new AI model from Chinese start-up DeepSeek caused a stir on the stock market a fortnight ago. The seemingly much more efficient and therefore cheaper model caused the share prices of many a tech heavyweight to plummet. Although the initial market reactions were probably exaggerated, one question remains: what long-term impact will DeepSeek have on the big tech companies?

Semiconductor Industry: Between AI Boom and US Tariffs

The semiconductor industry is considered one of the biggest beneficiaries of the AI boom. Investors therefore kept a close eye on the sector’s figures for the first three months of 2025. One thing became clear: the expansion of AI infrastructure continues to deliver good results for most chip companies – but the sword of Damocles in the form of impending US tariffs is still hanging over industry giants such as Nvidia & Co. Read more in today’s blog post.