Making sense of it all

I will be upfront about it: to me, the Taylor rule is still a helpful tool to assess the future monetary policy of the US central bank. However, it should not be used as blueprint without thinking it through. Instead, it should be seen as heuristic tool that helps structure one’s analysis.

In order to create an idea as to the “right” interest rate according to the Taylor rule, I want to set up a bandwidth of the Taylor interest rate. After that, I am going to offer my personal opinion and assessment and draw a few conclusions with regard to the future development of the monetary policy.

The input variables are the nominal, neutral interest rate (bandwidth of 2% to 5%); the inflation gap (currently -0.6 percentage points), which is the result of the US central bank’s inflation target of 2% and the current value of the CPCE deflator of 1.4%; and the output gap (-0.8% to 1.1%). This results in a Taylor interest rate of 1.3% to 5.25%.

Taylor interest rate estimate

Source: EAM

This, to me, leads to two findings:

- The large bandwidth of results is mainly due to the uncertainty about the actual level of the neutral rate. It is even more difficult to determine than the output gap, which also defies observation, and in many instances, is a case of believing rather than knowing. To me this means that one has to look very closely as to who the decision-makers are or will be at the Fed.

- The lower end of the bandwidth of the estimates above suggests a key-lending rate of 1.3%. This value is slightly above the current bandwidth for the Fed funds target rate of 1% to 1.25%. Even in the “optimistic” case, the key-lending rates are thus below the level suggested by the Taylor rule. To my mind, this definitely supports the notion of further interest rate increases.

With regard to my own personal assessment of the input variables for the Taylor rule:

- I expect the neutral rate to be located at the lower end of the bandwidth of 2% to 5%. Lower productivity, lower population growth, and higher propensity to consume suggest higher interest rates. From my point of view, all of this describes the economic status quo and thus differs from the situation in the 1990s.

- I base my assessment of the output gap on the assumption that it is located somewhere towards the higher end of the indicated bandwidth rather than at the lower end. In the course of the financial crisis, the qualifications of many people as well as numerous business models and the resulting investments have lost a lot of value on a permanent basis. Therefore, I think that the econometric models that were calibrated pre-2008 come with the risk of underestimating capacity utilisation. This fits the US labour market. The unemployment rate is currently 4.4% and thus at its pre-crisis lows.

- The current inflation gap amounts to 0.6 percentage points.

Overall, a lot suggests that the key-lending rate should currently be 1.65% (0% neutral real interest rate; 1.4% current inflation; -0.6 percentage points inflation gap; 1.1% output gap).

