Despite the recent stock market crash, signs are indicating a recovery for Japan’s economy. Although the Bank of Japan’s surprising interest rate hike earlier this month led to strong short-term turbulence on the stock and currency markets, the markets have since stabilised again.

The announcement by the BoJ that it would hold off on further interest rate hikes for the time being also helped to calm the situation. In addition, the latest economic data indicates a return to growth. According to the latest figures from the government, Japan’s economy (GDP) grew by an annualised 3.1% in Q2, following a contraction of 2.3% in the previous quarter. After many years of ultra-loose, negative interest rate policy, this could pave the way for a further tightening of interest rates and return to normality.

Note: Prognoses are not a reliable indicator of future performance.

Turning away from ultra-loose monetary policy

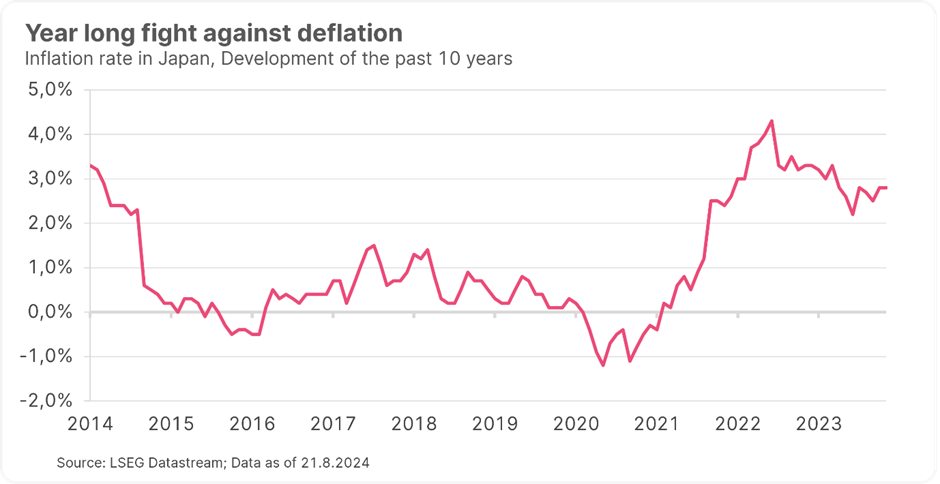

In terms of monetary policy, Japan has been an exception among the world’s major economies. While other countries’ central banks successively raised their key interest rates in recent years in the fight against inflation, interest rates in Japan virtually remained at zero. This was intended to stimulate lending for consumption and investment and to combat deflation, which had been plaguing Japan for years: a decline in prices can pose a problem just as much as an exaggerated increase can, as it leads to consumer and investment restraint and can trigger an economic downward spiral.

The low interest rates also caused a significant decline in the Japanese yen exchange rate. The Japanese currency dropped to around 160 yen per dollar at times this year, a 38-year low. Japan’s export-oriented companies benefited from this, as a weak yen increases demand for their products. The share prices of the corresponding companies also rose sharply, with the Japanese Nikkei stock index growing by around two-thirds during the course of this year.

Note: Past performance is not a reliable indicator of future performance.

Surprising interest rate hike

The BoJ’s recent surprise interest rate hike came as a shock to some investors. In March, the central bank had already abandoned its ultra-loose monetary policy by increasing its short-term key interest rate from minus 0.1 per cent to a range of 0 to 0.1 per cent. In late July, the BoJ then raised interest rates again to 0.25 per cent. This move surprised many analysts and investors alike, catching the latter off guard.

Many investors had expected interest rates in Japan to remain extremely low and wanted to profit from the high interest rate differential with other countries by means of so-called carry trades. In this investment strategy, investors borrow money in a currency with low interest rates and invest it in regions with high interest rates, such as Europe or the USA. Carry trades in particular, in which money from yen loans is invested in US bonds and equities, were widespread.

Financial markets recovered quickly after the mini-crash

The surprising interest rate hike in Japan, coupled with the prospect of further interest rate increases and the expectation of interest rate cuts in other regions such as the US, made these carry trades significantly less attractive or even potential losing trades. Many investors therefore sold their bonds and shares in dollars or euros and bought yen to close their loans. This caused the yen to rise further and at times led to a self-reinforcing spiral.

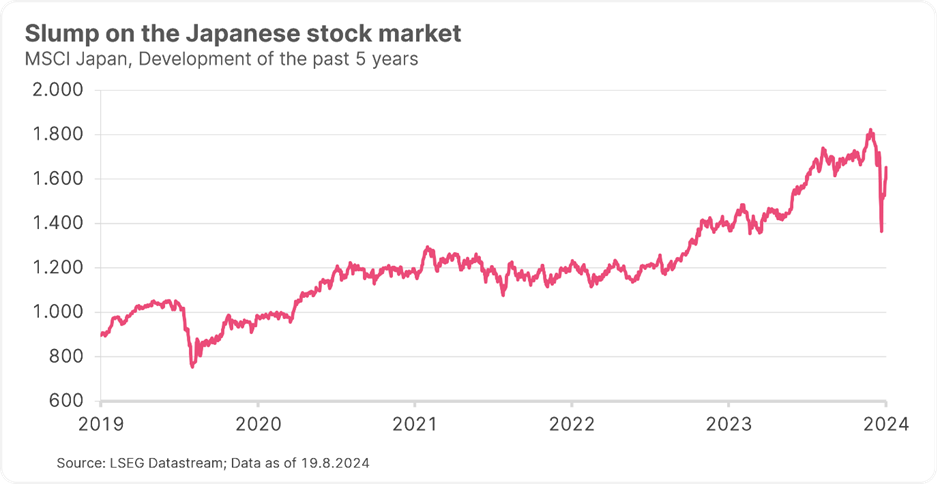

In addition, a nearly concurrent surprisingly weak US labour market report momentarily fuelled fears of an impending recession in the US, while the quarterly figures of some US technology companies raised doubts regarding the high expectations of the current AI boom. The result was a massive sell-off on the stock markets in the first week of August. The Japanese Nikkei stock index fell by 12.40 per cent on 5 August, the largest percentage loss in 37 years.

