Water as a regional risk variable

Water is essential to life. According to a medical rule, a human being can only survive three days without water. There’s a reason why the first step in examining foreign planets is the search for the source of life, i.e. water. A lack of water can make whole regions uninhabitable and force people to migrate, which is why the availability of water has increasingly gained importance on a global scale (sources: derstandard.at, spiegel.de).

The World Resources Institute breaks down water risk into physical, regulatory, and reputation risks. It has derived twelve key indicators from this breakdown in order to be able to evaluate the globally most important water catchment areas.

For example, the physical risk factors measure the ratio of annual water withdrawal to water supply, the frequency of floods, and the severity of droughts. They also measure the return rate, i.e. the amount of water that is reclaimed, and the share of water that is provided by protected ecosystems. The share of freshwater amphibians that are rated endangered by the IUCN (International Union for Conservation of Nature), constitute an indicator for the regulatory risk: a high share implies sensitive ecosystems that could be subject to stricter regulations when it comes to water withdrawal in the future, because the regulatory framework often dates back to times with sufficient water supply and is nowadays obsolete. According to OECD data, groundwater withdrawal has globally nearly tenfold in the past 50 years and demand for water is projected to rise by 55% between 2010 and 2055.

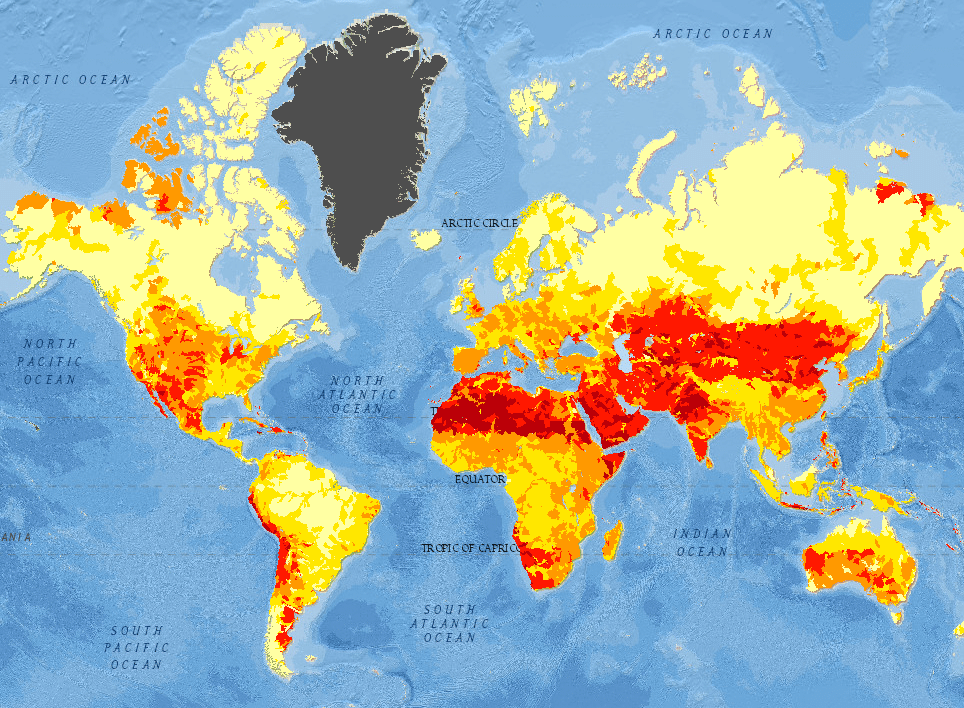

The result of this risk evaluation is the Aqueduct Water Risk Atlas by the World Resources Institute, which facilitates a global comparison of water risks on a regional basis. The regions with low water risk are light yellow, those with high water risk are dark red. Regions without sufficient data are grey.

Overall Water Risk

Source: Aqueduct Water Risk Atlas, World Resources Institute, as of 22 February 2018; www.wri.org

For example, the following risk regions have recently been battling the increasing scarceness of water: California was faced with a drought in 2014 of such a degree that it caused forest fires and the sagging of the ground. Cape Town has been forced to engage in drastic measures to save water since the beginning of the year in an effort to avoid Day Zero (i.e. the day without water).

