Almost every outlook for 2024 mentioned the super election year and landmark political decisions. A particular focus was on the presidential election in the USA, which brought back an old acquaintance, Donald Trump, to the White House and also turned the Senate and the House of Representatives in Washington red (the colour of the Republican Party in the USA).

The US election will also remain a central topic in the coming year: what consequences will Donald Trump’s re-election as president have for the global economy? Will the Republican really implement his far-reaching plans for more tariffs and protectionism, or does he just want to strengthen his negotiating position with the EU and China? Where is Europe heading in light of Trump’s plans?

In the following, we are going to look at the most important political and economic trends for 2025 and provide an overview of the strategies investors can use to position themselves in the coming year.

Will interest rate cuts soon be a thing of the past in the USA?

Donald Trump’s clear victory in the US election in November has already caused significant movements on the financial markets. US equities and cryptocurrencies such as Bitcoin have benefited particularly from the election result, and the US dollar also appreciated in the days following the election. On the one hand, the market expects Trump to take pro-business measures, such as the announced tax cuts for companies: “If these are implemented, share prices should rise again due to the positive effects on corporate earnings,” as Gerold Permoser, CIO of Erste Asset Management, summarises the situation.

However, there is a catch: such policies harbour the risk of further increasing the USA’s already high national debt. This could lead to higher yields on US Treasury bonds, as investors demand higher premiums for holding them. For the US Federal Reserve, this would limit the scope for further interest rate cuts.

Trump’s planned measures could have an impact on inflation and the US government budget. This could limit the US Federal Reserve’s room for manoeuvre. Sources: Valerie Plesch / dpa / picturedesk.com

In any case, the US economy continues to perform well, and the labour market has not weakened noticeably so far. The market has already priced this in to a large extent – expectations of interest rate cuts for the coming year have fallen significantly as a result of the election. That being said, according to Permoser, there is also room for potential disappointment: “The period of interest rate cuts in the USA could soon come to an end, which could bring about disappointment.”

„Trumponomics“ could create more volatile environment

The other side of “Trumponomics” – Donald Trump’s economic plans – aims to increase tariffs and protectionism. Trump has announced import tariffs on Chinese goods of up to 60% and the short-term implementation of punitive tariffs of 25% on all goods from Mexico and Canada. If these plans were put into action, they could trigger a spiral of import tariffs in Europe and China as well. This would make goods more expensive, impact exports and thus put a damper on the global economy. “We therefore have to expect higher volatility in the markets due to Trumponomics,” says Permoser.

In general, he sees the risks associated with Trump’s recent presidency as only marginally priced into the market at the moment. The VIX, the index that measures volatility and uncertainty in the US equity market, is currently below its long-term average. The motto for 2025 is therefore to become much more cautious and to “drive on sight”.