However, the following day, the markets stabilised and began to recover, with the Nikkei gaining back nearly 10 per cent on 6 August alone. The Bank of Japan also sought to calm the situation after the short-term turbulence on the financial markets. Two days after the mini-crash, the BoJ’s deputy governor, Shinichi Uchida, declared that there would be no further interest rate changes for the time being. The central bank would “not raise its key interest rate when the financial and capital markets are unstable”.

Experts Expect Further Interest Rate Hikes Down the Road

In the medium term, however, experts are expecting further interest rate hikes and thus a continuation of Japan’s return to normality, which country’s economy should also benefit from. Although the yen’s expected rise will likely put pressure on export-oriented companies, it should have a positive impact on domestic purchasing power, fuelling domestic consumption. In the past quarter, domestic consumption was the primary driver of economic growth, from which companies focusing on the domestic market should benefit the most. At the same time, export-oriented companies should also suffer less from a stronger yen than in the past, as many Japanese companies have expanded their production facilities outside of Japan.

Current sentiment indicators are also promising. According to the latest Tankan survey by the Bank of Japan, sentiment among major Japanese industrial producers improved in the three months leading up to June, reaching its highest level in two years. The sentiment index for large manufacturers rose from +11 in March to +13 points in June, slightly exceeding the market forecast of 12 points. According to the survey, Japanese large enterprises plan to increase capital expenditure by 11.1 per cent in the current fiscal year, which ends in March 2025, compared to 4.0 per cent in the last Tankan survey. In light of this development, some economists expect Japan’s central bank to eventually continue its move away from a loose monetary policy with one or more interest rate hikes before the end of the year.

This willingness was recently underlined by the deputy head of the central bank in Japan. If inflation moves in the right direction, the tightening of monetary policy will continue, he said this week.

Investing in Japanese stocks

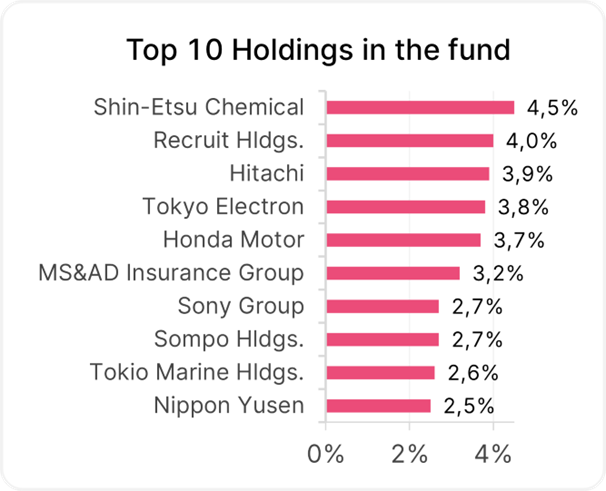

With ERSTE RESPONSIBLE STOCK JAPAN, investors can invest in Japanese equities across many different sectors. The fund has recovered quickly from the temporary slump on the Japanese stock market, resulting in a clear gain of about 16% in the year to date.

The fund invests in shares of selected companies domiciled or listed in Japan. The focus is on companies with medium to high market capitalization, attractive dividend yields and above-average quality. Sustainability criteria are also taken into account in the investment process.

Note: Please note that investing in securities involves risks as well as opportunities. Past performance is not a reliable indicator of future performance. Performance is calculated according to the OeKB method. The performance assumes a full reinvestment of the distribution and takes into account the management fee and any performance-related remuneration. The one-off issue premium that may be incurred upon purchase and any individual transaction-related or ongoing income-reducing costs (e.g. account and custody account fees) are not included in the presentation. The companies listed here have been selected as examples and do not constitute an investment recommendation. Data as of 21.08.2024

Notes ERSTE RESPONSIBLE STOCK JAPAN

The fund employs an active investment policy and is not oriented towards a benchmark. The assets are selected on a discretionary basis and the scope of discretion of the management company is not limited.

For further information on the sustainable focus of ERSTE RESPONSIBLE STOCK JAPAN as well as on the disclosures in accordance with the Disclosure Regulation (Regulation (EU) 2019/2088) and the Taxonomy Regulation (Regulation (EU) 2020/852), please refer to the current Prospectus, section 12 and the Annex “Sustainability Principles”. In deciding to invest in ERSTE RESPONSIBLE STOCK JAPAN, consideration should be given to any characteristics or objectives of the ERSTE RESPONSIBLE STOCK JAPAN as described in the Fund Documents.

Chances and risks in overview

Benefits for investors

- Broad diversification in selected Japanese companies with little capital investment.

- Opportunities for attractive capital appreciation.

- The fund is suitable as an addition to an existing equity portfolio and is intended for long-term capital appreciation.

Risks to be considered

- The price of the fund can fluctuate considerably (high volatility).

- Due to investments denominated in foreign currencies, especially in Japanese Yen, the net asset value of the fund can be negatively impacted by currency fluctuations.

- Capital loss is possible.

- Risks that may be significant for the fund are in particular: credit and counterparty risk, liquidity risk, custody risk, derivative risk and operational risk. Comprehensive information on the risks of the fund can be found in the prospectus or the information for investors pursuant to § 21 AIFMG, section II, “Risk information”.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.