Water (shortage) as a global risk

The World Economic Forum regards a global water crisis and its ramifications as fifth-biggest risk for 2018. Generally speaking, water shortage has been among the top five risks since 2012. Extreme weather is ranked second for 2018 in terms of global threats (source: World Resources Institute). There is a direct link: the already existing water crisis is due to the lack in measures taken to adjust to climate change, which in turn is connected to extreme weather events. Due to longer dry periods and more intense precipitation, the dried-up soil cannot absorb the rain anymore, as a result of which it drains above ground, and generally less ground water is stored. According to the World Resources Institute, 1 billion people currently live in regions with scarce water resources. By 2025, this number could increase to 3.5 billion. The most frequent reasons for water shortages are water pollution and the resulting threat to freshwater sources as well as climate change, which exacerbates periods of drought and floods, changes precipitation patterns, accelerates the melting of glaciers and thus changes the water supply (source: World Resources Institute).

Since man cannot live without water, the water shortage may result in massive refugee migration, with global effects beyond the locally affected areas. Therefore, this situation has been called a risk with social effects (source: OECD).

Water as footprint of the ERSTE RESPONSIBLE equity funds

In 2015, Erste AM decided as the first investment company in Austria to sign the Montreal Carbon Pledge and has thus undertaken to publish the CO2 footprint of the relevant equity holdings. The signature and the resulting coordinated approach of important asset managers has built up pressure vis-à-vis companies to promote the publication of CO2 data.

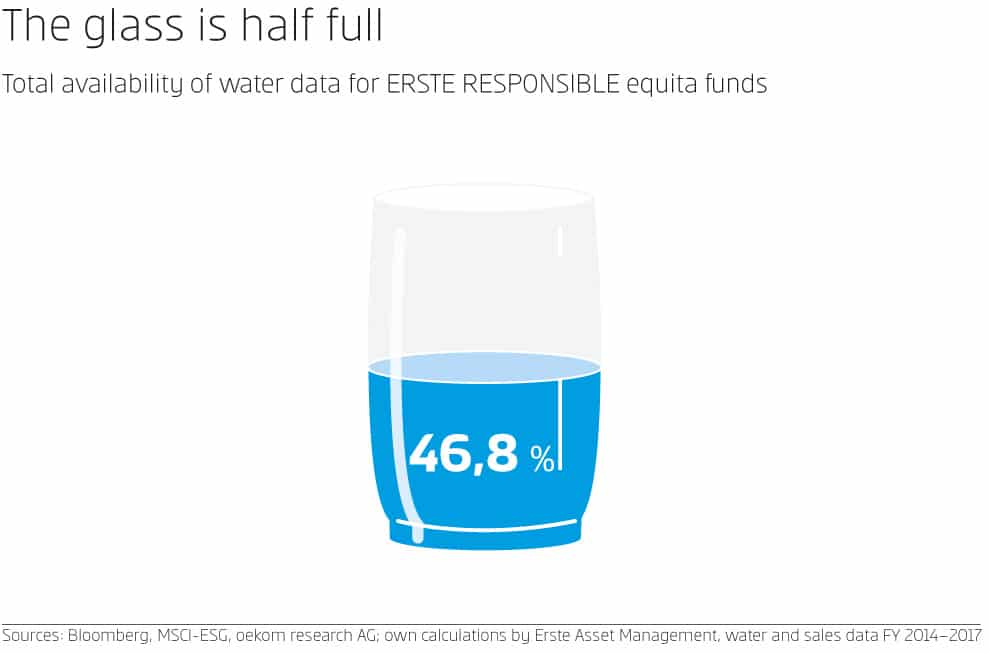

The first-time calculation of the water footprint in Austria for the ERSTE RESPONSIBLE equity funds of Erste AM is meant to become a similar success story. A holistic analysis cannot be limited to the tracking of the CO2 emissions.

