France’s controversial pension reform is about to be signed off. Roughly one week after its passage in parliament, only the Constitutional Council’s verdict is still pending, the Council having to examine the legality of the reform. French President Emmanuel Macron is confident that the pension reform will be in place “by the end of the year.” “This reform is necessary,” Macron emphasized again recently in a TV interview. Meanwhile, protests against the reform escalated last week, with demonstrations in Paris leading to riots. Protesters also blocked several ports, train stations and parts of Paris’ Charles-de-Gaulle airport.

Macron’s reform aims to gradually raise the retirement age from 62 to 64 years, bringing it closer to the European average. In fact, retirement already starts later on average: Those who have not paid into the system long enough for a full pension work more years. At 67 years citizens receive a pension without any deduction, regardless of how many years they paid into the system. This threshold age will remain the same; however, the number of individual years needed to receive full pension will increase more quickly. In addition, the minimum monthly pension is to be raised to around 1.200 EIR.

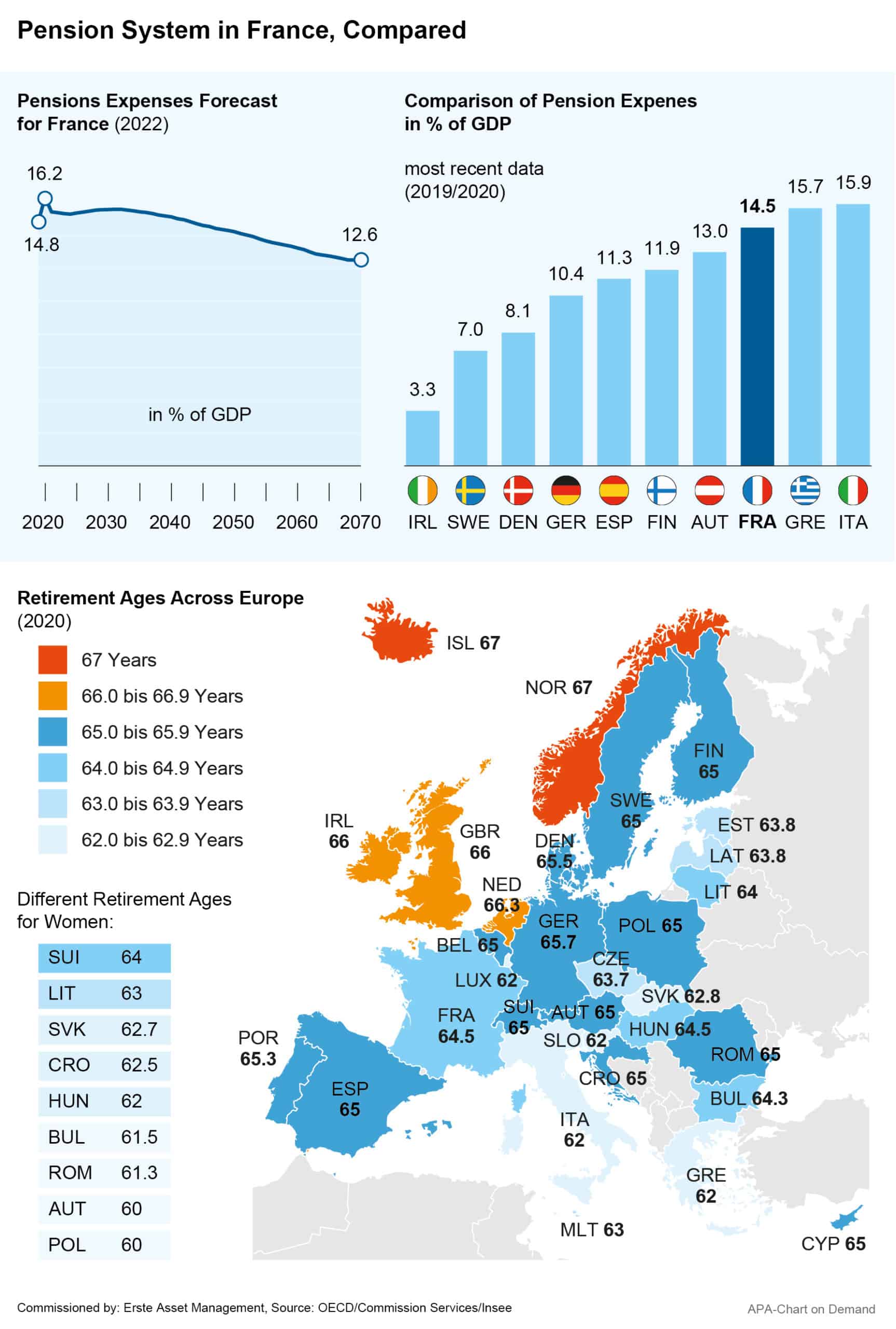

Retirement Age Raised to Fill in the Gap In Pension Funds

With the reform, the government plans to close a looming gap in the pension funds. The public pension system expenses in France accounted for 14.5 per cent of economic output (GDP) in 2021, according to OECD data. That is the third-highest figure in the EU, surpassed only by Greece and Italy, each with just under 16 per cent of GDP. Eurostat data for 2020 even puts France in second place in a comparison of countries.

This contrasts with a further increase in life expectancy and thus longer retirement periods in France. According to a study by the French Ministry of Economy in 2022, life expectancy for men is expected to rise from the current 80 to around 87 years and for women from around 86 to 91 years by 2070. Furthermore, the ratio of people of retirement age to the number of people working is expected to shift drastically. In 2019, the ratio was just under 37 per cent, meaning that on average there is one retiree for every 3 people working. However, according to the study, by 2070, this figure is expected to rise to just under 57 per cent.

The share of pension system spending is thus likely to rise to between 15 and 16 per cent of GDP by 2030, the ministry predicts. As shown in the study published leading up to the reform plans, this share is likely to decline over time even without a pension reform, because some effects of previous pension reforms affect expenses with a significant delay. However, this forecast still sows a share markedly above 12 per cent after 2030.

Macron Remains Adamant About the Reform Plans

Accordingly, Macron also defends the necessity of the reform, noting in a recent television interview that the reform is very difficult. “We are asking people to make an effort. This is never popular.” He asked, “Do you think I enjoy doing this reform?”, replying himself, “No,” and adding, “Between the polls and the short term and the general interest of the country, I choose the general interest of the country.”

