The multi-billion infrastructure and defense package in Germany has caused a lot of movement in the bond market in the eurozone. Meanwhile, the major central banks are facing the challenge of finding the balance between slowing economic growth and rising inflation.

Daniel Bebesy, Fixed Income Portfolio Manager at Erste Asset Management Hungary, talks about the latest decisions of the world’s central banks and their impact on the bond market. In his view, the current market uncertainty certainly argues in favour of bond positioning in a portfolio. Note: Please be aware that investing in securities involves risks as well as opportunities.

There were several central bank meetings recently. What are the major takeaways for you?

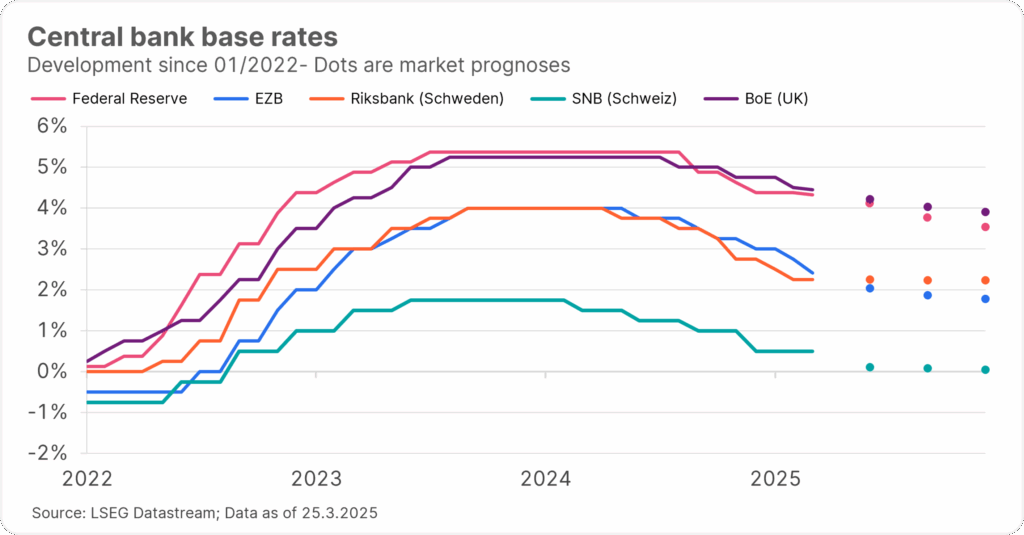

There were couple of important developed market central bank rate setting meetings last week. The overall message investors received, was that central banks on both sides of the Atlantic are facing the unpleasant combination of slowing economic growth and rising inflation. Uncertainty due to US tariff threats was a dominant theme for all Central Banks. The Federal Reserve kicked off the series of meetings and in line with expectations left the base rate unchanged. Nevertheless the Fed adopted a more pessimistic outlook in its latest quarterly economic projection (SEP). The GDP (gross domestic product) growth estimate for this year had been lowered, while inflation projection was moved higher. Despite the changes, the Fed still expected two rate cuts for this year, but the so-called dot-plot chart reflected some hawkish tilt among the Fed officials.

What about the other central banks?

A similar shift in the voting pattern could be detected in case of the Bank of England, where contrary to the previous months only one MPC (Monetary Policy Committee) member voted for lower rates this time. The key rate remained unchanged at 4.5%. However, the decision makers indicated that the door remined open for lower rates, but caution was requited at the current stagflationary environment.

The base rate remained unchanged at 2.5% in Sweden as well, and the central bank reiterated that the easing cycle was basically finished. The Swiss National Bank was the only one in the last weeks that opted for a cut, but also SNB claimed that a further reduction was less likely.

Note: Prognoses are not a reliable indicator of future performance.

The bottom line is that the rate decisions of the past few weeks revealed that central banks were getting more cautious and despite the sluggish GDP growth they were not willing to risk further aggressive easing.

What do you expect for the euro-zone in the next 6 to 12 months? What key indicators are you watching most closely?

