The Brexit-vote was a non-event, it seems. At least, that is what global equity markets are telling us. Since June 24 – the day after the referendum – US, European and Japanese indices all have gained around 10% in local currencies (up to August 19). Emerging Markets, on average, made a similar move as well. Whether the rally will continue depends on a number of factors, pointing in opposing directions. While the fundamental backdrop suggests remaining cautious and also valuation is not supportive, low bond yields and economic policy will likely continue to provide tailwinds for global equity markets.

Index Performance (Jun 23, 2016=100)

Source: Bloomberg, Erste Asset Management

Sluggish economic growth

The global growth outlook continues weakening. After the Brexit vote, consensus forecasts for 2017 GDP growth in the UK, the Eurozone and the US have been cut by 1.5, 0.4 and 0.1 percentage points respectively. Also the IMF in its recent update of the World Economic Outlook revised its growth projections again down by 0.1 percentage points to 3.1% and 3.4% for 2016 and 2017. The acceleration in 2017 is only due to faster growth in emerging economies.

The view that the developed world is entering a period of secular stagnation either because of a structural lack of demand (the Keynesian view) or a slowdown in productivity growth combined with demographic trends (the supply side version of the story) is increasingly gaining popularity. The bottom line for investors is that neither the near-term nor the longer-term outlook suggest that economic growth will be the main source of higher stock prices – at least in the developed world.

Lackluster earnings performance

In line with the macro-economic backdrop, earnings have been a drag on equity performance in recent quarters. In the US, the second quarter 2016 was the 7th quarter in a row with falling earnings, in Europe – which has had a lackluster earnings performance for the past five years – it will be the 4th.

Earnings revisions 2014-2016

Source: Bloomberg, Erste Asset Management

This is also reflected in analysts’ earnings revisions in recent months. Both in the US and in Europe, earnings estimates have drifted lower since the beginning of the year. Particularly in Europe the earnings outlook deteriorated significantly, with estimated EPS cut by more than 12% since January.

That said, the current earnings season was better than expected. On both sides of the Atlantic, positive earnings surprises outnumbered disappointments by a significant margin, fueling expectations that the next quarter could bring an end to the earnings recession.

Valuation rich by historical standards …

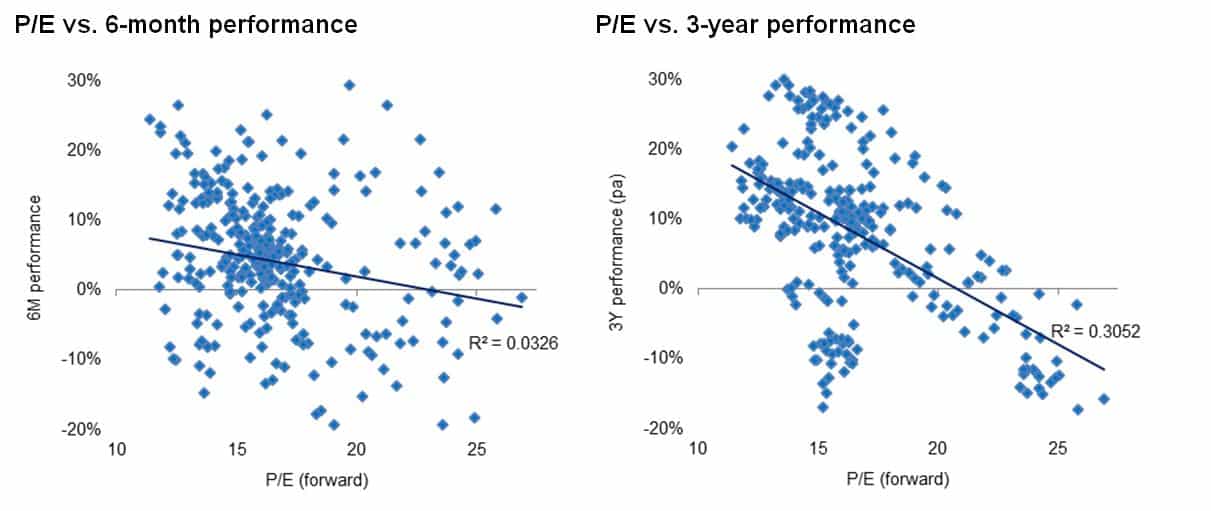

In the US, Europe and emerging markets, current PEs are about 20% above their five year average and also significantly above long-term levels. Only Japan does not appear to be overvalued by historical standards. That said, valuation is not a reliable indicator for the near-term performance of markets. For the US (which offers longer stock-price series than any other market) the regression between the market’s price-earnings ratio (P/E) and its subsequent six-month performance shows only a modest negative relationship, and the explanatory power is weak (R2 of just 3%).

Over the longer-term, the negative link between valuation and index performance is more pronounced. But even starting from an elevated earnings multiple of 18.6x (current level), regression results imply a three-year return of c.4% per annum based on data since 1990 – which is not thrilling, but clearly not a disaster scenario.

Valuation and index performance (S&P 500)

Source: Bloomberg; Erste Asset Management.

… but attractive relative to fixed income

While equity valuation may not be particularly enticing relative to its own history, relative to fixed income stocks appear highly attractive. Calling the peak of the bond market has turned out to be a fool’s game, but, for example, with German and Japanese ten-year rates below zero, there is little further upside. Holding European stocks is equivalent to holding 10 year German or Japanese sovereign bonds to maturity, even if dividends are cut by 50% by tomorrow and the Euro Stoxx 600 drops 20% over the next ten years. Nothing is impossible, as we learnt in recent years, but this looks like a comfortable margin of safety.

Fiscal policy support?

On top of valuation relative to fixed income, the recent strength in equity markets could be driven by shifting investor’s expectations with regard to economic policy. In the US as well as in Europe, fiscal policy will likely turn more expansionary, mostly driven by the rise of political populism – in Europe fueled by the Brexit vote and migration-related issues on the Continent, in the US related to the presidential race. In addition, Japan will likely rely increasingly on fiscal easing, because of Prime Minister Abe’s famous “three arrows” so far only the monetary policy-arrow has been shot. A turn toward a more expansionary fiscal policy in all three main developed regions would result in stronger demand and (nominal) growth, which – at moderate levels of inflation – is generally beneficial for equities. After years of solely relying on central banks, markets see a second ray of hope.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Interest rate cuts at the door

After the rapid and sharp interest rate increases in 2022 and 2023, the pendulum is now swinging in the opposite direction. After the European Central Bank (ECB), the US Federal Reserve will cut key interest rates for the first time this Wednesday, thus initiating a new cycle of interest rate cuts. What does all this mean for the economy and what conclusions can be drawn from it for investments?

The new age of protectionism

The path towards a clearly fragmented global economy is continuing. Recently, the increase in tariffs on Chinese electric cars in the USA and the European Union has been particularly noticeable. What impact is the rise of protectionism having on the global economy?

US elections: are the billions of investments in green technologies at risk?

Two years ago, the USA initiated its energy transition with the Inflation Reduction Act. This was followed by billions in subsidies and investments in renewable energies. What will happen to the Act if Donald Trump makes a comeback to the White House? Is the “Green Rush” in danger of coming to an end?