European economy at the crossroads

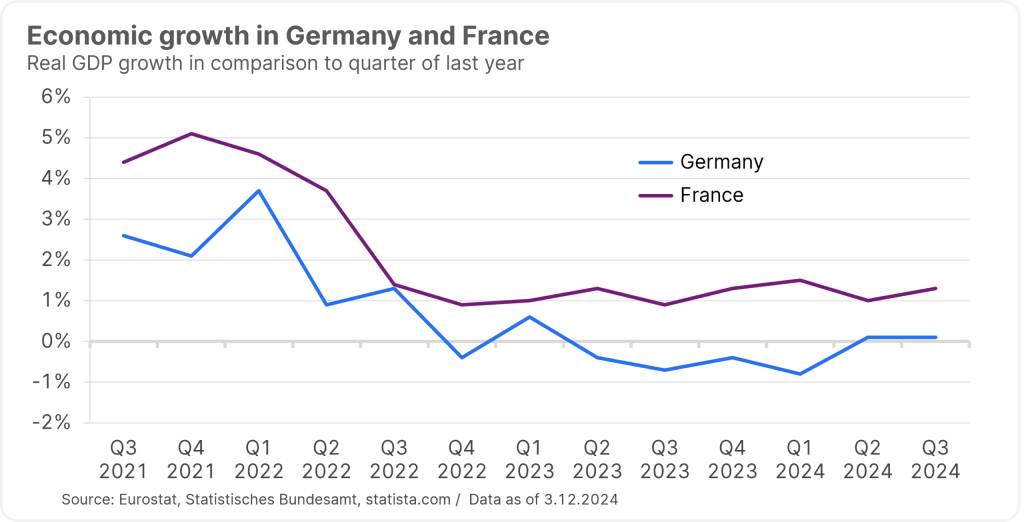

The trade restrictions that have been announced would be another blow for the already faltering European economy. As the latest economic data show, growth in the major European economies such as France and Germany remains weak. Higher tariffs would be a heavy burden on exports and further hamper the economic recovery in Europe.

“The uncertainty surrounding Trump’s policy is an issue in Europe,” summarises Permoser. However, the economic data is gradually bottoming out. The European Central Bank has initiated a turnaround on interest rates and is clearly moving away from a hawkish stance. Inflation is also falling towards the central bank’s target, which offers scope for further interest rate cuts by the institute. “Falling interest rates should help the European economy on its way,” Permoser says. In addition, real wages are rising after the decline in inflation, which should support consumption.

In Germany, the situation is somewhat unclear following the collapse of the “traffic light coalition” government. However, the budgetary framework there also offers scope for economic support measures. “One sticking point will be how the next government in Germany uses this leeway for support measures,” explains Permoser, already looking ahead to the upcoming parliamentary elections in Germany.

Has the tech rally run out of steam?

AI: in 2024, these two letters again not only sparked a lot of imagination, but also generated a large part of the gains on the equity market. Even with the “Magnificent 7” in mind, i.e. the tech companies Alphabet, Amazon, Apple, Facebook, Microsoft, Nvidia, and Tesla, the shares of AI high-flyer and chip giant Nvidia accounted for more than 50% of this year’s gains. So, the market is very concentrated in the technology sector.

“We don’t think that this development will continue – even though, to be honest, that was already our forecast last year,” Permoser admits. On the one hand, earnings expectations in the technology segment are gradually levelling out. On the other hand, there is currently a pause in the development of artificial intelligence. The business model that would allow the long-term, sustainable monetisation of AI has yet to be found. The performance in the tech sector should therefore converge more and more, with Trump’s expected deregulation policy also providing support. However, higher tariffs or a possible trade war would create the opposite scenario: “Tech companies are not likely to benefit from this.”

Will Trump do away with sustainability?

One of the losers in the US election were shares in the renewable energy and environmental technology sectors. The focus here is on the Inflation Reduction Act, one of the central laws under the soon-to-be former President Joe Biden. Said Act has led to a great deal of money being invested in sustainability themes such as renewable energies. The crux of the matter, however, is that around 90% of the green energy-related jobs created by the Act are in Republican states. In addition, large portions of the funds released by the act have either already been spent or earmarked for spending. “From our point of view, there is only limited scope for repealing the Act entirely,” says Permoser.

A complete repeal of the Inflation Reduction Act and thus the cancellation of the multi-billion investments in renewable energies is unlikely. Source: unsplash

Furthermore, during Donald Trump’s first presidency in the USA, more was invested in alternative energies than in fossil fuels for the first time, as Permoser notes. The background to this is purely economic – at this point, solar energy, for example, is already one of the cheapest energy sources around. “We don’t think it will be any different this time. As long as there is no additional demand for fossil fuels on the market, more oil will not be produced either, because that would simply not make sense in terms of market forces.”

Strategies for 2025

“The chances of solid returns remain intact in 2025,” says Permoser, looking ahead to the coming market year with optimism. In the context of rising uncertainty, it might make sense to rely on a mix of several asset classes – for example, with global mixed funds such as ERSTE OPPORTUNITIES MIX, which has performed quite positively in the first half of 2024 since its launch. ERSTE REAL ASSETS has also been one of Erste AM’s top performers this year and could be worth a look at for 2025.

If you are looking to invest in equities, a broadly diversified equity fund may be the right choice for you – for example, the ERSTE RESPONSIBLE STOCK GLOBAL equity fund, which invests worldwide. On the fixed income front, ERSTE BOND CORPORATE PLUS, a corporate bond fund that invests in investment-grade subordinated bonds, may be of interest.