The changing global environment obviously has its impact on the Eurozone and the ECB policy making as well. Nevertheless the German fiscal expansion and the broader Eurozone defense spending stimulus make things even more complicated. Early this year recession fears strengthened again for the Eurozone, since the economic bloc where underlying growth had been already weak, was considered the main victim of Trump’s trade war. Then came the historical fiscal regime shift in Germany, delivering the largest fiscal stimulus since the reunification, and this aggressive move obviously rewrote earlier scenarios.

Despite the fact that package got approved in the German Parliament, there are still some uncertainties regarding its overall impact. The fiscal multiplier of the defense spending package is heavily debated, and the key question is whether the stimulus can change some structural factors in the economy that could contribute to faster potential growth on the longer run. The example of the German reunification showed that a stimulus on this scale has the potential to move the so-called neutral rate higher.

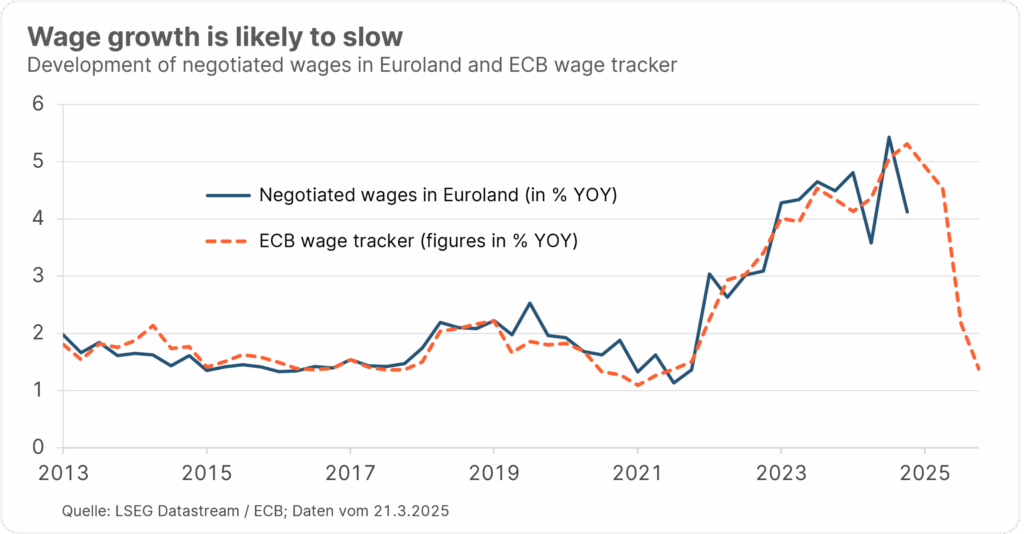

Nevertheless on the short run some headwinds certainly remain. Trade war with the US, intensifying competition from China, and higher energy prices put pressure on growth and still justify less restrictive monetary policy from the ECB in my view. Probably we will not get as much cuts, as market expected early this year, but slowing service inflation and the expected deceleration of wages in the Eurozone, reflected by the ECB survey are key indicators for me that validate further cuts. On the other hand, one has to pay attention to the recent sudden improvement of some sentiment indicators and the firming credit activity in the Eurozone, but these developments could be fragile in my view, especially if slowdown in the US intensifies.

Note: Prognoses are not a reliable indicator of future performance.

The yield curve seems to become more steep. What are the major reasons for this?

