Ladies and gentlemen, we are officially on a roll! Croatia has been finally awarded the much awaited investment grade rating, coincidentally (or not) by the same rating agency that first revoked it seven years ago. Admittedly, the nation’s reaction to it was pretty bland (quite unlike the one after getting in the finals) (1) with an in-house estimate of not a single beer per capita drunk on that account. Not surprising, given that the unbearable lightness of being and lack of macro data awareness still remain firmly rooted in this nation’s mindset. There is no question about the fact that recent trends look promising, but have we really made progress or is Croatia merely a collateral beneficiary of positive externalities as some analysts would like to suggest?

The pros

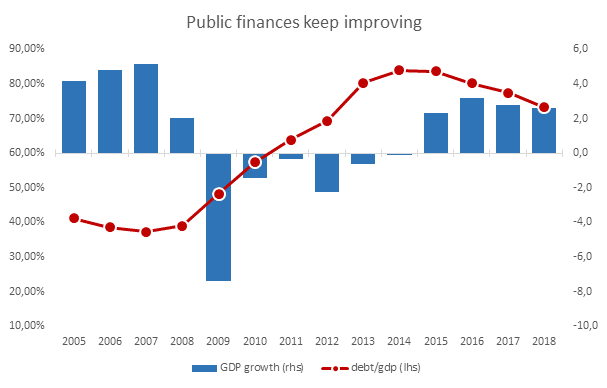

Markets have always been ahead of rating agencies and if one looks only at Croatia’s bond yields, recent rating upgrade was a slam dunk deal waiting to happen. Fiscal metrics have been improving and although debt/GDP level of 73,3% is still high on an absolute level, it has been slashed by 10pp in less than three years. Good macro data coupled with good market data give us a decent chance to keep our debt/GDP trajectory on a sustainable level – to say the least. With long term bond yields now below the nation’s GDP growth rate we have a real chance of bringing debt metrics down to textbook levels.

Note: Past performance is not indicative of future development. Source: EAM

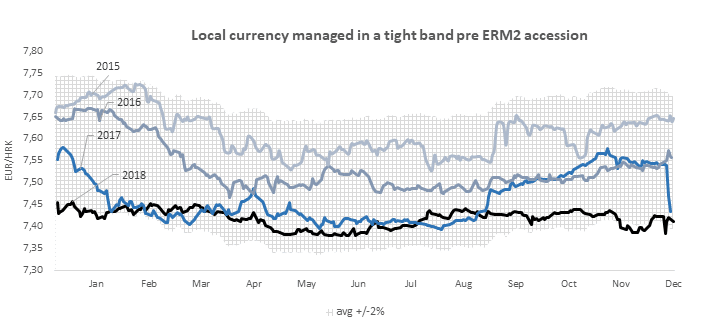

Tax-rich domestic consumption remains the back-bone of the recovery. It has been additionally boosted by a 3-step income tax reform targeting mid and high income workers who are, truth be told, a scarcity in this area, but a potential that the government is willing to work on. Fiscal surpluses are no more an exception, but a rule – in spite of the fall of Croatia’s biggest retailer and state guarantees being activated in relation to the recent shipyard industry problems. August should bring changes to the profit tax law and hopefully help the ailing corporate sector that is still deleveraging while at the same time households are going rampant by bringing the total stock of consumer credit loans to some 10% away from the total stock of home loans. Increasing EU fund absorption is also a benefit, as it fosters investment growth, but also as it keeps a lid on the euro exchange rate helping local currency confirm a yearlong appreciating pattern only months before Croatia officially applies for the European Exchange Rate Mechanism (ERM2) procedure.

Note: Past performance is not indicative of future development. Source: EAM

The latter should also be a formality, as Croatia already qualifies in 4 out of 5 criteria (compatibility of legislation, price stability, public finances and convergence of long term interest rates) with the only non-qualifying criterion being the exchange rate stability that only gets measured once you officially opt for the club. Back-testing the currency pair shows a clear CNB commitment to keep the pair in a narrow band, with only glimmers of seasonal volatility, something we do not expect to change anytime soon.