The public, as well as the opposition parties, have a very different view. Since no parliamentary majority could be found for the reform, Macron had to resort to the much-criticized constitutional article 49.3 to push through the reform act. This allows a law to be passed without a final parliamentary vote if the government survives a subsequent vote of no confidence. While the French government narrowly escaped being overthrown in such a vote last Monday, the fast-track procedure pushed through by the government further fueled protests against the reform.

However, the protests are unlikely to dissuade Macron from his will to reform. During his first term in office, the French president lowered corporate taxes and pushed through a labour market reform. According to some economists, the consequences of this reform are already in evidence: between Macron taking office and in Q4 of 2022, the unemployment rate fell from 9.5 to 7.2 per cent.

Further reforms are likely necessary – among other things, to reduce national debt. Rating agency Standard & Poor’s (S&P) downgraded France’s credit rating outlook from “stable” to “negative” in December. Although the rating for long-term foreign currency bonds initially remained at “AA,” a future downgrade looms. S&P cited increasing fiscal risks as the reason for the change in outlook, maintaining that the economic downturn in Europe is likely to limit growth in France.

Cour des Comptes Calls for Further Consolidation of Public Finances

France’s supreme audit institution Cour des Comptes also recently expressed concern about the country’s financial situation and called for fiscal consolidation. The state of France’s public finances will remain among the worst in the eurozone in 2023, the Cour des Comptes said in March.

While a reduction in government spending was actually planned in 2022 following the coronavirus pandemic, the government resorted to further support measures in view of the Ukraine war’s impact. The Cour des Comptes expects a public deficit of 5.0 per cent of GDP, delaying any reductions in the deficit and debt quota. The Cour des Comptes therefore called for a strategy for the determined reorganization of public finances.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

USA – a country is voting on its future

The day of the US election has arrived, bringing an end to a long, intense and exciting election campaign. What economic course could the US enter after the election and what impact can be expected on the country’s already high debt level?

The four seasons: when should I buy equities, Bitcoin, or gold?

Just as in nature, there are different seasons in the economy. This also has an influence on the stock markets – depending on the season, different asset classes such as equities, gold or bonds make sense. The good news for investors is that you don’t necessarily have to worry about the seasons; you can simply leave it to the experts.