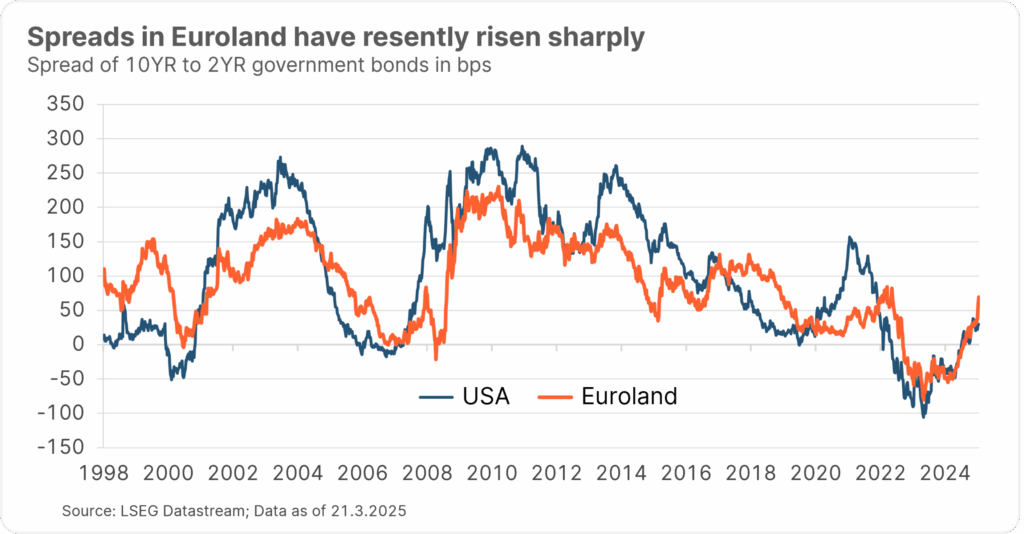

Steepening has been a general trend in the global bond markets for the past couple of months, and this move was pretty intense in Europe. As I already mentioned headwinds for the Eurozone economy certainly remain on the shorter run but the medium to long run looks more promising. Fiscal expansion in Germany does not guarantee success, but it brings some kind of hope that Germany can finally break away from the secular stagnation like environment it has been suffering from for many years.This dynamic of the expectations perfectly validates the steepening move of the European curve.

🔎💡 What does a steep yield curve mean?

A steep yield curve is one in which yields rise more at the long end than at the short end. The difference between long- and short-term interest rates is therefore increasing. This is often the case when the expected level of future inflation rises and market participants start to price in higher key interest rates.

The opposite of a steep yield curve is an inverted yield curve, in which short-term interest rates are higher than long-term interest rates. This scenario often occurs when the market expects an economic slowdown or recession.

Talking about steepening, the substantial increase of government debt supply due to the stimulus package, has to be mentioned as well. German fiscal spending is expected to increase around 3 percent annually, and the public debt is seen to rise by 20 percent of the GDP. Annual net bond supply will shoot up in an environment, where the European Central Bank is still doing Quantitative Tightening (QT). Relatively hawkish FED and slowing US growth might lead to some temporary flattening of the US curve, and this move could pose some headwinds, to the Europen steepening as well, but the direction of travel is going to remain the steepening on the medium run.

Note: Past performance is not a reliable indicator of future performance.

Resilience is a topic in fixed income portfolios. How does a robust portfolio look like in the current environment?

The current environment with stagflationary risks puts the fixed income investor in a tricky position. Slowing economic growth would call for some bond exposure, but potential accelerating inflation requires caution. In my view, given the fact the inflation is a lagging indicator, the economic slowdown due to the trade war will sooner or later mitigate inflationary pressure. Nevertheless the situation in the Eurozone looks more complicated due to the stimulus package. Despite the current uncertainties, there is definitely room for bonds in portfolios these days. Economic slow down and fragile equity markets makes this asset class more attractive. I would focus on short and medium segment of the curves, and in my view USD rates probably look more attractive compared to EUR rates at the moment. I would be cautious with longer maturities though. Heavy debt supply, ongoing QTs (quantitative tightening) and increasing term premium could result in further steepening of the curves.

Note: Please note that an investment in securities entails risks in addition to the opportunities described. Prognoses are not a reliable indicator of future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Market update: Economists see Germany economy regaining momentum

In football, things have been going well for the European Championship host country Germany recently with its place in the round of 16, but the economy has been in the doldrums in recent quarters. According to leading economists, this could now change. Positive signals from industry and private consumption indicate that the German economy is regaining momentum.

Environmental stocks: How is the sector faring in the current volatile environment?

The first quarter had a few surprises in store for the markets. The US tariff announcements shook the markets to the core and caused a volatile stock market environment. The environmental technology sector was not spared either. What is the outlook for the sector? We asked fund managers Clemens Klein and Alexander Weiß in a double interview.