Conclusion

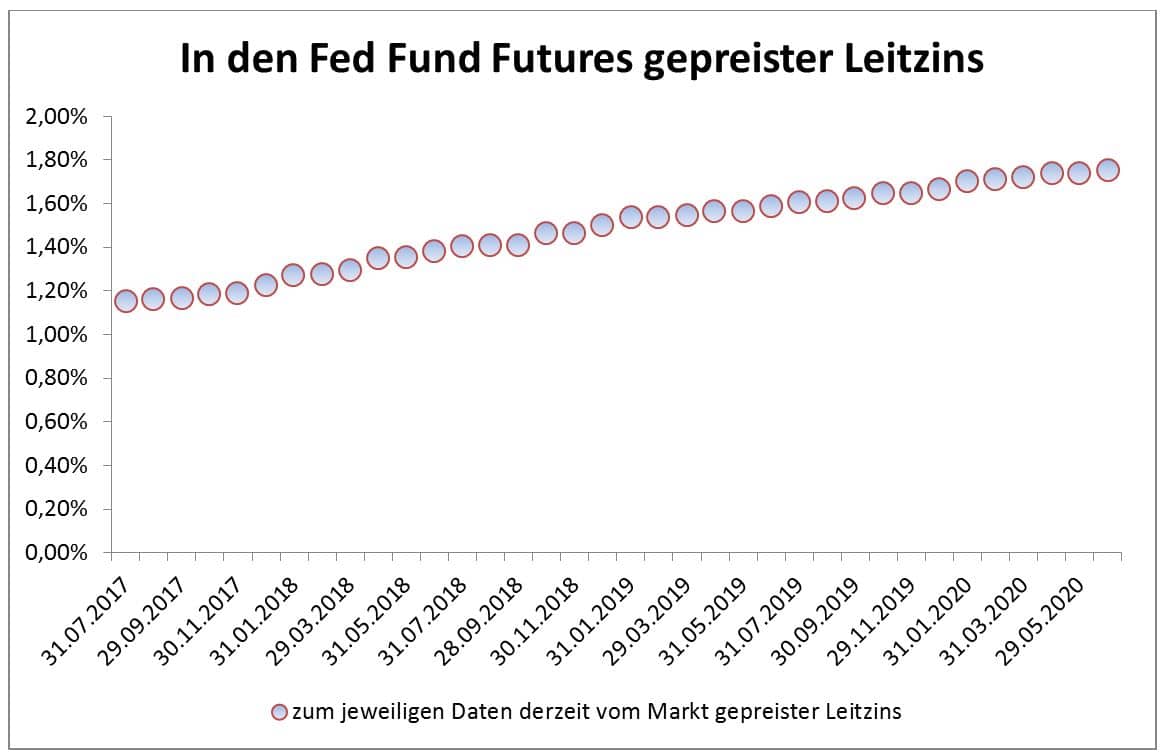

- The Fed funds futures, i.e. derivative contracts that illustrate the market expectation of the future key-lending rate, show that the market expects to see the key-lending rates at 1.75% in the middle of 2020. A Taylor interest rate of 1.65% is roughly in line with the expectations for the Fed funds rate for 2020 currently priced into the market. There is a little wiggle room for an increase in inflation or the continued growth of the economy at its current pace.

Fed funds rate priced into the Fed fund futures contract

Source: EAM/Bloomberg

Please note: Prognoses are no reliable indicator of the future performance of a fund.

- If inflation were to be around 1.9% twelve months from now, which would be in line with the current market expectation, the model would suggest a Taylor interest rate that was 0.75% higher (Inflation is an input variable both for the nominal interest rate and the inflation gap). This also explains why the market is currently paying so much attention to the inflation data. If inflation rises, the Fed will come under pressure to raise interest rates faster and more drastically than currently priced in by the market.

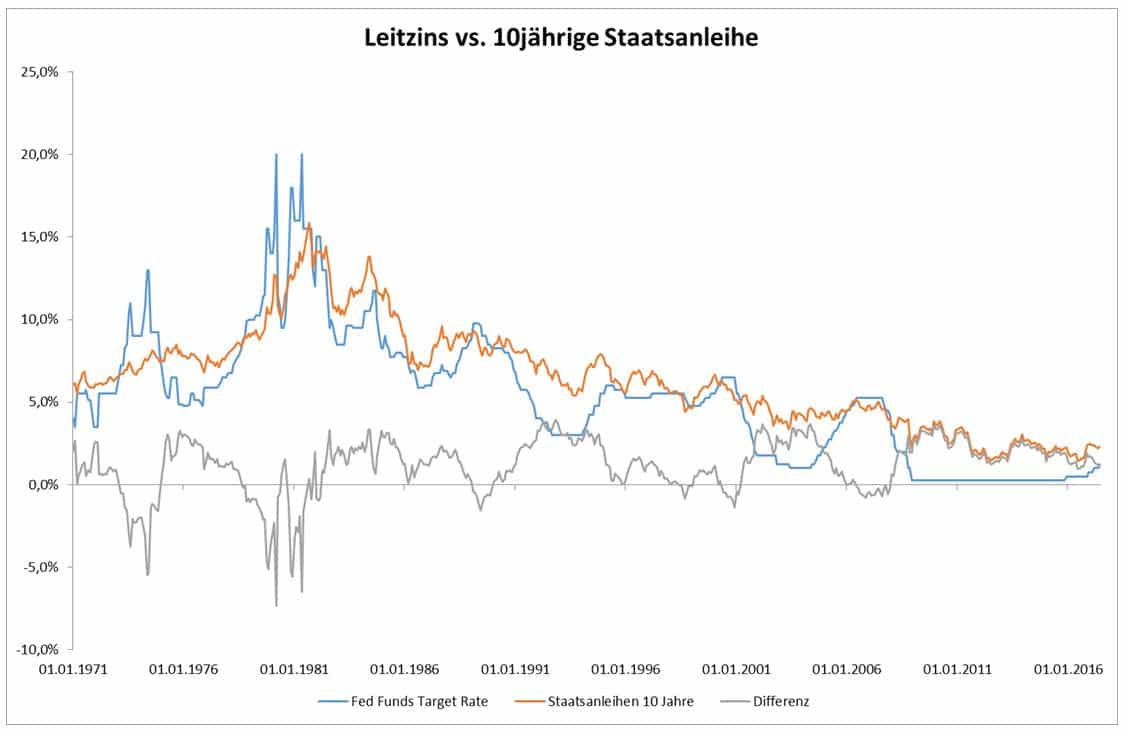

- Based on a Taylor interest rate of 1.65% and a spread of 1.2% for 10Y US Treasuries, which is in line with the average value since 1970, the 10Y yield should be 2.85%. This value is about 60 percentage points above the actual value at the moment.

Fed funds rate vs. 10Y Treasury bonds

Source: EAM

- If the nominal interest rate is really 2%, the unorthodox measures we have seen taken as part of the monetary policy will not have been a one-off event but will continue to play an important part. After all, the next recession will undoubtedly come our way some day. The Fed could then cut the Fed funds rate significantly less than in the past.

Ironically, the eponym of the Taylor rule, John Taylor, could mess up the aforementioned analysis. He famously does not think that the neutral interest rate has fallen significantly in the past years. Therefore, he regards the current Fed funds rate as too low. If John Taylor were to become the next Fed chairman, he might therefore raise rates more significantly than anticipated by the market and myself.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.