The central ratio used for the establishment of the average water intensity of the companies held by the fund is the water consumption as published by the various companies. However, assuming the pioneering role by establishing the first-ever water footprint comes with the downside that many data points do not yet exist at sufficient levels of quality. Nevertheless,to ensure a reliable data base, only those values are considered which areprovided independently by several data providers. Data points that account forless than 80 percent of relevant business activity are not taken intoconsideration. At a total coverage of 50% in terms of portfolio holdings, the resulting set of water data is unfortunately not yet up to par with the CO2 ratios. We are in constant exchange with our research partners in order to achieve a higher coverage ratio and also to facilitate an increased awareness of the relevance of regional water consumption from an investor’s perspective.

Water withdrawal and region as input data for the Erste AM water footprint

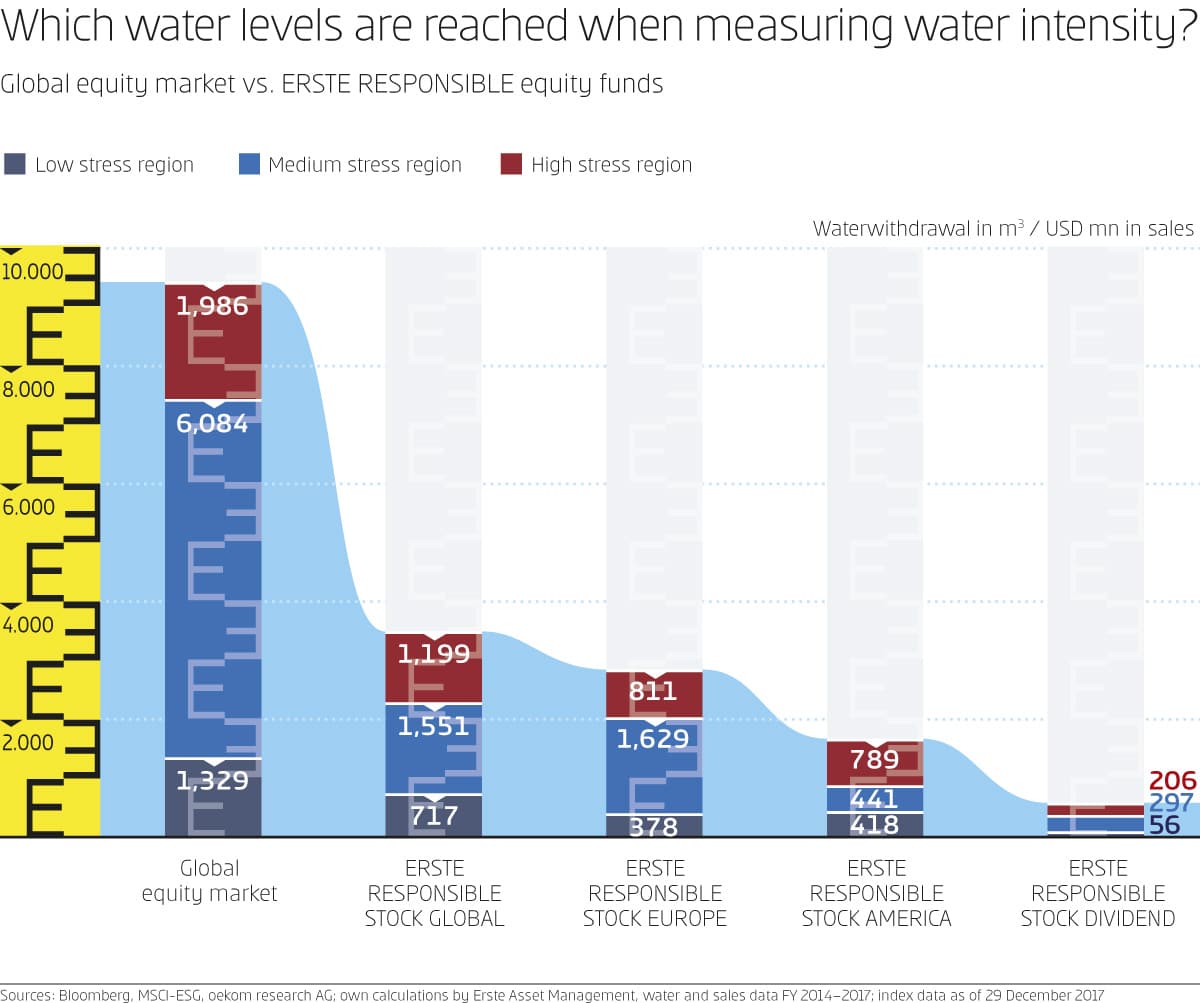

The consumption of freshwater indicates how much water companies consumed in the last fiscal year from surface waters or from the ground water. The value depends strongly on the sector of the respective company. But the attribution of water consumption to water risk regions (high / medium / low) allows for a differentiation within the sector and thus an assessment of the extent to which the company might be affected by a water shortage in the future. To this end, water consumption has to be standardised over annual sales first so as to ensure the comparability of companies of different sizes. In the last step, the water intensity thus established can be aggregated to a weighted average, depending on the regional distribution of locations of the company and the weighting in the fund.

In contrast to the CO2 footprint, the regional component provides a very important additional component for the water footprint. Companies whose production facilities are based in locations with high water stress level harbour a particularly high level of water risk, even if their water consumption is average for the respective sector. This is due to the fact that in these regions the likelihood of a future water shortage is considerably higher than in low-stress regions (i.e. regions with low water stress levels). An actual water shortage can entail an array of implications such as stricter regulations