It should be noted that investing in securities always involves risks as well as opportunities. The prices of individual funds may fluctuate considerably.

Conclusion

Even though the equity markets rallied briefly after the US election, it would be unwise to be overly optimistic about the year ahead. Donald Trump’s election marks the return of uncertainty to the White House. It is still unclear which of Trump’s proposed measures will actually be implemented. Tax cuts would have a positive impact on corporate earnings, but a more restrictive trade policy by the USA as an economic powerhouse could have a dampening effect on the global economy.

Europe would not be spared either: higher import duties from one of its most important trading partners would probably be another factor hindering economic recovery in this region. On the other side of the coin, the decline in inflation offers further leeway for interest rate cuts in the Eurozone, which could certainly help the European economy in its recovery.

All in all, Permoser rates the positive outlook for the global equity and bond markets as intact. He believes that the risks at the political level are offset by positive factors such as the continued growth of the global economy, falling key-lending rates around the world, and stimuli from countries such as China. On the stock exchanges, the investors’ attention will focus on dividends, real earnings, inflation, and valuations. “If companies continue to report earnings growth and pay dividends, prices will reflect this.”

Please note: forecasts are no reliable indicator of future performance.

Risk notices

ERSTE OPPORTUNITIES MIX

The fund pursues an active investment policy and does not follow a benchmark. The assets are selected at our discretion, without any constraints to the latitude of judgement on the investment company’s part.

For further details on the sustainable strategy of ERSTE OPPORTUNITIES MIX and on the Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐related disclosures in the financial services sector and the Taxonomy Regulation (Regulation (EU) 2020/852) please refer to the current prospectus, point 12 and the appendix, “Sustainability principles”. When deciding to invest in ERSTE OPPORTUNITIES MIX, please take into account all features and goals of ERSTE OPPORTUNITIES MIX as described in the fund documents.

Warning notices according to the Austrian Investment Fund Act of 2011

In accordance with the fund terms and conditions approved by the Austrian Financial Market Authority, ERSTE OPPORTUNITIES MIX intends to invest more than 35% of assets under management in securities and/or money market instruments from public issuers. For a detailed statement on these issuers, please refer to the prospectus, section II, sub-section 12.

ERSTE REAL ASSETS

The fund pursues an active investment policy and does not follow a benchmark. The assets are selected at our discretion, without any constraints to the latitude of judgement on the investment company’s part.

Warning notices according to the Austrian Investment Fund Act of 2011

ERSTE REAL ASSETS may invest a significant portion of its assets under management in shares of investment funds (UCITS, UCI) as defined by sec 71 of the Austrian Investment Fund Act of 2011.

ERSTE RESPONSIBLE STOCK GLOBAL

The fund pursues an active investment policy and does not follow a benchmark. The assets are selected at our discretion, without any constraints to the latitude of judgement on the investment company’s part.

For further details on the sustainable strategy of ERSTE RESPONSIBLE STOCK GLOBAL and on the Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐related disclosures in the financial services sector and the Taxonomy Regulation (Regulation (EU) 2020/852) please refer to the current prospectus, point 12 and the appendix, “Sustainability principles”. When deciding to invest in ERSTE RESPONSIBLE STOCK GLOBAL, please take into account all features and goals of ERSTE RESPONSIBLE STOCK GLOBAL as described in the fund documents.

ERSTE BOND CORPORATE PLUS

The fund pursues an active investment policy and does not follow a benchmark. The assets are selected at our discretion, without any constraints to the latitude of judgement on the investment company’s part.

For further details on the sustainable strategy of ERSTE BOND CORPORATE PLUS and on the Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐related disclosures in the financial services sector and the Taxonomy Regulation (Regulation (EU) 2020/852) please refer to the current prospectus, point 12 and the appendix, “Sustainability principles”. When deciding to invest in ERSTE BOND CORPORATE PLUS, please take into account all features and goals of ERSTE BOND CORPORATE PLUS as described in the fund documents.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.