The cons

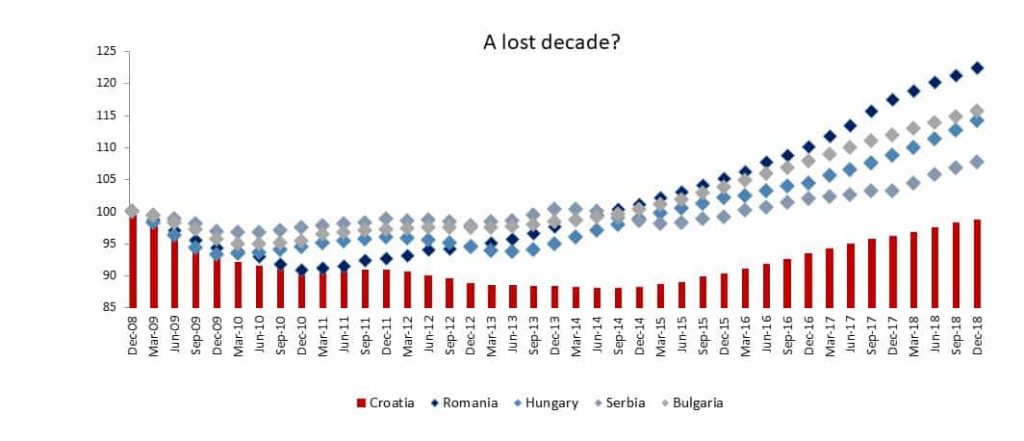

Analysts warn that all this might not be enough though. True, when compared within its peer group, Croatia can indeed be labeled laggard (regardless of one’s Excel skills).

Note: Past performance is not indicative of future development. Source: EAM

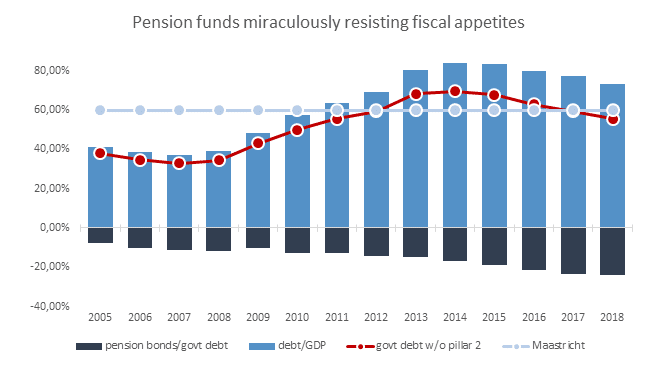

True, our normalized GDP has still not reached the level it had ten years ago. True, we got lucky because our main trading partners fared well and our flagship tourism sector generating almost 20% of GDP went with the flow. True, a sizeable outbound migration distorts per capita numbers on the upside. There’s no doubt that more should have been done and that government structures claiming exclusive merits for the whole progress interfere with common sense (and show lack of good taste for that matter). However, it is also true that a lot more could have been done differently which would probably have made us worse off. Some of our peers opted for a major pension system overhaul. Croatia hasn’t. Pension funds’ government bond holdings currently make almost 25% of government debt. Switching these assets to the first pillar and sterilizing them would have made the debt ratios look far better at any point of time. Although the concept had been flirted with, it was miraculously put on the back burner.

Note: Past performance is not indicative of future development.

To sum it up, another good year might be ahead of us. Yes, we are making progress in baby steps (2) and yes, we could have done better, but it’s a sunk cost anyway (3). We see green shoots in our assets under management rising (over 800mln EUR, thank you very much), real estate prices recovering, households leveraging and global backdrop offering positive momentum for future debt issues. Fitch delivering the same verdict in June and siding with S&P Global Ratings could offer an additional boost and provide such a great start to this summer season. Stay tuned!

(1) To all those of you now frantically googling “Croatia finals”…like, seriously?

(2) Despacito was the most googled word in Croatia in 2017. It means slowly, in Spanish.

(3) To all those of you now frantically googling “Despacito”…like, seriously?

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Deficit spiraling out of control: French government plans drastic austerity program

The high deficit in the French national budget is forcing the new government to implement drastic austerity measures. Investors are keeping a close eye on the announced plans, as the tense financial situation has been noticeable on the stock market for some time.

Tense situation in the Middle East: Will oil prices rise again?

Oil prices have fallen significantly in the year to date, which also had a noticeable dampening effect on inflation. However, this could change with the further escalation in the Middle East. Following the Iranian missile attack on Israel, Prime Minister Netanyahu announced retaliation.

What effects could DeepSeek have on the technology sector?

The new AI model from Chinese start-up DeepSeek caused a stir on the stock market a fortnight ago. The seemingly much more efficient and therefore cheaper model caused the share prices of many a tech heavyweight to plummet. Although the initial market reactions were probably exaggerated, one question remains: what long-term impact will DeepSeek have on the big tech companies?