of water withdrawal, massive price increases, or even the closing-down of a production facility. Therefore, the assessment of the water risk seems advisable from an economic perspective. The classification into low, medium and high stress regions is based on the already described risk classification of the World Resources Institute in which physical, regulatory and reputational risks are taken into account. The according world map (pictured above) with regional differentiation can be found also online.

From the perspective of Erste AM, the result shows that the water intensity of the companies in the ERSTE RESPONSIBLE equity funds is clearly lower than in the global equity market both for the various risk regions and overall. This outcome is due to the comprehensive ESG analysis, which all companies that are held by the ERSTE RESPONSIBLE equity funds have to go through. An important partial aspect of the sustainability ratings is the assessment of how much a company depends on high water withdrawal in risk regions. This analysis illustrates that the companies in the ERSTE RESPONSIBLE equity funds are also among the best in their respective sectors when it comes to water management.

[Walter Hatak & Stefanie Schock]

Sources:

https://derstandard.at/1315005461229/Wie-lange-ueberlebt-ein-Mensch-ohne-Wasser

http://www.spiegel.de/wissenschaft/natur/fluechtlinge-klimawandel-und-wassermangel-verschaerfen-gefahr-a-1059195.html

http://www.oecd-ilibrary.org/environment/groundwater-allocation_9789264281554-en

http://www.oecd.org/water/water-quantity-and-quality.htm

http://www.spiegel.de/spiegel/kapstadt-suedafrikas-metropole-geht-das-wasser-aus-a-1190386.html

http://worldwaterday.org/theme/

http://www.wri.org/our-work/topics/water

http://www.wri.org/sites/default/files/pdf/aqueduct_metadata_global.pdf

https://www.wri.org/sites/default/files/aqueduct_coutnry_rankings_010914.pdf

http://www.wri.org/our-work/project/aqueduct/methodology

https://www.welt.de/vermischtes/article160308379/Ueberleben-ohne-Wasser-wenige-Tage-moeglich.html

http://www.spiegel.de/wissenschaft/natur/fluechtlinge-klimawandel-und-wassermangel-verschaerfen-gefahr-a-1059195.html

http://www.spiegel.de/wissenschaft/natur/duerre-in-kalifornien-nach-fuenf-jahren-offiziell-fuer-beendet-erklaert-a-1142481.html

http://www.ovgw.at/media/medialibrary/2016/04/Studie_Wasserversorgung_2015.pdf

http://www3.weforum.org/docs/WEF_GRR18_Report.pdf

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.